IN TODAY'S ISSUE:

- Discounts on DATs are widening, but DATs are failing to reach a crucial hurdle.

- Digging into the USD1 stablecoin, we find that it is largely held offshore, which aids in some of the administration’s objectives but hampers others.

- Since its launch, USD1 accounts for 4.1% of the industry-wide inflows into stablecoin, but only 1.1% when excluding one large deal.

DAT Discounts Deals Widen

A few weeks back, we noted an interesting transaction in the DAT markets, where tokens were being offered at a discount that let investors purchase shares below NAV. In the case of the Solmate Solana DAT, which was acquired by Brera Holdings (BREA), investors gained entry at a 15% discount to NAV (0.85x mNAV). This week brought another such deal, with Mountain Lake Acquisition Corp. (MLAC) merging with Avalanche Treasury Co. (AVAT) with equity investors participating at a valuation reflecting a 23% discount to NAV (0.77x mNAV). Discounts and other incentives are increasingly being used to entice investors as the differentiation between DAT strategies is becoming increasingly difficult.

In the case of the MLAC transaction, shares climbed to $10.50 following the announcement, compared to the $10.00 pricing for PIPE and original SPAC shares. One consideration, however, is the extended timeline typical of DAT SPAC deals. While shares may trade higher initially, it can take months for the merger to close and for the shares tied to the transaction to be registered and tradable. For example, the first SPAC-structured transaction, Cantor Equity Partners (CEP) acquiring Twenty One, a firm backed by Tether and led by Jack Mallers, was announced on April 22. Nearly five and a half months later, that merger still has not closed, and the deal shares remain unregistered and unavailable for investors to trade.

While long time to liquidity will be one issue for investors, the more pressing concern in the MLAC/AVAT deal is the premium (or lack thereof) to NAV. Even though the deal was structured as a discount to NAV, giving it more than a few steps head start, the proforma NAV/share is $11.33/sh (assuming no SPAC investors redeem their shares and using 22.2M AVAX and 59.2M shares). That’s above the current stock price (still a discount to NAV). Essentially, the DAT didn’t get enough lift to achieve flight. With shares trading below NAV, it eliminates the most valuable tool in a DAT’s arsenal to generate yield – issuing stock at a premium to NAV. The DAT can still lever up, as well as engage in active treasury management, to grow its crypto/share, but issuing equity would be off the table if things don’t change.

USD1 Aims to Keep America #1

This week, at the Token2049 conference in Singapore, representatives from World Liberty Financial, the DeFi platform majority owned by the Trump family, discussed plans to tokenize real-world assets (RWAs) and pair them with its stablecoin, USD1. While details were sparse, the comments highlighted the intersection of two of the most important trends within crypto, stablecoins and RWAs. Representatives also said that dollarizing the world was a “patriotic mission,” but one that was “also very good for the world.”

USD1 Under the Hood

Given the prominence of the project and what’s publicly known, we took a closer look at USD1 to consider the implications for investors and public policy. The first thing to understand is that USD1 is issued and redeemed by BitGo Technologies, LLC, not by World Liberty Financial, Inc. The USD1 brand is owned by World Liberty Financial, Inc. and SC Financial Technologies, LLC, while reserves are held in segregated qualified trust accounts at BitGo Trust Company, Inc., a South Dakota–chartered trust company regulated by the South Dakota Division of Banking. BitGo Technologies, LLC is registered with FinCEN as a Money Services Business and holds state money-transmitter licenses, while BitGo Trust oversees custody of cash and money market funds for the benefit of token holders. The best way to think about it is that BitGo provides the back-end infrastructure and reserve management, while World Liberty Financial serves as the market-facing front end.

Looking ahead, this structure may need adjustment once the GENIUS Act takes effect (the earlier of January 2027 or 120 days after final rules). The law limits issuance to subsidiaries of insured depository institutions, federal-qualified issuers, or state-qualified issuers. As currently structured, BitGo Technologies, LLC does not appear to fall into any of those categories, suggesting that adjustments would be required to maintain compliance. This isn’t an existential threat, but it is an important nuance for understanding USD1’s long-term regulatory trajectory.

Surprisingly, we found out that the issuer’s monthly attestation reports are tardy, the most recent of which is July (it’s October, guys). Lack of reserve transparency has been the number one, two, and three issue for stablecoins since their inception. For a project of USD1’s stature, up-to-date attestations are non-negotiable (Circle/USDC is updated through August, and Tether/USDT does them only quarterly).

Four Different Assets – BNB Chain Leads the Way

The other important fact about USD1, like most “stablecoins,” is that it’s not just 1 token; it’s technically 4 different tokens, each issued on different networks, Ethereum, BNB Chain, Solana, and TRON.

According to our analysis, the overwhelming majority of the USD1 tokens are issued on BNB Chain, which, while more open-sourced in development today, with a diverse set of validators, is still closely associated with Binance by way of history.

America’s Stablecoin Held Mostly Offshore?

Aggregating balances across chains, it’s clear that USD1 is overwhelmingly preferred by offshore holders vs onshore. 78% (at a minimum, we only looked at the top addresses) of USD1 tokens are held in wallets associated with offshore entities, such as exchanges.

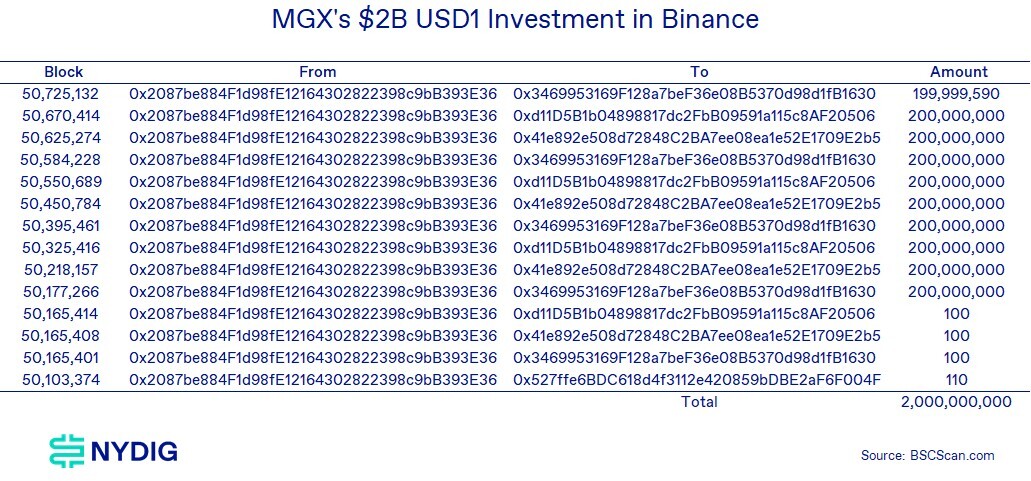

At first blush, one might ask what is a stablecoin that most closely associated with the President doing mostly held offshore? Importantly, USD1 tokens were used in the settlement of MGX's, an AI-focused investment group founded by the Mubadala sovereign wealth fund and AI company G42, investment into crypto exchange Binance. The following transactions are likely the funding transactions for the $2B deal. Strangely, the USD1 BNB Chain balances held in offshore accounts are lower today than the $2B MGX investment, implying that USD1 issued on BNB Chain has migrated to unidentified addresses (likely) or been redeemed.

USD1 Inflows Compared to the Industry

Taking into context the $2B MGX investment and the total USD1 supply of 2.7B tokens brings up an important point – excluding the MGX investment, USD1 has seen inflows of $688M. This is important given the current stablecoin boom going on. Since the launch of USD1 at the end of March, stablecoins have grown by $65.4B by our calculations, giving USD1 ex-MGX a share of 1.1% of the industry inflows or 4.1% considering the MGX investment.

Exporting the USD – Two Sides to the Story

On one hand, distributing USD stablecoins to users outside the United States reinforces the dollar’s dominance and solidifies its role as the world’s reserve currency, an invaluable advantage that Washington has arguably leaned on too heavily in the past. On the other hand, this dynamic runs counter to the administration’s explicit and implicit objectives, which include fostering a weaker dollar to stimulate exports and bolster domestic manufacturing. Ultimately, this tension highlights the difficult trade-offs between preserving global financial power and pursuing domestic economic priorities.

Market Update

Bitcoin surged 10.5% this week, breaking back above $121K. Notably, the rally wasn’t driven by forced buying as short liquidations were limited. Spot ETF inflows accelerated, with $2.3B of inflows from Monday through Thursday, likely contributing to upward pressure. Additional momentum came from Metaplanet’s headline purchase of over 5,200 BTC (about $620M) in the wee hours of Wednesday morning, which appeared to coincide with part of the rally.

Funding rates on perpetual swaps remained modestly positive, while CME futures basis climbed alongside price but stayed well below overheated levels. In short, even after double-digit gains, the rally does not appear stretched. At the same time, the “debasement” trade continues to gain traction with investors, gold is up 45.4% year-to-date, silver 64.0%, and the Bloomberg US Dollar Spot Index is down 8.2%, suggesting that bitcoin may also be benefiting from these macro-driven flows.

Important News This Week

Investing:

JPmorgan Sees Bitcoin Hitting $165,000 By Year-End on Retail-Led 'Debasement Trade' - The Block

Vanguard Flirts With Crypto - Decrypt

IBIT’s Options Market Fuels BTC ETF Dominance - CoinDesk

Regulation and Taxation:

SEC Staff Backs State-Chartered Trust Companies as Qualified Custodians - SEC

Companies and Industry:

The Stablecoin Duopoly is Ending - Nic Carter

Visa Direct Taps Stablecoins to Unlock Faster Funding for Businesses - Visa

The Debate Raging Over Bitcoin's Future - Decrypt

BTC Mining Hits Toughest Level Yet While Hashprice Slides - CoinDesk

Upcoming Events

Oct 15 - CPI inflation data

Oct 31 - CME expiry