IN TODAY'S ISSUE:

- DATs are making billion-dollar financing decisions based on inconsistent, loosely defined metrics, risking major strategic missteps.

- With several companies trading right around “1x mNAV," small changes in valuation methodology can flip capital-markets choices from “issue equity to buy BTC” to “sell BTC to buy back equity.”

- A full NAV framework exposes these distortions and delivers clearer, more accurate guidance for financing, dilution, and bitcoin-acquisition strategy.

Corporate Finance Decisions Shine a Light on DAT Metrics

This week, Strategy (MSTR) returned to the industry spotlight with the creation of a $1.44B “USD Reserve” (a fitting figure, given Bitcoin’s 144 blocks per day). Funded through sales of stock under its ATM program, the reserve provides a substantial cash buffer to meet dividend obligations on its preferred stock and convertible notes. In effect, the move reduces investor concerns about MSTR’s ability to service these obligations and has already helped lift the prices of several preferred issues. The company also added to its bitcoin holdings, bringing the total to an even 650,000 BTC.

MSTR simultaneously updated its guidance, released a new investor presentation, and held a call to discuss the developments. Our interpretation of the event was twofold. First, the company continues to highlight its preferred stock as a central tool in its bitcoin-acquisition strategy. This may be the area where it has achieved its most significant financial innovation within traditional market structures, something we've highlight before. Second, it plans to lean heavily on “mNAV," an industry-defined metric, when making capital markets decisions. If mNAV (industry-defined enterprise value to bitcoin value) exceeds 1.0x, MSTR will issue equity to grow its USD Reserve. If mNAV falls below 1.0x, the company would instead sell bitcoin, monetize bitcoin derivatives, or potentially lend out its bitcoin holdings.

Billion-Dollar Decisions Hinge on mNAV

Statements from DATs across the sector make it clear that mNAV remains a central metric, one that is actively shaping billion-dollar capital markets decisions. We’ve been openly critical of mNAV many times: its ambiguous definition, inconsistent application, lack of uniform industry standards, and questionable components make it ill-suited for decisions of this scale. We strongly prefer a comprehensive accounting of a company’s true net asset value (NAV) and a direct comparison to its equity value. As we illustrate in this note, that approach can lead to capital-markets decisions that differ dramatically from those implied by mNAV.

Dilution or No-Dilution? That is the Question

One of the most important questions investors and companies must first address is how to think about a DAT’s capital structure, specifically, how to handle share count. Bitcoin-native metrics such as mNAV and "bitcoin yield" have their foundations rooted in the concept of “bitcoin per share” (BPS), defined as a company’s bitcoin holdings divided by its share count. In industry practice, BPS is typically calculated using “assumed shares outstanding,” a non-GAAP measure that should include all potentially dilutive securities (convertible notes and preferreds, warrants, stock options, etc.). In theory, this produces the most conservative BPS figure (the lowest possible number), though independently verifying what constitutes “assumed shares outstanding” is notoriously difficult.

The challenge becomes more pronounced when applying derivative metrics. While DATs commonly use “assumed shares outstanding” (we refer to this as “fully diluted”) for BPS, many switch to basic shares outstanding when calculating market cap, "enterprise value", and mNAV. Basic shares exclude all potentially dilutive instruments. To derive "enterprise value," companies add the principal value of debt and preferreds to this basic-share market cap and subtract recently reported cash. We go a step further in our definition of enterprise value, however, and further subtract the fair market value of current bitcoin holdings and other investments, and cash. The purpose of calculating enterprise value is to estimate the theoretical cost to acquire the entire company, including all claims on its assets and liabilities. That’s why bitcoin holdings are subtracted.

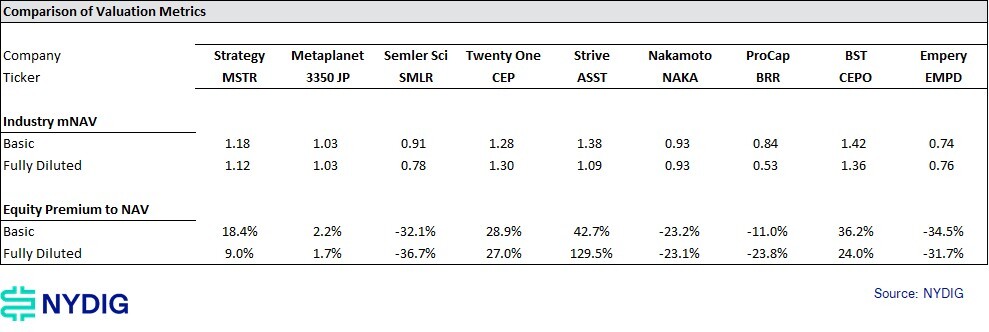

Basic vs Fully Diluted Measures Can Yield Very Different Capital Markets Decisions

Beyond the lack of industry-wide consistency in using basic versus fully diluted mNAV, an apples-to-oranges problem, these differences can produce sharply divergent valuations. For companies trading near the 1.0x mNAV threshold, the stakes are particularly high: the choice between issuing stock to buy bitcoin versus selling bitcoin to repurchase stock can hinge entirely on which share count methodology is used. In other words, the metric can drive capital-markets decisions in opposite directions. This is not merely theoretical. Several DATs are hovering around 1.0x mNAV.

NAV Calculations are More Stringent

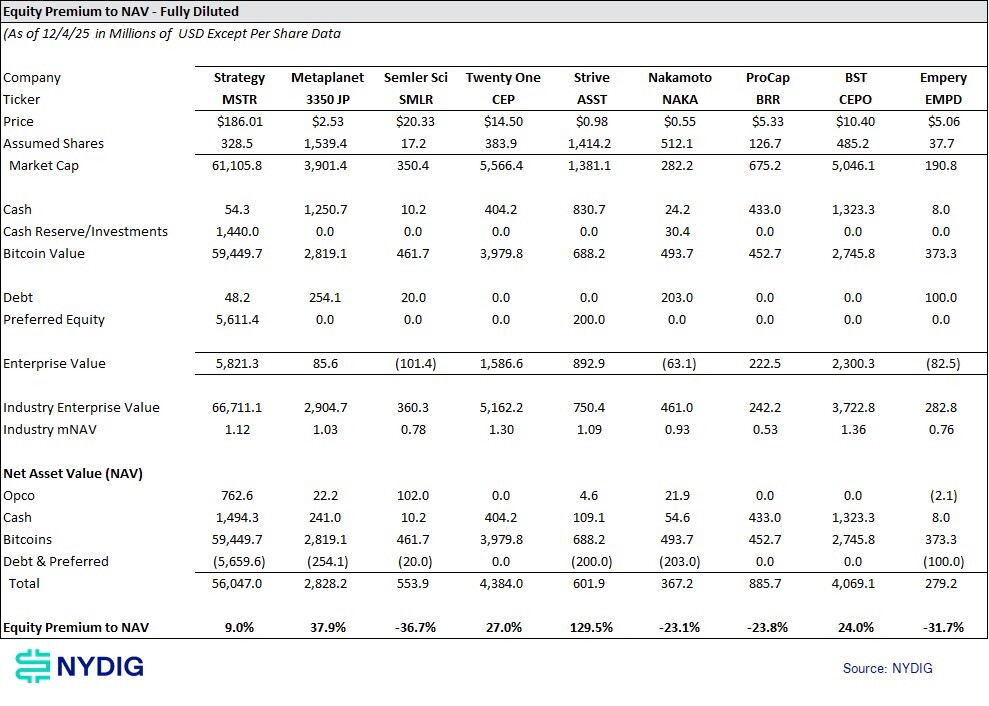

Naturally, there’s a substantial amount of work required even before you reach the basic-versus-diluted share count discussion. Keeping up with each company’s status, merger approvals, share registrations, and pro forma metrics is practically a full-time effort on its own. In the table below, we’ve done that work again (in a new format) and also calculated what we view as the most useful metric for capital-markets decisions: the Equity Premium (Discount) to Net Asset Value (NAV). NAV is a stricter measure than mNAV because it captures the full capital structure and all owned assets, including any operating business. Some DATs, like SPACs, have no operating company by design, while others, such as MSTR, have meaningful ones. For this analysis, we’ve used the enterprise value of the company as of the day before announcing the transition to a DAT or the acquisition of bitcoin. We acknowledge that some of these figures are now dated, so estimating the current value of the operating company would also be a reasonable exercise.

Excluding certain assets, such as cash, investments, or operating businesses, results in an understated NAV, which in turn produces inflated equity premiums relative to NAV or even mNAV. A company that believes it is issuing equity at a premium when it is not can easily end up making value-destructive financing decisions, especially since the discrepancies can be large (mid-single digit percentages) and the margin for error is small (several companies trading close to their NAV).

Treating Convertibles as Cash Obligations is Most Conservative

In the previous table, we’ve used basic shares outstanding and treated all potentially convertible debt instruments, such as convertible notes and convertible preferreds, as straight debt, accounted for in the total principal amount. This technique is perhaps the most stringent of measures and assumes that the debt will be repaid with cash, not share issuance. Cash repayment is a much more onerous requirement for DATs than share issuance. We’ve also treated all pre-funded warrants as basic shares, something not consistent across the industry, but the cash has already changed hands (and is part of the NAV), and the incremental cost to issue shares is trivial (fractions of a penny), and thus should be exercised by all holders.

Full Dilution Typically Reduces Premiums to NAV

But what if we treat all convertible obligations as equity issuance rather than cash repayment? In this approach, issuers could meet their debt obligations by delivering shares instead of cash. We exclude the principal value of convertible debt, assume the exercise of any warrants that are in the money relative to the current share price, and include the associated cash proceeds. This method is generally more favorable for issuers because the conversion premium embedded in convertible notes and preferred stock effectively allows the company to issue shares at a premium to NAV. That was a realistic option during the bitcoin bull market, but the subsequent downturn has cast doubt on this path; as a result, most convertibles in the sector now trade below their conversion price.

What’s interesting about the diluted-share approach is that it typically lowers enterprise value and therefore depresses premium-to-NAV and mNAV metrics, because the value of convertible obligations is “marked down” through the conversion premium. Counterintuitively, this means that the basic shares methodology is not the more conservative one. Instead of producing lower valuation outputs, it produces higher mNAV figures and higher premiums (or smaller discounts) relative to NAV.

Conclusion Remarks – Companies Should Use Basic Shares NAVs

The recent actions by Strategy underscore a broader truth about the DAT ecosystem: capital markets decisions are only as sound as the metrics guiding them. As the industry increasingly leans on mNAV to justify billion-dollar financing moves, the limitations of that metric — its inconsistent definitions, selective treatment of dilution, and exclusion of key balance-sheet realities — become more consequential. Our analysis demonstrates that basic versus fully diluted share methodologies can produce meaningfully different valuations and, in some cases, drive opposite strategic outcomes. For companies hovering near the critical 1.0x threshold, this can be the difference between issuing equity to purchase bitcoin or selling bitcoin to repurchase equity.

A more rigorous framework, one anchored in full NAV, offers clearer guidance. NAV forces a more thorough accounting of capital structure, operating businesses, investments, and all financial instruments. It avoids the distortions that arise when certain obligations are ignored or inconsistently treated and helps prevent value-destructive decisions born from overstated premiums or understated liabilities. As we show, whether convertible obligations are treated as debt or presumed equity can dramatically reshape a company’s apparent valuation and its perceived capacity to raise capital. Our recommendation is to use the basic shares methodology, but fully account for all assets and liabilities under a NAV framework.

Ultimately, the industry would benefit from moving toward more uniform, transparent valuation practices. Until that standard emerges, investors and issuers alike should remain vigilant: the choice of metric is not a technicality; it is a determinant of corporate strategy. In a sector where margins for error are thin and capital flows are large, precision in measurement is not optional.

Market Update

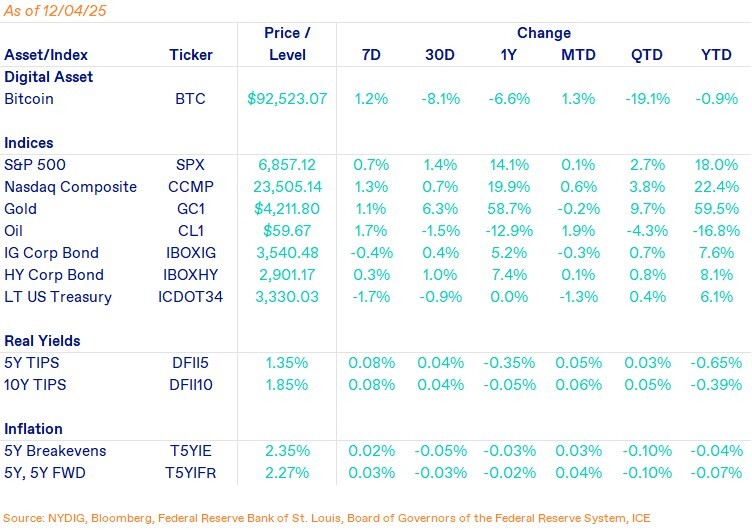

After a brief burst of BoJ–induced volatility early in the week, bitcoin regained its footing and surged back above $92,500, finishing the week up 1.2%. Despite the rebound, the broader crypto market remains divided on whether this is simply a pause in a longer secular bull run or a sign that momentum has cooled.

Against this backdrop, stablecoins and bitcoin ETFs returned to net inflows, an encouraging sign that capital is again rotating into crypto after a period of hesitation. Still, the contrast is hard to ignore. While equities and gold hover near their highs, bitcoin is flat on the year.

Whether this divergence signals late-cycle exhaustion or sets the stage for a catch-up rally will depend on bitcoin-specific catalysts. But for now, the message from the cross-asset landscape is clear: traditional markets continue to march higher while bitcoin, for the moment, is merely regaining its footing.

Important News This Week

Investing:

Vanguard to Allow Bitcoin, Ethereum and XRP ETF Trading in Major Crypto Pivot - Decrypt

Crypto Deals Hit a Record $8.6 Billion as Market Strains Grow - Bloomberg

Regulation and Taxation:

Acting Chairman Pham Announces First-Ever Listed Spot Crypto Trading on U.S. Regulated Exchanges - CFTC

Citadel Asks SEC to Regulate DeFi Protocols as Exchanges, Sparking Backlash - The Block

Bitnomial Announces Launch of First-Ever US Leveraged Retail Spot Crypto Exchange - Bitnomial

Companies & Technology:

Bitcoin and Quantum Problem - Part I - Nic Carter

Bitcoin and Quantum Problem - Part II - Nic Carter

Strategy Announces Establishment of $1.44 Billion USD Reserve and Updates FY 2025 Guidance - Strategy

Bitcoin-Focused Firm Twenty One Sees Public NYSE Listing on Dec. 9 - CoinDesk

S&P Downgrades Tether Rating - S&P

Upcoming Events

Dec 10 - FOMC interest rate decision