IN TODAY'S ISSUE:

- Bitcoin reached a new all-time high during the quarter, but after a liquidation-led sell-off, it declined 23.5% during Q4 2025.

- The weak performance in what is typically a strong quarter seasonally left bitcoin in the red for the year, declining 6.3%.

- In stark contrast, gold & precious metals had a banner quarter & year, making bitcoin’s “digital gold” moniker symbolic, though still a useful framing device.

- Looking ahead, 2026 is going to be the year where we test the cycles vs secular growth thesis. Our advice: allocate, don’t speculate.

- Volatility is likely to continue its secular decline, punctuated by sudden spikes, a bane for volatility harvesters, but a boon to spot ownership.

- Growth in tokenization/RWAs and stablecoins is likely to continue regardless of what price action, unlike what happened with institutional initiatives in 2022.

- TradFi is likely to continue to adopt crypto, percolating into custody, collateral management, settlement, and market infrastructure.

- Quantum computers continue to be THE risk for investors. Their threat isn’t immediate, but mitigation planning likely begins.

- DATs likely trade as crypto beta plays, and for those trading below NAV, corporate finance activities will play an important role in the coming year.

PERFORMANCE REVIEW

Bitcoin Breaks Seasonality as Precious Metals Dominate

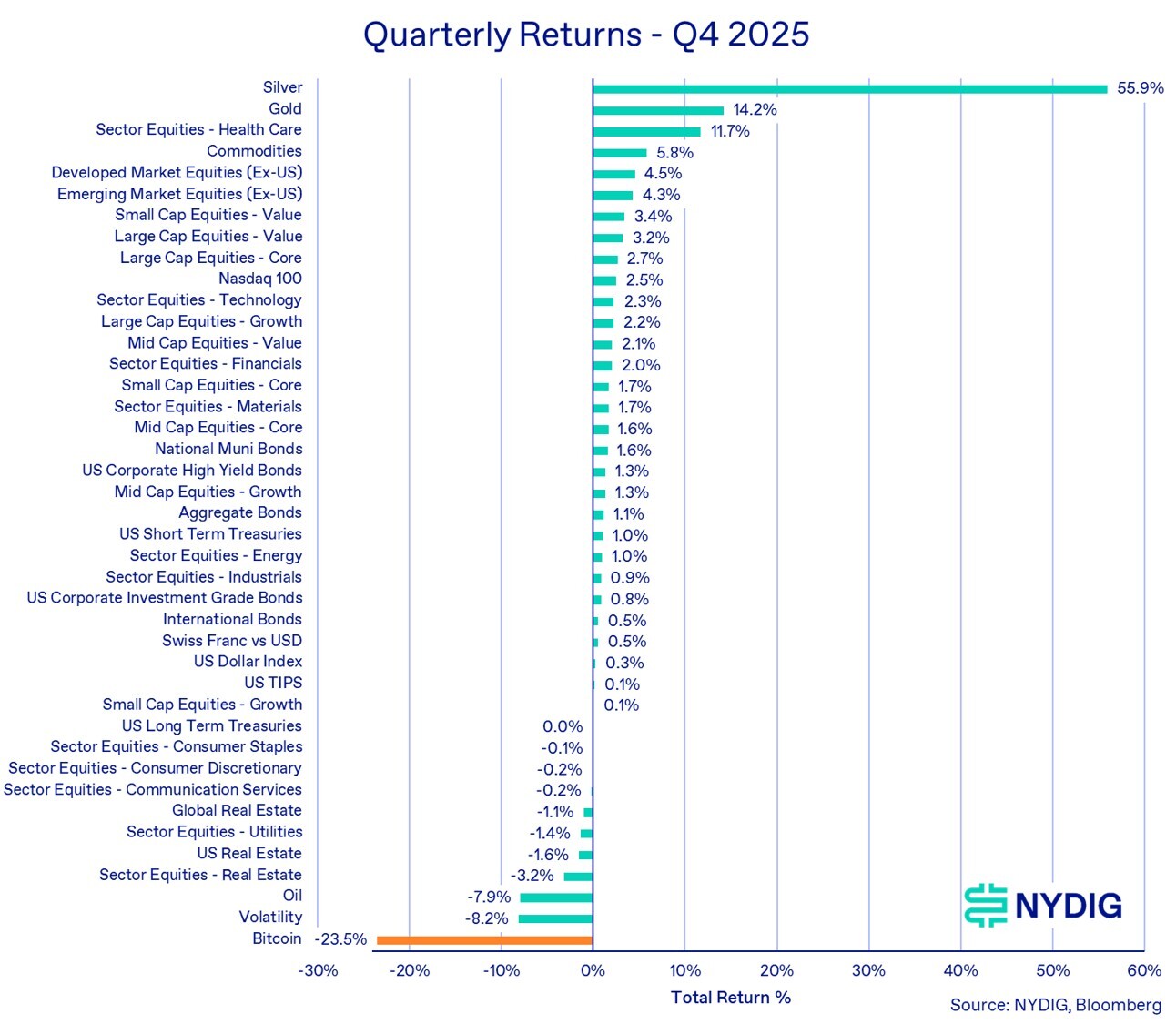

Bitcoin declined 23.5% in Q4, dramatically underperforming nearly every major asset class. Historically, Q4 has been bitcoin’s strongest quarter, making the quarterly decline even more noticeable. The magnitude of the decline places Q4 2025 as the 14th worst fourth-quarter performance since 2011, a notable deviation from historical norms.

The quarter was not without positives, as bitcoin set a new all-time high in early October, briefly trading above $126,000. The level, however, proved short-lived. What followed was a swift reversal driven by renewed China tariff concerns, including the largest futures liquidation event in crypto market history, spot selling by large holders, and declining market depth. By contrast, traditional risk assets remained relatively resilient, underscoring that bitcoin’s weakness was largely endogenous rather than macro-driven.

Precious metals were the clear winners of the quarter. Silver surged 55.9% in Q4 and finished the year up 149.1%, while gold rose 14.2% in the quarter. The scale of this divergence was striking, given bitcoin’s frequent comparison to gold, reinforcing the “digital gold” narrative remains just a narrative for the time being.

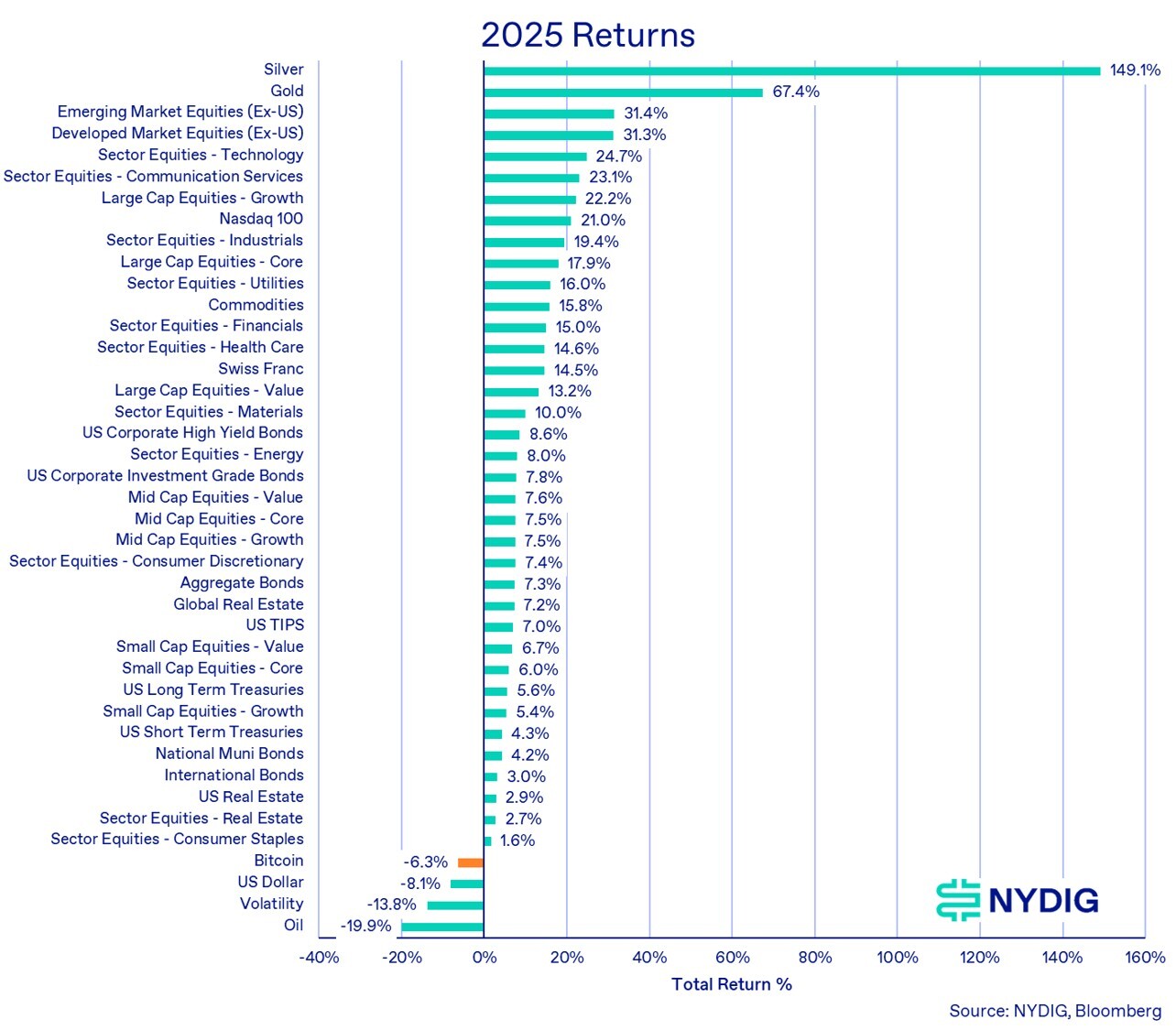

Bitcoin Finishes 2025 in the Red

The Q4 drawdown erased earlier gains, leaving bitcoin down 6.3% for the year and placing it among the weakest performing assets in 2025. This outcome stands in stark contrast to the broader market backdrop. Precious metals were the clear leaders, with silver up 149.1% year to date and gold gaining 67.4%, extending a multi-year trend in the debasement trade. Global equities also delivered strong performance, led by emerging and developed markets ex U.S., both of which posted returns above 30%, while U.S. equities, particularly technology and communication services, finished the year solidly higher. Even traditionally defensive assets, including utilities, investment grade credit, and aggregate bonds, generated positive returns. Against this backdrop, bitcoin’s underperformance underscores both the severity of the Q4 selloff and the extent to which crypto specific dynamics, rather than broad macro conditions, drove returns in 2025.

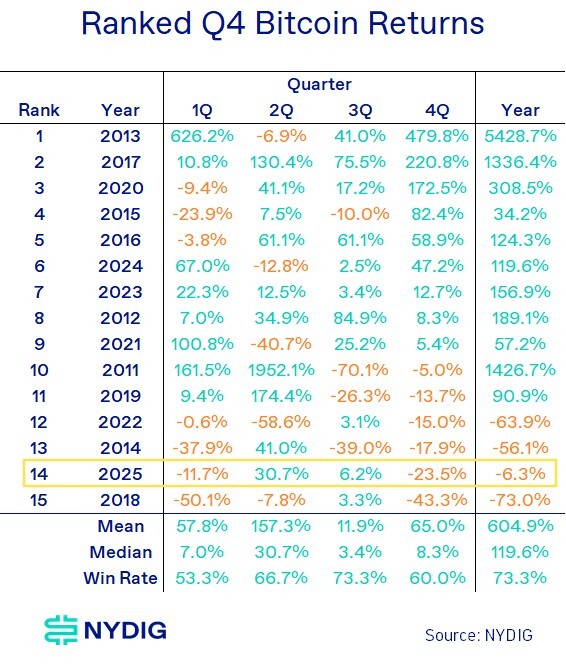

Bitcoin in Historical Context: Quarterly and Annual Rankings

Looking beyond absolute returns, bitcoin’s performance in Q4 2025 takes on additional meaning when viewed through a historical ranking lens. Bitcoin’s -23.5% return ranks 14th out of 15 fourth-quarter outcomes since 2011. This is notable not only because of the magnitude of the decline, but because Q4 has historically been bitcoin’s strongest quarter, delivering some of its most explosive upside moves.

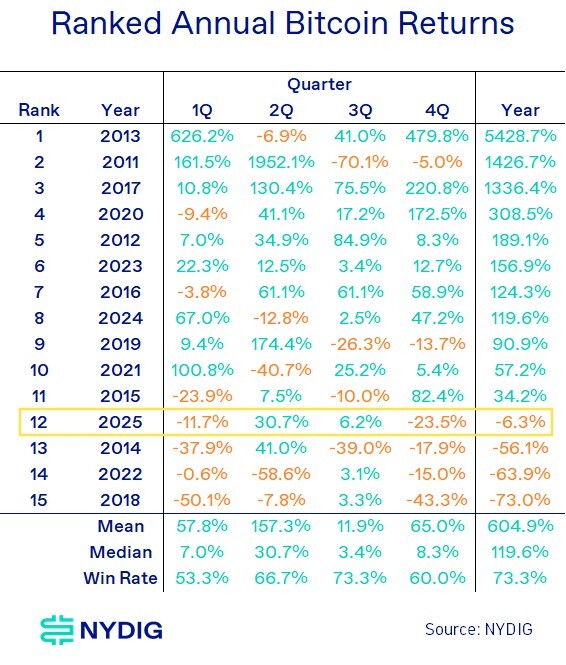

On an annual basis, bitcoin finished 2025 down 6.3%, ranking 12th out of 15 years. While negative annual returns are not unprecedented, they have historically occurred during periods of cyclical drawdowns (2014, 2018, and 2022). In contrast, 2025 unfolded amid improving regulatory clarity, expanding ETF access, and deeper institutional integration underscoring that price outcomes remain path-dependent even when long-term fundamentals appear constructive.

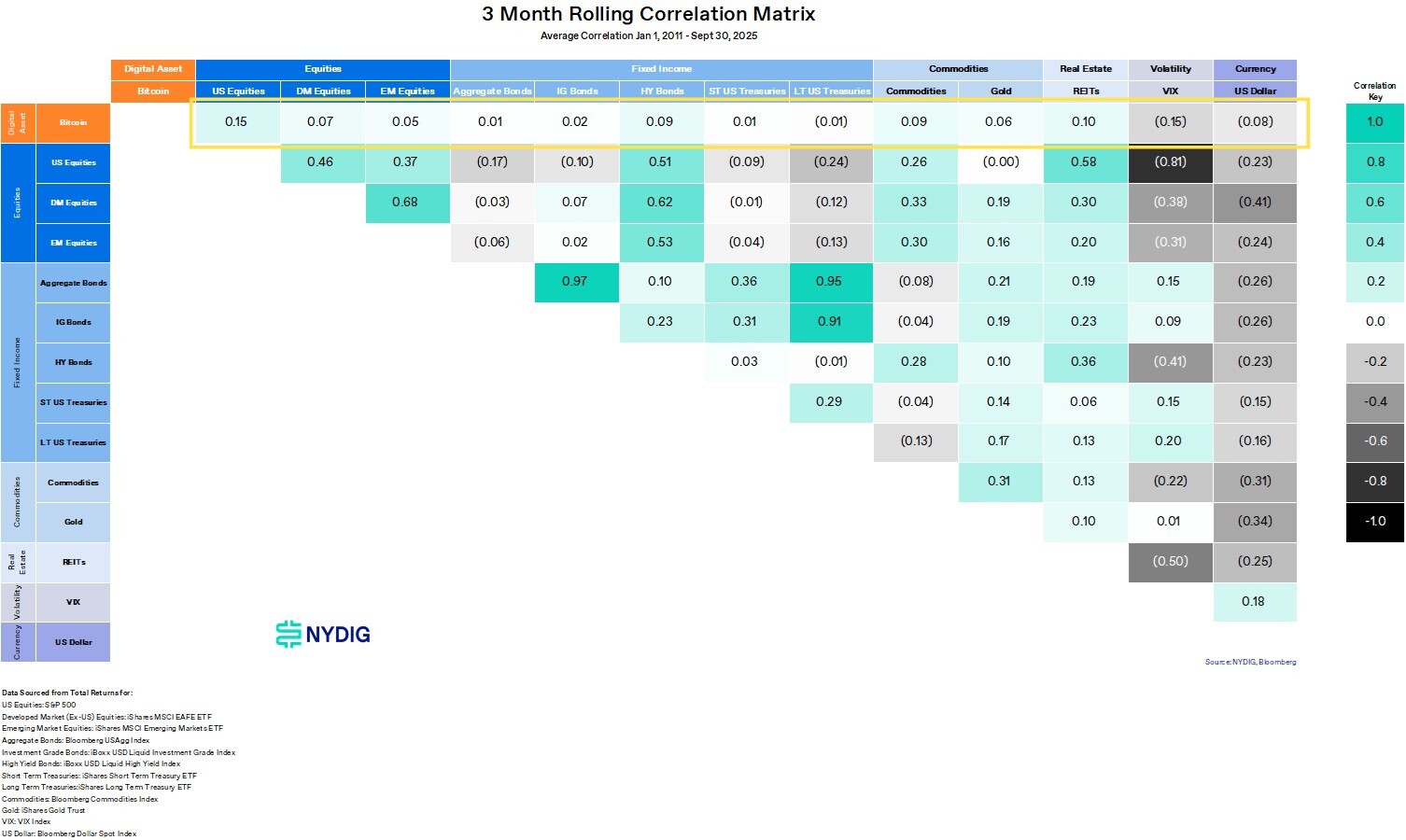

Correlation with Equities: Elevated Still

Bitcoin’s correlations with U.S. equities remain elevated throughout the quarter. As shown in the rolling three-month correlations, bitcoin’s relationship with U.S. equities strengthened during periods of market stress, rising into the 0.4 to 0.6 range at several points over the past year. These episodes of elevated correlation coincided with broader risk-off environments and deleveraging events, consistent with bitcoin’s tendency to trade as a high-beta risk asset in the short run.

By contrast, bitcoin’s correlation with gold remained low, oscillating around zero throughout the period. While brief intervals of positive correlation emerged, they were neither persistent nor directional, underscoring that bitcoin has yet to consistently trade as a gold proxy over shorter horizons. Correlation with the U.S. dollar remained modestly negative, reflecting bitcoin’s partial sensitivity to the U.S. dollar, though the relationship remains low.

Looking beyond short-term dynamics, the longer-term correlation matrix highlights how limited these relationships are on average. Since 2011, bitcoin’s average three-month rolling correlation with U.S. equities has been just 0.15, with even lower correlations to developed and emerging market equities. Correlations with fixed income assets, commodities, real estate, and the U.S. dollar have been near zero.

THE EVENTS THAT SHAPED THE QUARTER

Bitcoin Hits a New All-Time High

Bitcoin entered Q4 with strong momentum and quickly established a new all-time high, breaking the $126K barrier. The rally reflected optimism around regulatory clarity, expanding ETF access, and deeper integration with traditional financial institutions. However, leverage and speculative positioning built rapidly beneath the surface, leaving the rally increasingly vulnerable to exogenous shocks, like the one with China tariffs. As has often been the case in prior cycles, marginal buyers relied heavily on derivatives rather than incremental spot demand.

A Tsunami of Liquidations

On October 10th, 2025 crypto markets experienced the largest liquidation event on record, with approximately $19 billion in futures positions forcibly unwound. The liquidation cascade accelerated downside momentum and triggered a broader risk-off dynamic across digital assets. Forced selling overwhelmed available liquidity, pushing prices lower than would have been implied by fundamentals alone. The episode once again highlighted the reflexive relationship between leverage and volatility in crypto markets.

DATs NAV Premiums Compress

Digital Asset Treasury (DAT) companies underperformed bitcoin during the quarter as equity premiums to NAV compressed and, in many cases, flipped to discounts. Liquidity unlocks, dilution concerns, and investor fatigue became increasingly apparent as prices declined. As sentiment deteriorated, investors reassessed the sustainability of business models predicated on persistent access to capital markets. The shift reinforced that DATs behave less like passive crypto exposure and more like vehicles leveraged to crypto prices.

Crypto ETFs Continue to Proliferate

The rollout of new crypto ETFs continued under the SEC’s revised commodity ETF listing standards. While BTC ETFs showed outflows to the tune of $1.1B during the quarter, the expanding product set underscores the rapid institutionalization of digital assets. At the same time, the growing number of vehicles has intensified competition for flows, with the new ETFs for SOL and XRP (amongst others) garnering $2.2B in inflows since launch during the quarter.

Crypto Pushes Deeper into TradFi

Integration between crypto and traditional finance advanced meaningfully. The CFTC approved regulated spot crypto trading on U.S. exchanges, JPMorgan allowed bitcoin and ether to be used as collateral, and U.S. Bank resumed crypto custody services, all incremental but structurally important developments. While these changes did not insulate markets from short-term volatility, they continue to lower barriers to adoption and embed crypto more firmly within existing financial infrastructure. Over time, this integration may alter both investor composition and market behavior.

Stablecoins and RWAs Grow, Banks Push Back

Stablecoin balances and tokenized real-world assets continued to expand throughout the quarter, highlighting demand for on-chain dollars and programmable financial infrastructure. At the same time, the banking industry remained hostile towards stablecoins despite the recent legislation, reinforcing the tension between innovation and regulatory conservatism. This divergence suggests that growth in crypto-native financial activity is increasingly occurring outside the traditional banking system. The gap may narrow over time, but for now it remains a defining feature of the market.

Gold Leaves Bitcoin Behind

The decisive outperformance of gold and silver over bitcoin was one of Q4’s defining narratives. While bitcoin remains a long-term monetary alternative, the quarter highlighted that its ‘digital gold’ thesis remains episodic rather than persistent. In periods of stress, capital continues to favor assets with longer track records and lower volatility. Bitcoin’s relative underperformance underscores that its role as a hedge remains highly context dependent.

2026 CRYPTO MARKET THEMES

With the new year upon us, we are highlighting some important trends that investors should keep an eye on for 2026. We’re not fans of “predictions,” especially for such a rapidly moving asset class (technology, market structure, regulations, etc.), rather we think that key topics for the coming year likely serves investors better than “called shots.”

1. Cycles vs. Secular Growth Remains the Key Question

Crypto enters 2026 still framed by the clash between repeating cyclical patterns and claims of long-term secular growth. Historical four-year cycles have dominated bitcoin’s price history, yet growing institutional adoption, regulatory clarity, and political support in the U.S. complicate simple analogies to prior periods.

While “cycles” is still the null hypothesis to be disproved, we offer another viewpoint. Rather than attempting to resolve the debate through market timing, investors should increasingly emphasize allocation strategies designed to withstand multiple regimes. The focus shifts from predicting cycle turns to structuring exposure that can persist through volatility, drawdowns, and extended consolidation phases. “Allocate, don’t speculate” is our suggestion.

2. Volatility Continues to Structurally Compress, but Tail Risk Persists

Long-term volatility in crypto assets, particularly bitcoin, continues to trend lower as market depth improves, derivatives markets mature, and institutional infrastructure expands. However, we expect volatility compression to be uneven and punctuated by episodic spikes driven by macroeconomic shocks, regulatory developments, leverage unwinds, and idiosyncratic crypto events. For institutional portfolios, crypto increasingly resembles other alternative assets: returns must be evaluated alongside drawdown behavior, liquidity under stress, and correlation dynamics. While the decline in volatility might be lamented by volatility sellers, the positive is that a much-reduced volatility makes it much more palatable for spot allocations, either in risk parity or even traditional portfolios.

3. Bitcoin Dominance in a Post-Narrative Cycle

We think market leadership in 2026 continues to consolidate around bitcoin, reflecting the industry’s shift away from narrative-driven expansion toward structural integration and institutional adoption. Bitcoin’s regulatory positioning, liquidity profile, and conceptual simplicity as “digital gold” make it uniquely compatible with balance-sheet allocation, collateral usage, and long-duration holding strategies. Innovation continues across the broader ecosystem, particularly among major Dapp platforms such as Ethereum and Solana. These networks not only support DeFi, one of crypto’s core use cases, but also enable asset issuance, tokenization, real-world assets (RWAs), and stablecoins, all of which we expect to see significant growth in 2026 and beyond.

4. Crypto Becomes a Balance-Sheet Asset, Not a Trade

Institutions increasingly approach crypto exposure as a balance sheet decision rather than a tactical trade. Considerations around custody, accounting treatment, financing, collateralization, and capital efficiency take precedence over short-term price moves. This shift reframes crypto as a treasury and risk-management asset, comparable to commodities or foreign exchange exposure, rather than a purely speculative instrument. As a result, the questions that matter most concern how crypto is held, financed, and governed over time, not simply when it is bought or sold.

5. TradFi and Crypto Integration Deepens Through Market Infrastructure

The integration of crypto into traditional financial systems continues to accelerate across custody, settlement, collateral management, and asset allocation. We think this trend continues in 2026 regardless of price action, which is very different than in 2022 where most major institutions shelved or scuttled their crypto initiatives amidst the industry downturn. Over time, the distinction between “crypto infrastructure” and “financial infrastructure” becomes increasingly blurred, even as asset-level risks remain distinct.

6. Stablecoins Emerge as Institutional and Payments Settlement and Liquidity Infrastructure

Stablecoins evolve beyond their origins as trading utilities (DeFi and offshore exchange quote currencies) into core institutional settlement and liquidity instruments. Adoption expands across payments, treasury operations, collateral transfers, and interbank movement, offering speed and programmability unavailable in traditional rails. As stablecoins scale, we expect the old guard to continue to push back with the fears of “banking reserve drainage.” Regardless of how that’s settled in legislation/regulation, we expect stablecoins to be increasingly viewed not as speculative assets, but as financial plumbing.

7. Tokenization and RWAs Drive Collateral Utility and Capital Efficiency

Tokenized real-world assets (RWAs), particularly government securities and money-market instruments, demonstrate some of the clearest product-market fit in crypto. In 2026, their importance extends beyond yield generation to collateral utility, financing efficiency, and balance-sheet optimization. Institutions increasingly value tokenized assets for their ability to move seamlessly across venues, integrate into risk systems, and support capital-efficient strategies. We think tokenization shifts from experimentation (the designs and approaches are still varied) toward practical deployment within existing financial processes.

8. DATs: Leveraged Crypto Exposure Forces Capital Discipline

Digital Asset Treasuries (DATs) continue to evolve as a distinct category, offering public-market exposure to crypto assets through corporate balance sheets. We expect these entities to trade as leveraged crypto beta, with equity returns dominated by underlying asset price movements. We expect DATs trading at persistent discounts to NAV to feel pressure on management teams to demonstrate capital allocation discipline, transparency, and shareholder alignment. Over time, these dynamics drive consolidation (we’ve already had 1 DAT M&A), governance scrutiny, and a clearer distinction between DAT business models.

9. Quantum Computing: Not an Immediate Threat, but Planning Begins

Quantum computing (QCs) is THE crypto risk for crypto investors now (it affects all of crypto, not just Bitcoin) and is likely to remain that way throughout 2026. While a crisis is far from imminent, QCs represent a long-term existential threat, and recent advancements are turning the relevant question from “if?” to “when?” We don’t expect 2026 to be the year in which the QC threat is real, but we do expect planning to begin in earnest. Numerous topics need to be researched and vetted — technology, economics, governance, to name a few. Don’t expect a QC fix to be fast or without contention, especially for Bitcoin, even if there are off-the-shelf solutions already available designed for a post-QC world.

10. Regulatory Clarity Continues to Benefit the Industry

Regulatory progress, driven by the market structure legislation but also around regulatory rule making and guidance, continues to reduce uncertainty for institutional participants, particularly around asset classification, custody, and intermediary oversight. This clarity enables greater participation by regulated entities, accelerating the growth of institution-facing crypto activity. At the same time, there are still unresolved questions around decentralized protocols that if not addressed, reinforce a bifurcated market structure. Regulated and permissionless crypto systems grow in parallel, with capital flowing between them under distinct constraints rather than converging into a single regime.