IN TODAY'S ISSUE:

- We review the first major M&A DAT announcement as ASST finalizes a deal for SMLR.

- Metrics such as mNAV continue to be misleading for investors for several reasons.

- Based on the math, the deal appears favorable for both SMLR and ASST shareholders.

DAT Deals Spring Up as ASST Snaps up SMLR

This week saw the first merger in the Digital Asset Treasury (DAT) landscape, with Strive (ASST) acquiring Semler Scientific (SMLR) in an all-stock deal. The merger, which was announced Monday morning, represents the first time one DAT acquired another DAT (both bitcoin DATs). This was something we had theorized could occur, but the first time it has crystallized. Given that there are many other DATs (mostly non-BTC) trading below their NAVs, this could be a harbinger of things to come.

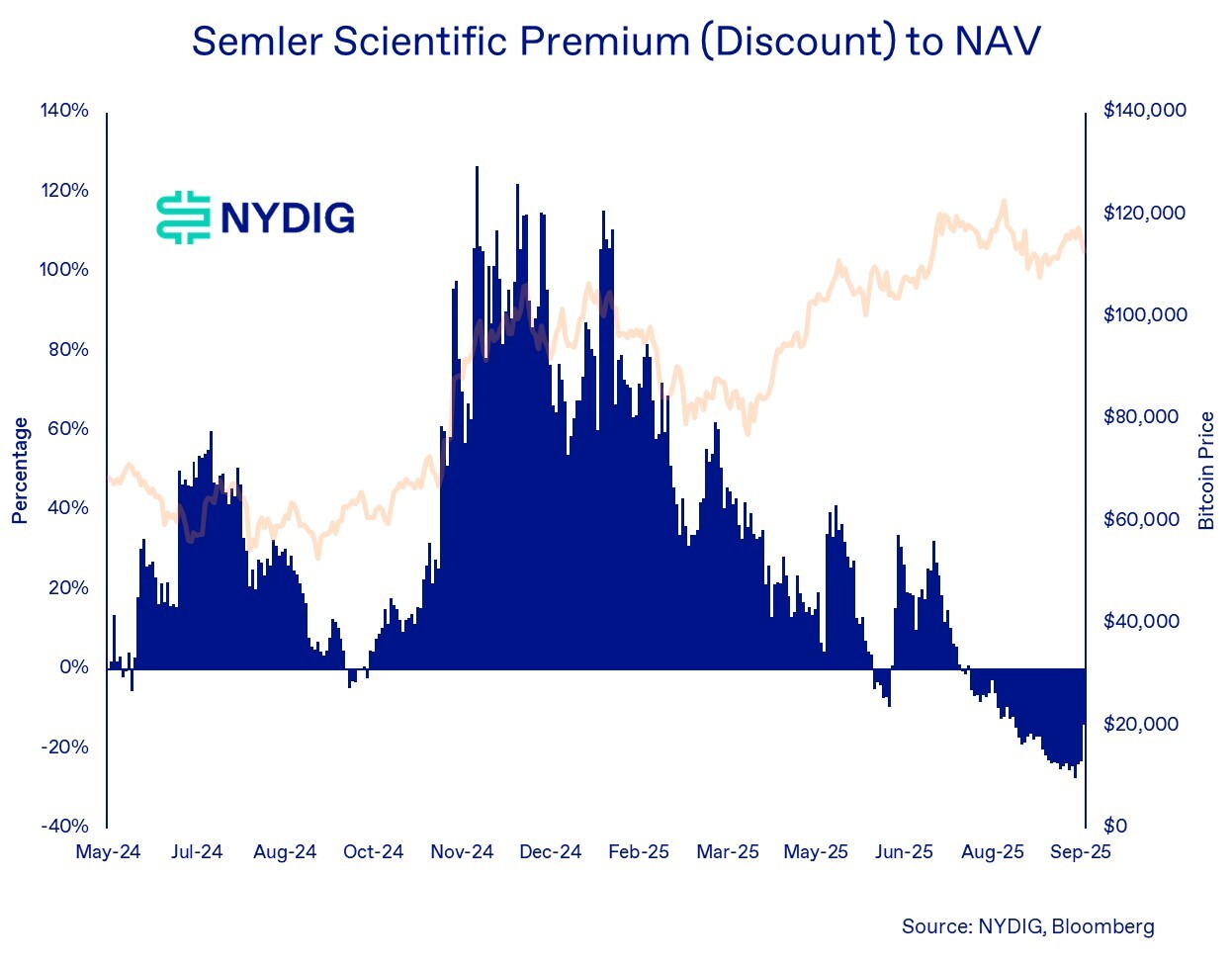

SMLR Has Been an Opportunity for a While

This deal has been a potential opportunity for a while now. SMLR was an early adopter in wave 2.0 of the bitcoin treasury companies, adding bitcoin to its balance sheet in May 2024, right after Metaplanet started its effort. It has also been trading at a discount to its NAV for months, first flipping negative in June and consistently negative since July.

While some DATs have highlighted the opportunity to buy other DATs at a discount, the reality is that few DATs have outlined active treasury management to increase crypto per share (observation: this seems to be more common outside of bitcoin DATs, where staking and DeFi activities are readily available options). Strive, right from the start, was one of the few bitcoin DATs to highlight active treasury management. Most DATs seem content to issue stock at a premium to NAV or to lever up.

The Definition of mNAV Needs to be Expunged from the Records

We’ve written about this before (here), but the industry definition of “mNAV” needs to be deleted and forgotten. “Market cap to bitcoin/digital asset value,” the original definition of mNAV, is a useful metric for nothing. At best, it’s misleading; at worst, it’s disingenuous. Note: some companies seem to be replacing “market cap” with “enterprise value.” Better, but still insufficient.

The reason is two-fold. First, for companies with operating businesses or assets outside of the DAT (Semler is one of them), it doesn’t give credit to the operating company. NAV is what matters in the game of increasing digital assets/share, not enterprise value or heaven forbid market cap – can the DAT issue equity at a premium to its NAV? This is how it creates “yield.”

The other reason is the metric, “assumed shares outstanding.” It sounds appealing at first - a fully loaded share count (common, stock options, and potential dilution from convertible issuances). But when you peel back the convertible debt part, things unravel. First, accounting for convertible debt automatically as equity is not correct from an accounting or economic perspective. If the conversion hurdles have not been met (time, price, etc.), economically, it should be treated as debt. Convert holders would demand cash, not shares, in exchange for their debt. This is a much more onerous liability for a DAT than simply issuing shares. The other issue, and we’ve written about this before (here), is that because convertible debt is essentially volatility harvesting (converts are debt + call options), the DAT is incentivized to maximize its equity volatility. A very simple way to do this is lever up, which may or may not be a desired outcome for equity holders.

Deal Mechanics

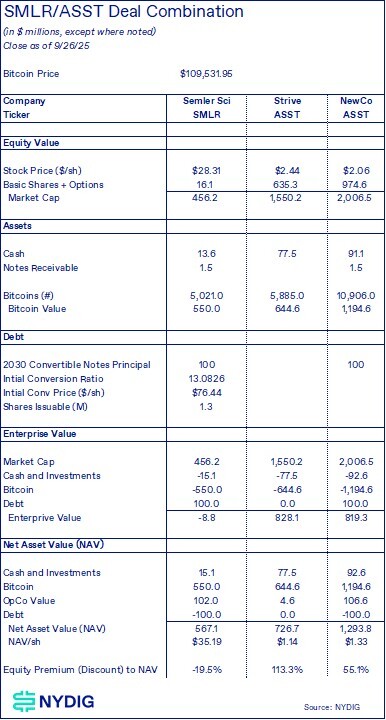

The mechanics of the SMLR/ASST deal are fairly simple – SMLR shareholders will get 21.05 shares of ASST for every share of SMLR they own. SMLR has a convert outstanding, $100M of convertible notes due in 2030, but given the pricing and deal structure, make-whole or put-back (fundamental change) clauses won’t be triggered. The combined companies would control over 10,900 bitcoins, making it a much larger scale player. The combined “NewCo” companies should look like this:

Does the Deal Make Sense?

Is this a good deal? This is the question on everyone’s mind.

For ASST shareholders, they get a step up in the NAV/share – “yield,” essentially, in the DAT vernacular. ASST’s current NAV/sh is $1.14, which is lower than that of the PIPE deal that closed, almost purely because they are down on their recent bitcoin purchase ($116,047 avg price). The NewCo (combined SMLR/ASST) should have a NAV/sh of $1.32. Another way to look at this is they are selling stock above NAV, which is how DATs increase their NAVs/sh.

For SMLR holders, they are getting their stock valued above the NAV/sh of both existing ASST stock and the NewCo. It works out for both, albeit after some work (which we’ve conveniently done for investors). The “210% premium” and “$90.25/share” metrics cited in the joint press release were admittedly a bit confusing.

As for where this stock ultimately trades, that’s harder to predict. It will ultimately depend on the premium or discount to NAV that investors put on the stock (Friday's close was $2.44, and PIPE shares still need to be registered). But as a proof point, using NAVs (again, not mNAVs), the SMLR acquisition by ASST shows how accretive DAT deals can be done.

Market Update

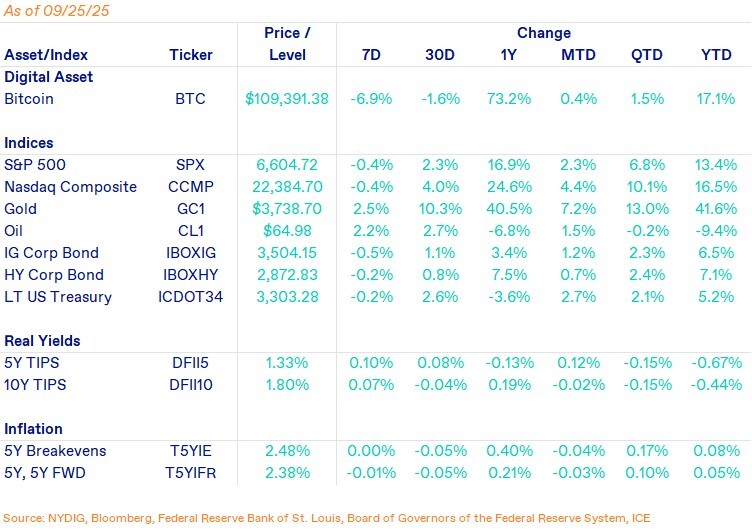

Bitcoin fell 6.9% on the week, briefly breaking below $109K Thursday afternoon before finding support. The decline wasn’t tied to any clear fundamental catalyst we could identify, but momentum has been muted since the cryptocurrency notched a new all-time high in mid-August. Over the past five weeks, equities and gold have continued climbing to record levels while bitcoin has lagged. Even so, at $109K, it remains within striking distance of its $124.5K peak. For context, stocks also ended the week lower, while gold’s rally showed no signs of slowing.

If bitcoin acquisitions from DATs are slowing down, as this Bloomberg article suggests, a significant source of demand and cycle narrative is drying up. We have yet to see any new bitcoin DATs emerge, but there could be continued action coming from the existing players, with several continuing to trade above NAV. Still, as our previous section on the SMLR/ASST deal highlighted, there’s plenty of action to come from DATs.

Important News This Week

Investing:

The Main Driver Behind BTC's Break From Global M2, According to Raoul Pal - CoinDesk

Regulation and Taxation:

Unusual Trading Ahead of Crypto-Treasury Deals Draws Scrutiny From U.S. Regulators - WSJ

White House Eyes Year-End Finish Line for Sweeping Crypto Market Structure Bill - The Block

Acting Chairman Pham Launches Tokenized Collateral and Stablecoins Initiative - CFTC

US Strategic Bitcoin Reserve Audit Now 172 Days Overdue - Protos

Companies:

Michael Saylor Says Short Seller Deployed Bots to Bash MSTR - Protos

Stablecoin Issuer Circle Examines ‘Reversible’ Transactions in Departure for Crypto - FT

Cloudflare Introduces NET Dollar to Support a New Business Model for the AI-Driven Internet - Cloudflare

Upcoming Events

Oct 3 - Jobs report

Oct 15 - CPI inflation data

Oct 31 - CME expiry