IN TODAY'S ISSUE:

- As the AI era accelerates, its effects on bitcoin are likely to be transmitted through macroeconomic channels, particularly via monetary and fiscal policy responses.

- The rise of AI agents is poised to reshape the payments industry, but incentives will still matter in an AI-driven economy.

- Circle likely outsources the remainder of its stablecoin reserves as the IQMM ETF shows huge inflows.

Bitcoin in the Age of AI

In case you missed it, this piece from Citrini Research made the rounds earlier this week. Written as a macro memo from the future, it looks back on the past two-plus years and the sweeping impact AI has had on society. Though framed as “not doomerism fan fiction,” it reads very much like the backdrop of a dystopian novel or film, one we’d gladly read or watch.

We encourage readers to go through it and draw their own conclusions, but the core argument is that the AI boom has profoundly reshaped the economy, society, and business, ultimately leading to a collapse in aggregate demand. The timing is inconvenient for markets: anxiety around AI’s effects is high, regulation remains (intentionally) absent, and equities are hovering near all-time highs. Adding fuel to the fire, after the close on Thursday, Block (formerly Square) announced it would reduce its headcount by 40% after installing AI tools.

AI Threatens Knowledge Work

Strip the fear of AI down to its core, and it’s this: it threatens knowledge work, the very engine of human activity and wealth creation since the Industrial Revolution. The promise to society has been: work hard, earn good grades, get a strong education, and you’ll secure economic stability. That has already begun to break for many following the formula, however, something we’ve highlighted before, most recently in Speculation and the War for Attention.

But what if it’s not just fraying? What if it breaks entirely? That’s the anxiety AI provokes, and the scenario Citrini lays out. Employment, wages, ability to service debt and prop up asset prices collapse. What ensues is a cataclysm in aggregate demand — deflation on a scale society has never seen.

There are Historical Precedents

Here’s the thing about this type of technology: we’ve been here before. The steam engine replaced human and animal labor with mechanical power, centralizing production and driving industrial scale. Electrification, a true general-purpose technology, went further. It didn’t just power factories, it reorganized the economy. Productivity initially lagged, but once workflows, capital stock, and institutions adapted, output surged. Labor unrest followed mechanization; electrification brought corporate and labor reform. Yet demand did not collapse. Higher productivity translated into higher output and higher GDP. Tasks changed. Jobs evolved.

AI is more analogous to electrification than steam. It is not simply a tool layered onto existing processes; it requires workflow redesign, new skills, and complementary investment. Technology historically displaces tasks, not total labor demand. The transition may be volatile and uneven, but history suggests that general-purpose technologies expand productive capacity rather than extinguish it.

The AI Implications for Bitcoin

If AI is a general-purpose technology akin to electrification, its relevance to bitcoin is not technological but macroeconomic. Such technologies reshape employment, economic growth, real rates, global liquidity, and risk appetite. Bitcoin is downstream of those forces, and ultimately, the determining variable is how AI and the policy response change those factors.

If AI-driven growth occurs alongside expanding liquidity and contained real rates, that backdrop can be supportive for bitcoin. But if stronger growth lifts real yields, tightens policy, and reduces the need for monetary accommodation, bitcoin may face headwinds. Conversely, if AI generates labor disruption or volatility that prompts fiscal expansion and easier monetary policy, the resulting liquidity impulse would likely favor bitcoin.

Final Thoughts

One final note. The arc of human civilization is defined by adaptation. Time and again, through industrial revolutions, world wars, financial crises, pandemics, and technological upheavals, societies have confronted disruptions that appeared existential in the moment. Yet the prevailing pattern is triumph, not collapse. Institutions reform. Businesses reorganize. Labor markets re-skill. Incentives realign. The human instinct is to compete, adapt, and overcome, not to concede obsolescence.

AI will pose challenges, but they are unlikely to break from that historical pattern. Like steam power and electrification before it, AI changes relative advantage. Firms that integrate it effectively will widen margins and productivity gaps. Workers who adapt will enhance their relevance. Those who resist may fall behind. The transition may be uneven and volatile, but technological shifts have consistently rewarded adoption over avoidance.

The implication is not that disruption will be painless, but that the equilibrium response to new technology has historically been integration, not obsolescence. Society's response to AI will likely follow the same pattern.

Payments, AI Edition

One section of the Citrini piece that merits particular attention is agentic payments, an emerging model in which AI agents autonomously initiate and route payments using stablecoins. Coinbase’s recent launch of Agentic Wallets enables AI systems to hold digital wallets and transact via the x402 standard, facilitating payments without human intervention. This concept echoes one of Bitcoin’s earliest visions: machine-to-machine payments. While that thesis did not materialize, stablecoins and embedded wallet infrastructure powered by AI may now make it viable.

The opportunity is compelling: real-time, automated payments across digital services and machine-driven payments (assuming one could overcome the risks of allowing AI access to your finances). That said, it is premature to conclude, as the Citrini piece implies, that incumbent payment networks, especially credit cards, face an imminent collapse in revenue. There are important structural dynamics within crypto and payments that investors should carefully consider before extrapolating such outcomes.

Credit Cards Offer Benefits

Payment networks are two-sided markets, with merchants and consumers. For merchants paying roughly 2–3% in interchange fees, the appeal of stablecoins is clear: margin improvement.

For credit cards, the constraint is on the consumer side. Cardholders are incentivized through rewards and access to revolving credit. Stablecoin payments, on the other hand, require prefunded balances and offer no embedded credit function. They also offer no rewards. Absent comparable incentives or financing mechanisms, consumers have little reason to migrate. Note: credit cards are just one way to move money.

That is not to suggest that agentic payments and stablecoins lack meaningful potential. To ignore them would be foolhardy. However, displacing payment rails like consumer credit cards, with their embedded incentives and financing features, is likely to be more difficult than the piece assumes.

Circle Likely Outsources the Management of the Remainder of its Reserves

Last week, the launch of the ProShares GENIUS Money Market ETF (IQMM) drew significant attention after generating $17 billion in first-day trading volume. For context, this is approximately 70% higher than IBIT’s largest single trading day on record. After just one week, IQMM claims to be the largest money market ETF, although traditional money market mutual funds remain substantially larger.

Volume declined meaningfully after the first day, suggesting the initial surge was likely driven by a pre-arranged allocation, most likely from a stablecoin issuer. Our guess is Circle. The fund’s prospectus states that it is designed to qualify as a reserve investment for payment stablecoin issuers under the GENIUS Act.

Circle already outsources the majority of USDC reserve management to BlackRock. BlackRock manages the Circle Reserve Fund and oversees roughly 90% of USDC’s dollar-denominated reserve assets (excluding bank deposits). In other words, Circle has already embedded its reserves within traditional asset management infrastructure.

Allocating $17B to IQMM, just over 9% of Circle’s total reserves, would represent the remaining portion not currently managed by BlackRock. This move would further institutionalize reserve management while aligning the balance sheet with emerging stablecoin-specific regulatory frameworks.

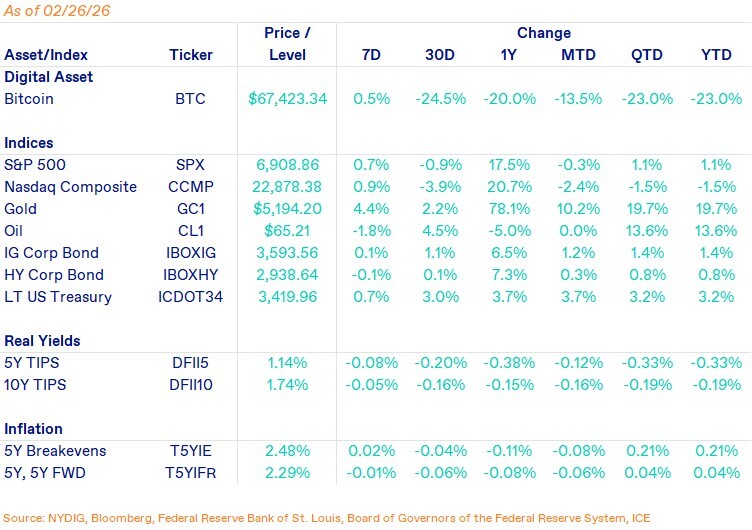

Market Update

Bitcoin finished the week essentially flat (+0.5%), continuing the recent pattern where rallies are quickly sold. Attempts to build momentum higher have repeatedly run into overhead supply, reinforcing $70K as a key psychological and technical resistance level. Midweek strength coincided with a sharp rally in Circle’s stock following its earnings announcement, which provided a constructive backdrop for sentiment more broadly. Even so, spot bitcoin was unable to sustain a breakout.

From a flows and positioning standpoint, spot bitcoin ETFs saw solid inflows, taking in over $900 million across the past five trading days. Despite this steady bid, derivatives positioning remains notably muted. Perpetual swap funding rates have stayed subdued, offshore futures open interest (measured in bitcoin terms) has been trending sideways since the October 10th liquidation event, and CME basis remains in the mid-single digit percent. Together, these signal limited speculative froth and a lack of aggressive directional positioning. In short, while spot flows are constructive, the absence of expanding leverage helps explain bitcoin’s continued difficulty in breaking decisively through resistance.

Equities were modestly higher on the week, with the S&P 500 up 0.7% and the Nasdaq Composite gaining 0.9%. Early-week sentiment was weighed down by the Citrini note, which cast a pall over risk assets, but markets ultimately stabilized and ground higher.

Gold was back in vogue, rising 4.4% on the week and continuing its strong year-to-date performance. The move higher comes alongside declining real yields (5Y and 10Y TIPS lower on the week), reinforcing the macro bid for hard assets.

In commodities more broadly, oil declined 1.8%. The divergence between gold and energy highlights a more nuanced macro environment: safe-haven demand appears firm, while growth-sensitive commodities remain mixed.

Important News This Week

Regulation and Taxation:

OCC Issues Notice of Proposed Rulemaking for GENIUS Act - OCC

U.S. Regulator's GENIUS Pitch Casts Dark Cloud Over Crypto Sector's Stablecoin Model - CoinDesk

Investing:

Tracking Bitcoin's Flows - CF Benchmarks

The 2026 Global Intelligence Crisis - Citadel Securities

Companies:

Jane Street Accused of Insider Trading That Helped Collapse Terraform - WSJ

Binance Fired Staff Who Flagged $1 Billion Moving to Sanctioned Iran Entities - WSJ

MrBeast Editor Nabbed by Prediction market firm Kalshi for Alleged Insider Trading - CoinDesk

Tether Says it Has Frozen $4.2 Billion of its Stablecoin Over Crime Links - Reuters

ZachXBT Exposes Group of Alleged Axiom Insider Traders - Protos

AI Agents Want to Identify Your Crypto Wallet Using Social Media - Protos

Bitdeer Sold all its Bitcoin to Fund its Move into AI Data Centers - CoinDesk

Coinbase Partners with Yahoo Finance as it Opens Stock Trading to all US Users - The Block

Upcoming Events

Mar 11 - CPI release

Mar 18 - FOMC interest rate decision