IN TODAY'S ISSUE:

- As we continue to look at factors affecting the recent sell-off, we look at what the rise in quantum computing fears had on bitcoin.

- Futures bases underscore a growing divergence in regional positioning between U.S. and offshore market participants.

- While the economic theory for prediction markets is strong, the practical implementation reveals a meaningful gap between concept and execution.

Quantum Computing: No Smoking Gun

Quantum computing (QC) is THE existential threat to bitcoin on every investor’s lips. In theory, Cryptographically Relevant Quantum Computers (CRQCs), quantum computers that could compromise current cryptographic standards, make this an important topic. However, market behavior does not support the view that quantum risk is driving bitcoin’s recent drawdown.

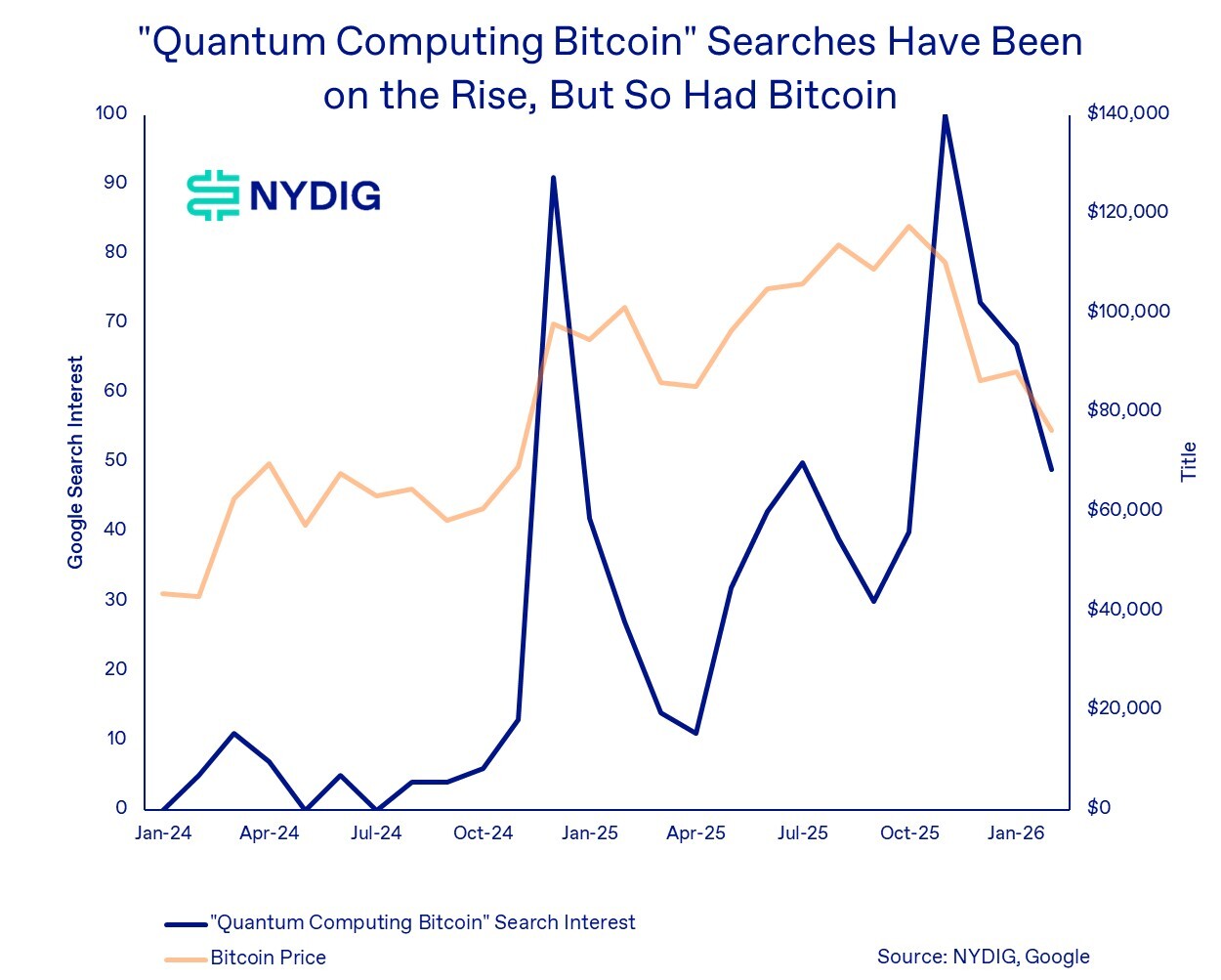

Our first piece of evidence is from Google Trends. Search interest for “quantum computing bitcoin” has risen, but notably this occurred alongside bitcoin’s rally to new all-time highs, not ahead of sustained weakness. In other words, heightened searches about quantum risk coincided with price strength rather than weakness. If the market were repricing bitcoin on an imminent technological threat, we would expect search intensity to lead or amplify downside risk, not accompany a period of gains.

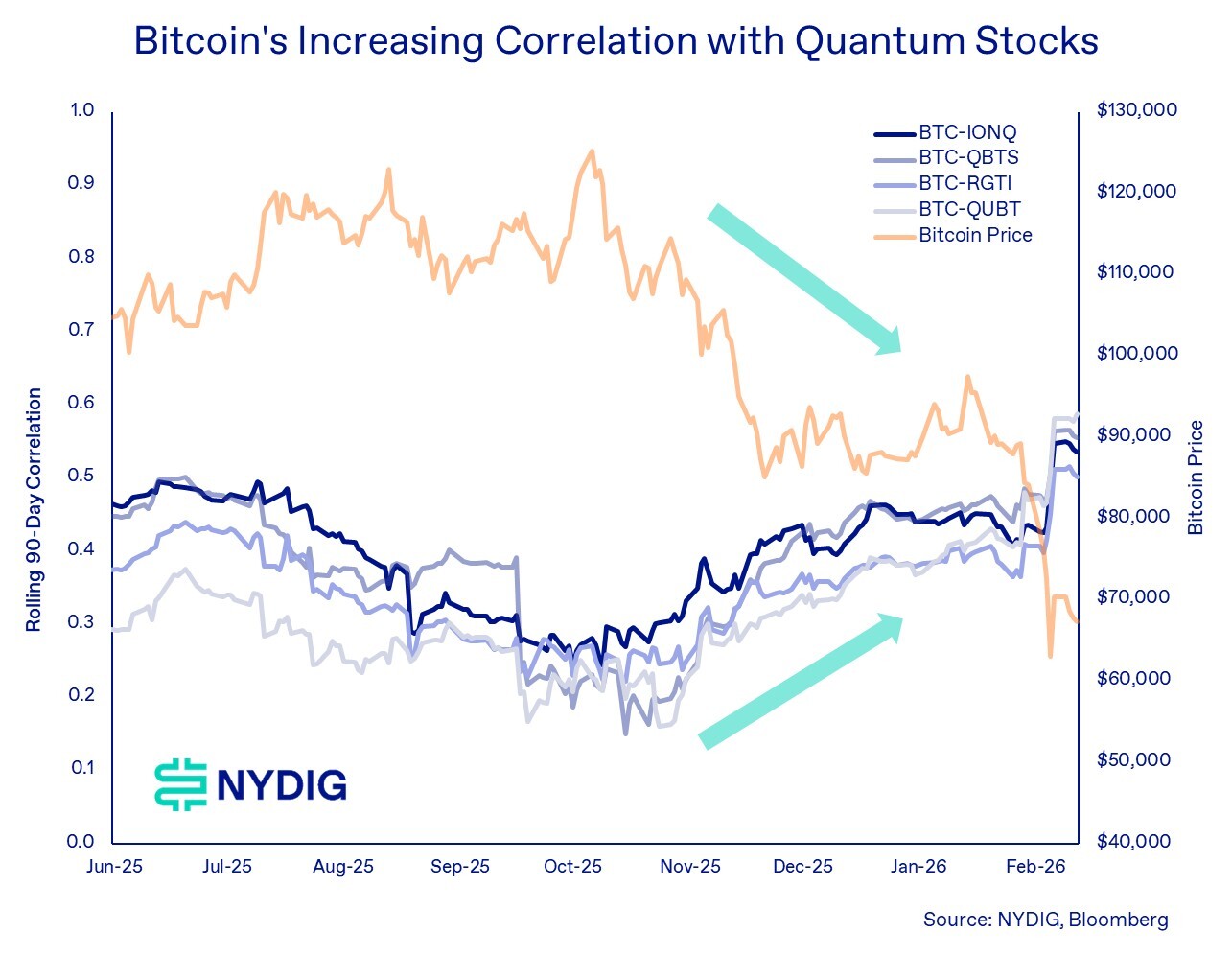

Our second piece of evidence is that bitcoin has been positively correlated with publicly traded quantum computing equities (IONQ, QBTS, RGTI, QUBT), and those correlations have strengthened during the recent drawdown. If quantum advances were eroding confidence in bitcoin, we would expect the opposite dynamic — QC equities appreciating as bitcoin declines. Instead, the assets have moved in tandem, with correlations rising through the selloff, pointing to a common factor rather than a causal relationship.

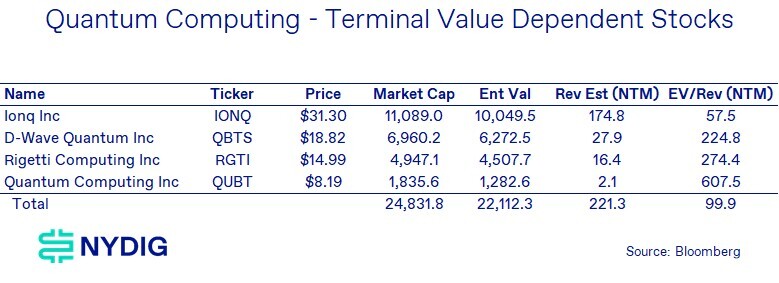

The common factor is likely risk sensitivity. Quantum computing companies are long-duration, expectation-driven assets: large enterprise values, minimal revenues, and high enterprise values (EV)/revenue multiples. Their valuations depend on terminal outcomes, much like bitcoin’s. When liquidity is abundant and investors are comfortable underwriting long-duration growth, both asset classes perform. When risk appetite contracts, both are repriced.

The data provides no evidence that quantum computing is the proximate cause of bitcoin’s weakness, even if it is the dominant risk narrative at the moment. The more plausible explanation is a broader macro repricing of risk across long-duration, expectation-driven assets. Bitcoin’s recent drawdown appears more consistent with shifts in overall risk appetite than with any discrete technological catalyst. Quantum risk remains a long-term consideration, but at present, the data does not support it as the driver of bitcoin’s decline.

Futures Basis Highlights Differing Geographical Attitudes Towards Bitcoin Price

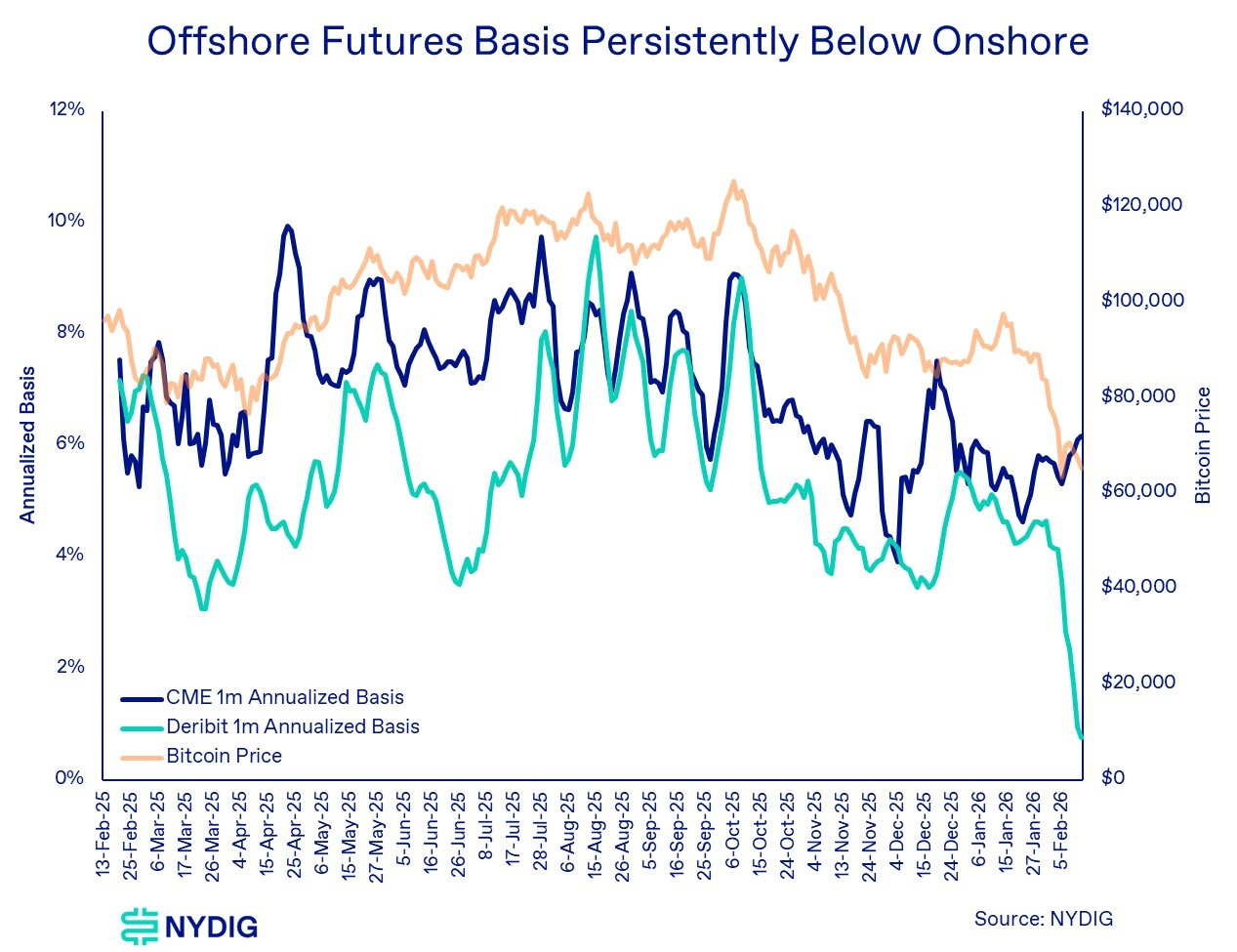

The divergence between onshore and offshore derivatives pricing has been an interesting read on regional attitudes towards the price of bitcoin. As shown in the chart, the 1-month annualized basis on CME (proxy for U.S. institutional positioning) has persistently traded above Deribit (proxy for offshore positioning). Structurally higher CME basis relative to Deribit implies that on-shore traders, including hedge funds, CTAs, and macro desks, have maintained a more constructive outlook compared to off-shore traders.

In addition, the sharp decline in Deribit 1-month basis indicates increasing caution among offshore investors. The more pronounced drop in offshore basis suggests reduced appetite for leveraged long exposure. The widening spread between CME and Deribit basis functions as a real-time gauge of geographical risk appetite.

Prediction Markets: Promise vs. Practical Application

“In theory, there is no difference between theory and practice. In practice, there is.” – Yogi Berra

One of the most notable financial innovations of the past several years has been the rise of prediction markets, platforms that allow participants to trade contracts tied to the probability of discrete future events (personally, I like the title “event markets” better, but no one asked me). Their recent acceleration has been closely associated with digital asset infrastructure, particularly as leading platform Polymarket operates on the Polygon blockchain and utilizes the USDC stablecoin for collateral and settlement. Regulatory clarity in certain jurisdictions has further legitimized the category, moving prediction markets from financial purgatory toward broader institutional awareness.

In theory, the economic case for prediction markets is compelling. They offer a mechanism for superior information aggregation by aligning financial incentives with accuracy. Market pricing converts dispersed knowledge into quantifiable probabilities, often updating in real time as new information emerges. This structure promotes transparency, accountability, and, in sufficiently liquid markets, improved forecasting accuracy relative to surveys or expert opinion. For institutional participants, prediction markets can function as risk management tools, allowing firms to hedge exposure to policy outcomes, regulatory decisions, macroeconomic events, or other uncertainties that materially impact portfolios or operating environments.

In practice, however, the realized composition of many prediction markets diverges from their theoretical utility. While certain contracts may provide economically meaningful signals, a substantial portion of market activity gravitates toward event-style speculation with limited social or financial relevance. Markets tied to celebrity behavior (number of Elon Musk tweets), entertainment outcomes (number of times the word “Tylenol” is said in a South Park episode), or other low-consequence events (length of the Super Bowl National Anthem) may generate trading volume but provide little in terms of economic hedging value or societal value. This distinction is important. While prediction markets can serve as powerful tools for information discovery and risk transfer, not all uncertainty warrants financialization.

Market Update

Bitcoin rebounded this week after finding support at $60K last Thursday evening. The subsequent rally from the oversold condition (14-day RSI hit 17) carried prices back through $70K before fading throughout the week, leaving BTC up 2.9% over the past 7 days. Consistent with this pattern, spot bitcoin ETFs recorded inflows in three of the past five sessions during the rebound phase, followed by renewed outflows as price momentum stalled, suggesting tactical dip-buying rather than sustained allocation.

Broader risk assets were comparatively stable. The S&P 500 and Nasdaq Composite posted modest gains. Gold continues to stand out, rallying 1.3% on the week as traders continue to take the asset back up after suffering a 20%+ drawdown a few weeks ago.

Derivatives and liquidity indicators suggest positioning in crypto remains muted. Perpetual swap funding rates and CME basis remained subdued following the selloff, indicating limited willingness to express directional views.

Aggregate stablecoin balances have remained broadly flat, suggesting there has not been a meaningful wave of sidelined capital re-entering the market, nor evidence of continued broad-based capital flight. Beneath the surface, however, composition has shifted. USDT balances have been declining, while supply growth has occurred in alternative stablecoins such as USDC, USD1, and PYUSD. This mix shift is incrementally negative for price action, as USDT remains the dominant quote currency across offshore venues and perpetual futures markets. A contraction in USDT liquidity may therefore imply reduced speculative capacity and marginal buying power in the segments of the market that tend to drive short-term price moves.

Taken together, the data points to a market that has stabilized from oversold conditions but has yet to show evidence of renewed structural risk appetite.

Important News This Week

Investing:

Bitcoin’s 24/7 Trading Risk Spikes While Wall Street Sleeps - Bloomberg

Here's How Market Makers Likely Accelerated Bitcoin's Brutal Crash to $60,000 - CoinDesk

Regulation and Taxation:

Crypto's Banker Adversaries Didn't Want to Deal in Latest White House Meeting on Bill - CoinDesk

Companies:

Trump-Linked World Liberty Financial to Launch Forex Remittance Platform - Reteurs

CME Explores Launching Its Own Coin as 24/7 Trading for Crypto Funds Nears - Decrypt

Upcoming Events

Feb 27 - CME expiry

Mar 11 - CPI release