IN TODAY'S ISSUE:

- MSTR continues to innovate on financial products, turning bitcoin into a money-market like product.

- The impact the altcoin rally has had on ETF fund flows and bitcoin's dominance.

- The SEC exhibits some unique behavior in its approving of crypto ETFs.

MSTR Transmutes Bitcoin into Stability

This week, Strategy (formerly MicroStrategy) launched its newest financial innovation: the Series A “Stretch” Preferred Stock, or STRC. Originally targeting a $500 million preferred offering, the deal has since been upsized to $2 billion, underscoring strong investor demand.

A Unique Financial Product

STRC joins Strategy’s expanding stable of preferred securities, which includes Strike (STRK), Strife (STRF), and Stride (STRD). But unlike its predecessors, which offer fixed-rate dividends (and in the case of Strike, convertibility into MSTR Class A shares), STRC introduces some novel elements, like a variable-rate, a cumulative dividend, a callable feature, and the intention to adjust monthly dividends to anchor the share price near its $100 face value.

The preferred shares, which are being marked at $90 - $95 according to media reports, are to have an initial monthly dividend rate of 9% annually, which then changes monthly. Strategy can lower STRC’s monthly dividend rate, but only by a maximum of 25 basis points plus the difference between the SOFR (1m) at the start of the prior month and the lowest SOFR rate (1m) observed during that month, and never below the SOFR rate (1m) in effect the business day before notice is given. There is no formulaic cap on raising the monthly interest rate. Proceeds from the STRC offering will be used to fund additional bitcoin purchases.

A High Yield Money Market Replacement?

STRC looks to us like a high-yield, bitcoin-backed, money-market-style vehicle, designed to trade near $100 par while offering a far higher yield than traditional short-term instruments, albeit with a different liquidity profile. With Strategy holding ~$72 billion in bitcoin against just ~$11 billion in debt and preferreds, the 9% dividend appears well-supported, unless STRC issuance scales dramatically.

Although STRC holders have no direct claim on Strategy’s bitcoin, another way to view it is that the 9% yield effectively reflects the company’s outlook on future bitcoin returns. Historically, bitcoin has delivered a minimum annualized return of 3 - 4% over five-year periods, with average returns significantly higher. While future performance may moderate as bitcoin matures, this return history offers a margin of safety. Given the inventiveness and attractiveness of the product, it’s no surprise that investor interest is running high, causing MSTR to quadruple the size of the offering.

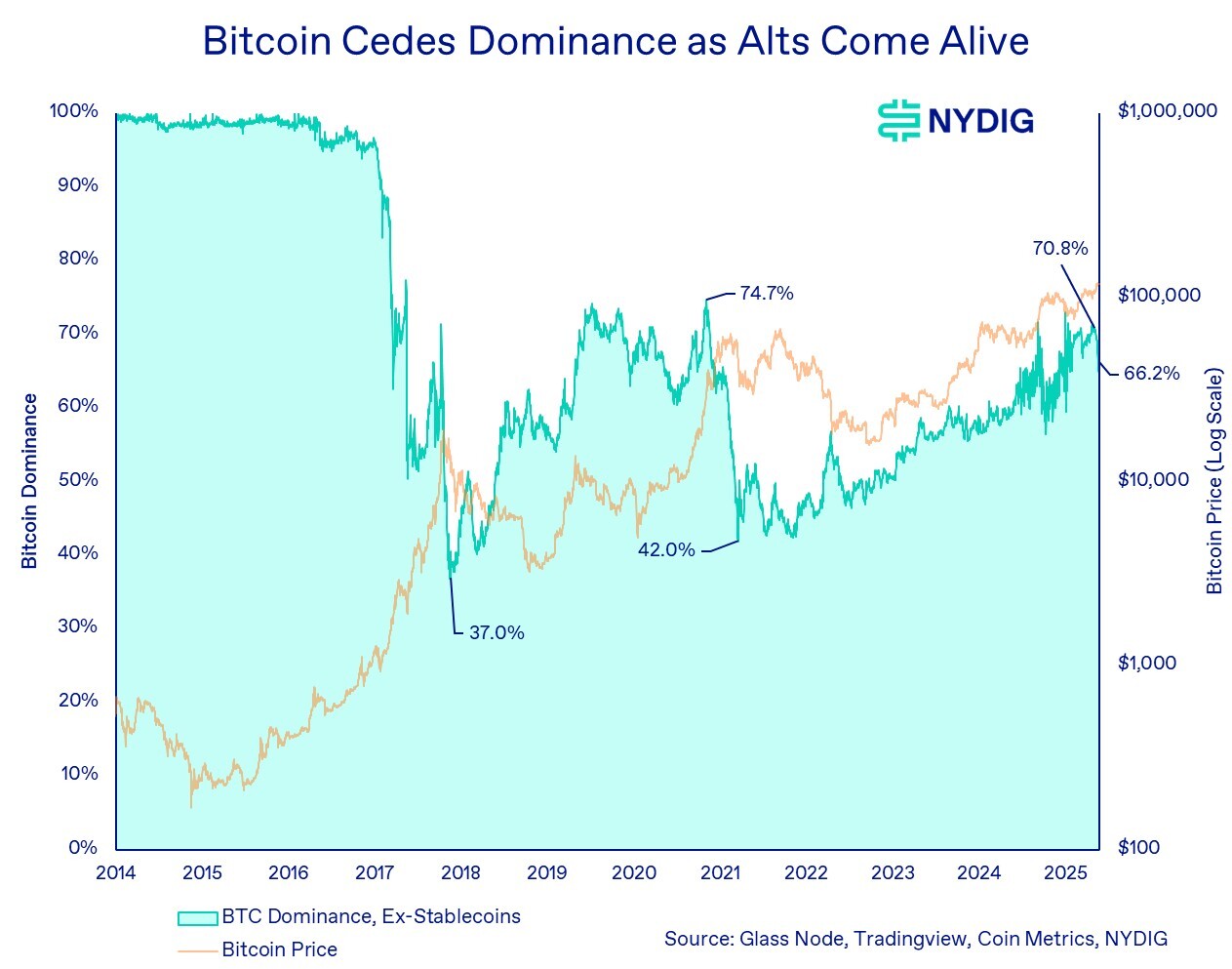

Altcoins Spring to Life as Bitcoin Sheds Dominance

Altcoins (short for “alternative coins”, or anything not bitcoin) experienced a resurgence in recent weeks, affecting bitcoin’s dominance and altering the fund flows into spot ETFs. The altcoin rally, which touched off on or around July 9th, gained momentum ahead of the House of Representatives' “Crypto Week” (July 14-18th), during which lawmakers passed stablecoin legislation and advanced the CLARITY Act (crypto regulatory framework) on to the Senate. The rally unfolded even as bitcoin surged to new all-time highs, breaking $123K for the first time.

Bitcoin’s Dominance Dips from the High

Altcoin rallies have historically been a recurring feature of every Bitcoin price cycle, and the latest surge may be yet another signpost along the way. For example, bitcoin began to rapidly shed dominance (share of the industry market cap) beginning at the end of December 2021, even though bitcoin would ultimately peak in price nearly a year later in November of 2021. The same thing happened in the 2017 cycle, where bitcoin began to shed dominance in March 2017, even though it ultimately peaked in price in December 2017. Bitcoin’s dominance hit a recent high of 70.8%, before falling to 66.2% amidst the altcoin rally. If this pattern holds, the ongoing decline in dominance may signal that the cycle is far from over, not just for altcoins, but for bitcoin’s price trajectory as well.

ETFs May Keep Money Captive in Brokerages

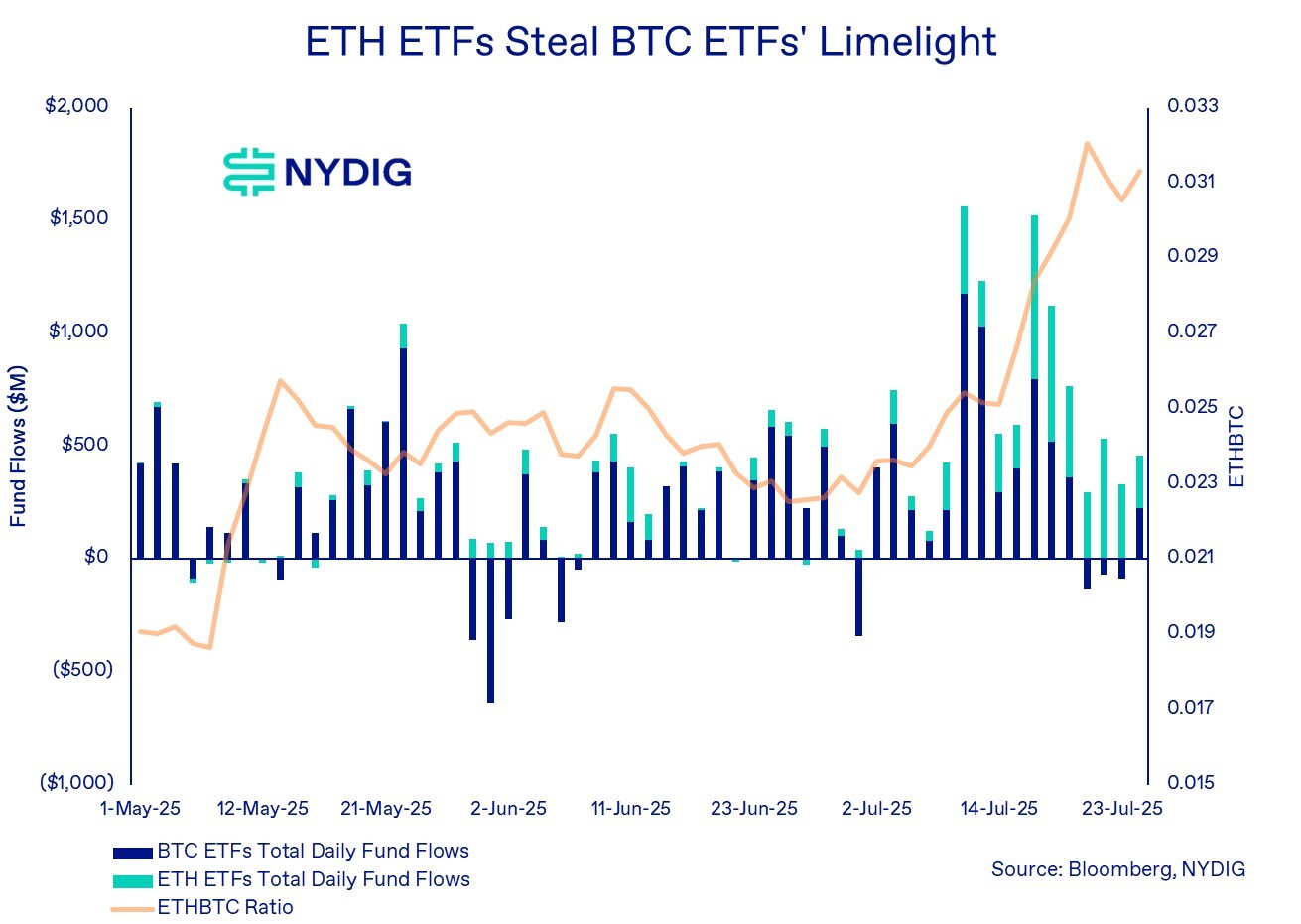

A key difference in this cycle is the introduction of spot ETFs for both bitcoin and ether (Ethereum), which may temper the altcoin rally compared to previous cycles. In previous market cycles, investors primarily accessed crypto through centralized exchanges like Coinbase, where a wide range of tokens were available. Profits from early bitcoin gains often rotated into smaller altcoins, driving significant price appreciation due to the sheer size disparity between bitcoin and the rest of the market. Even modest capital outflows from bitcoin could produce outsized percentage moves in altcoins.

This time, however, with spot ETFs essentially limited to just bitcoin and ether, those profits are less likely to filter into the broader altcoin market. Since these ETFs are held in traditional brokerage accounts, which lack access to the wider range of cryptocurrencies, capital rotation is largely confined to these two assets. As a result, we’re seeing flows shift from BTC ETFs into ETH ETFs, a trend that has become increasingly evident over the past several trading sessions.

Final Remarks

Alt season is a typical feature of crypto market cycles, and the recent resurgence in alts demonstrates to us that the cycle appears to be intact. The changing market structure, with just BTC and ETH ETFs, may dampen the appreciation for alts compared to previous cycles. Narratives for alts also seem to be light this cycle outside of stablecoin, but this is another guidepost that the cycle should continue.

SEC Giveth and Pauseth

In recent weeks, the SEC has engaged in actions we haven’t seen before with approving or denying crypto financial products. The agency’s Division of Trading and Markets recently approved the conversion of the Grayscale Digital Large Cap Fund (GDLC) and the Bitwise 10 Crypto Index Fund (BITW) into ETFs to be listed on NYSE Arca. However, these approvals were immediately paused by the Commission, placing them under formal review and indefinitely delaying their launch until the review is completed. GDLC: Approval, Review. BITW: Approval, Review.

The approvals were poised to mark a milestone in the regulation of cryptocurrencies. GDLC and BITW would have been the first U.S.-listed ETFs to hold spot cryptocurrencies beyond just BTC and ETH, the only two digital assets the SEC has explicitly approved. GDLC holds five crypto assets, and BITW holds ten.

In amendments filed just days before approval and review, both funds (GLDC and BITW) adopted a 15% cap on exposure to "non-Approved Components", tokens the Commission hadn’t already expressly permitted, while committing to hold at least 85% of their assets in “Approved Components,” BTC and ETH. Despite these concessions and the fact that both funds were already in compliance with this requirement, the Commission decided to weigh in directly on the matter. It may take some months before a review is complete, and there is no explicit timeline. The Commission may also be waiting for comprehensive listing standards that don’t require the staff or Commission to weigh in on listing decisions on an ad hoc basis. Either way, other ETF approval deadlines are looming (the Canary Litecoin ETF appears to be the next final deadline on October 2nd), which may prompt the SEC to respond similarly.

No, Fidelity Has Not Been Granted In-Kind Creation/Redemption Orders

With the SEC’s moves closely watched, some media outlets have picked up (but misinterpreted), changes associated with a recent filing for the Fidelity Wise Origin Bitcoin Fund (FBTC). On Monday, the sponsor and Trustee amended the Trust agreement to permit in-kind creation and redemption orders—when approved. The SEC has yet to approve the SRO’s (Cboe BZX) change request.

While we expect the SEC to ultimately permit in-kind creation and redemption orders, Nasdaq is the first in line for review, with an October 10th final decision deadline for its request to allow in-kind orders for the iShares Bitcoin Trust ETF (IBIT). The SEC has yet to make a final decision on in-kind orders for any spot cryptocurrency ETF, nor has it met with any exchanges or sponsors in their evaluation process, according to public records. Ahead of the initial approval of the spot ETFs, we saw a flurry of meetings, including ones specifically addressing creation and redemption orders. We may see those again as a precursor to a final decision by the SEC.

Market Update

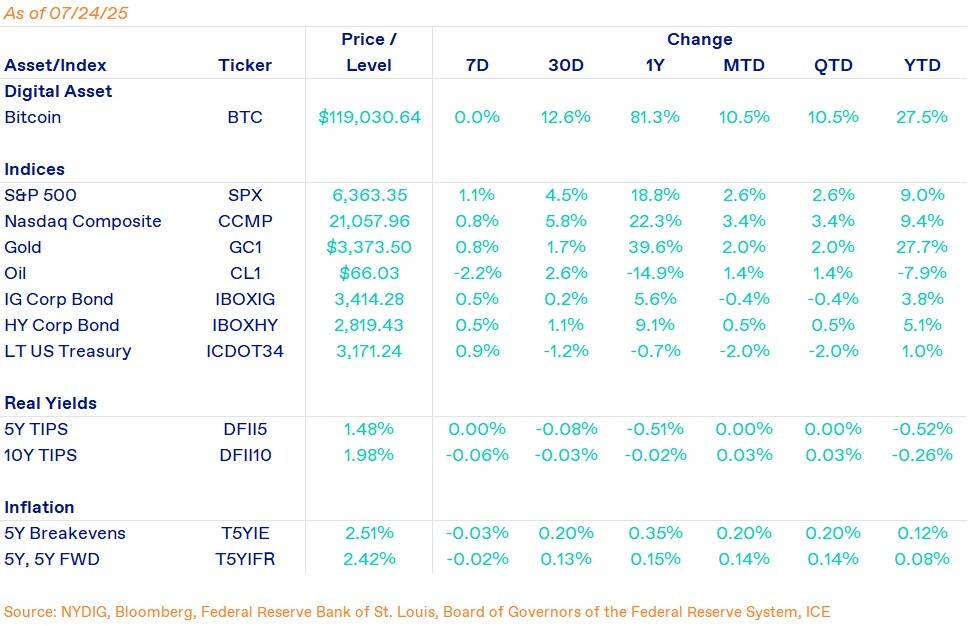

Bitcoin traded flat over the past week as markets continued to absorb the impact of the large-scale selling pressure we highlighted in previous weeks.

Several other significant long-term holders have also reemerged this week. SpaceX transferred $153 million worth of bitcoin to new addresses. In addition, $468 million in bitcoin, dormant for 14.5 years, was moved, along with another $1.7 billion from a separate 14-year-old dormant wallet, likely in anticipation of liquidation. These movements underscore a recurring dynamic of long-term holders distributing to newer market participants, a pattern typical of broader market cycles.

Galaxy Digital has been the destination for many of the long-dormant bitcoins, including the July 4th Whale’s 80,000 BTCs. As of Friday afternoon, our tracking shows that Galaxy has received a total of 88,272 BTCs since the “July 4th Whale” transfers began hitting the service’s provider’s wallet on July 14. Of that, 76,025 BTC have already been moved out, presumably sold, leaving an estimated 12,246 BTC still to be sold, or roughly $1.4 billion in bitcoin.

Important News This Week

Investing:

Bitcoin Price Prediction: $23.7M Bullish Bet Targets $200K by Year-End - CoinDesk

Citadel Securities Warns SEC Against Rushed Tokenized Securities Rollout - CoinDesk

Bankrupt Crypto Exchange FTX to Start Next Round of Creditor Repayments on Sept. 30 - CoinDesk

Regulation and Politics:

FBI Drops Probe of Kraken Founder Jesse Powell, Returns Devices - Fortune

Companies:

Trump Media Announces its Purchases for Bitcoin Treasury - Trump Media

rump Media Bets on Bitcoin Options in Push for Crypto Profits - Bloomberg

MARA Holdings Plans $850M Convertible Note Offering to Fuel BTC Purchases, Repay Debt - CoinDesk

Tether CEO Says Stablecoin Issuer Is Making Plans to Do Business in US - Bloomberg

Companies Load Up on Niche Crypto Tokens to Boost Share Prices - FT

Upcoming Events

Jul 25 - CME expiry

Jul 30 - FOMC interest rate decision

Jul 30 - White House Crypto Working Group to Deliver Report

Aug 12 - CPI report