IN TODAY'S ISSUE:

- Comparing the 2021 - 2022 cycle versus the current drawdown.

- The growing TAM for unmined bitcoins?

- Implications as crypto transitions from an alternative financial system to one embedded in TradFi.

A Look Back at the 2021 - 2022 Drawdown and Comparisons to Today

Past crypto cycles are top of mind right now. First, it is the sixth anniversary of one of, if not the worst, liquidation/sell-off events in crypto history: Black Thursday, March 12, 2020. If you didn’t experience it, or did and just want to experience some PTSD, Coin Metrics published excellent write-ups on the event (here and here). The summary of the event is that the onset of the COVID-19 health care and economic crisis rippled through markets, causing a 40% decline in the price of bitcoin, which didn’t end until BitMEX, the dominant derivatives exchange at the time, was (fortunately?) knocked offline by a DDoS attack.

Second, there was the recent lawsuit in which the administrator of the Terraform Labs bankruptcy, the company behind the ill-fated Terra (LUNA) and TerraUSD (UST) token and algorithmic stablecoin ecosystem, sued trading firm Jane Street, alleging it helped trigger the collapse of those tokens. The failure of LUNA/UST evaporated roughly $60 billion in crypto wealth, on par with the collapse of Lehman Brothers, becoming a primary catalyst behind the broader market meltdown in 2022.

The case prompted a surprising number of questions. While we have already spilled plenty of ink criticizing the LUNA/UST design in the past, and the courts will ultimately decide the merits of the lawsuit, it brought back events of that year and how the current drawdown is unfolding. There are several important lessons from that episode that may still help guide investors today.

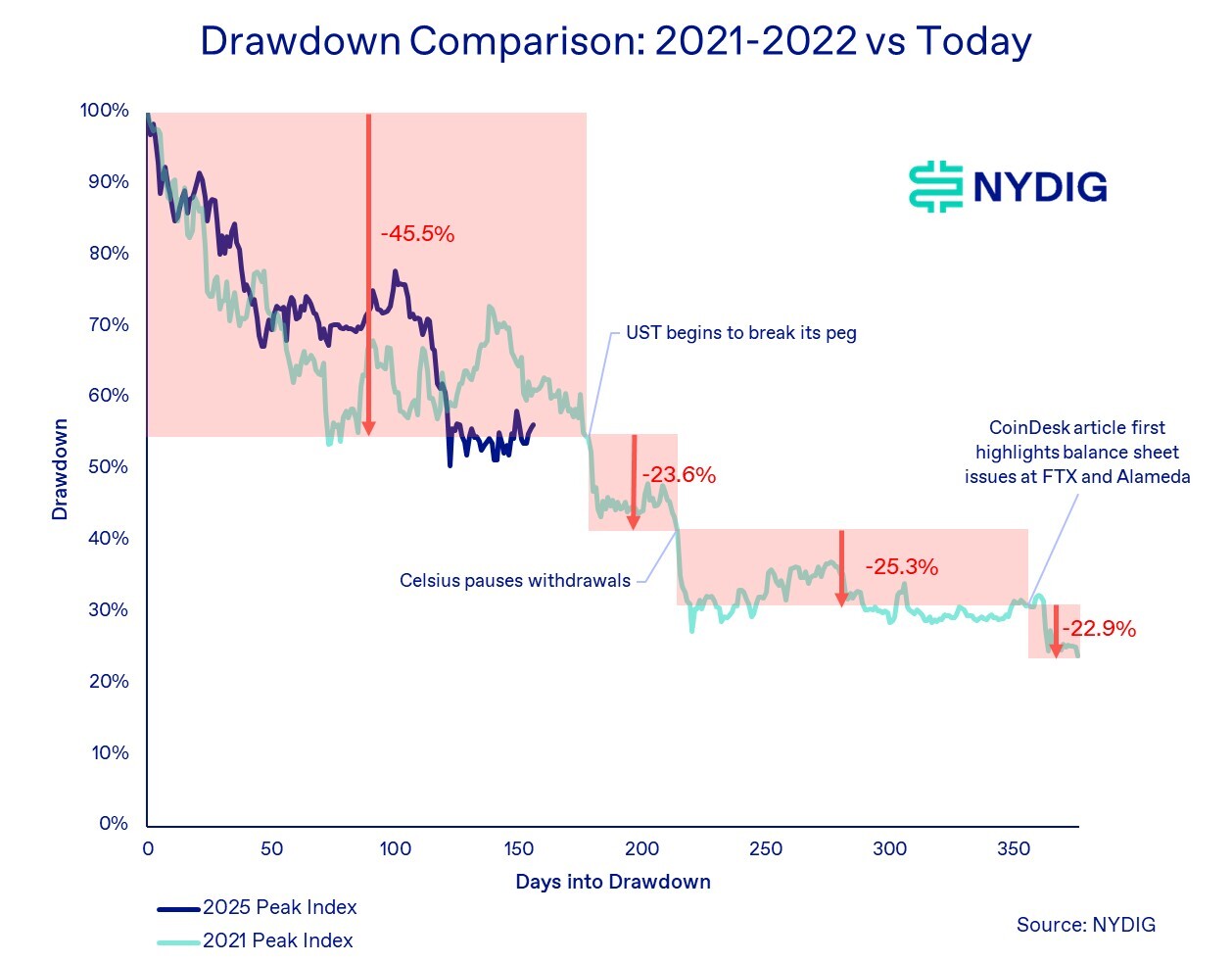

First Part of the 2021 Drawdown

The first observation is that the initial drawdown, following bitcoin’s $69K peak in November 2021, just ahead of the launch of the ProShares Bitcoin ETF (BITO), largely reflected profit-taking rather than structural stress. The launch of BITO clearly helped propel bitcoin to a new all-time high. Front-month CME basis briefly rose above 35%, highlighting the extent of speculative demand at the time.

From that peak, bitcoin fell roughly 45.5%, which in hindsight was a fairly typical correction following a cycle top. During this period, there were a couple of notable incidents, most prominently the Wormhole and Ronin bridge hacks in February and March 2022, which together totaled about $950 million. Trading volumes were declining, collateral values were falling, and questionable lending and business practices were already underway across parts of the ecosystem. But importantly, no core market infrastructure had broken yet.

Structural Collapse Followed in 2022

What followed in 2022 was a cascade of failures across crypto market infrastructure, beginning with the rapid collapse of LUNA/UST in early May 2022. At the time, LUNA was the 6th largest non-stablecoin cryptocurrency, while UST was the 3rd largest stablecoin and the 10th largest crypto asset overall (historical snapshots on CoinMarketCap are always fun). At their peak, the two accounted for roughly $60 billion in combined market value.

After UST first “broke the buck,” bitcoin fell another 23.6%. The next shock came with the unraveling of the crypto lending sector, beginning with Celsius pausing withdrawals in June 2022. Bitcoin subsequently declined another 25.3%, then traded sideways for a period as markets digested the fallout from additional failures, including Voyager and Three Arrows Capital.

The final leg lower, another 22.9% drawdown, came after reports of balance sheet issues at FTX in early November, which ultimately triggered the exchange’s collapse and marked the last major phase of the 2022 downturn before the market eventually bottomed.

Today: A Familiar First Phase, But Damage Could Be Limited

The early phase of the drawdown following the 2021 peak looks very similar to where we find ourselves today, a roughly 52.5% decline from the cycle high of $126K on October 6 to a low of $60K on February 6. While prices have fallen sharply, there has been little evidence of systemic breakage. Aside from the failure of Blockfills, which left a relatively small $75 million hole in its balance sheet by industry standards, the core infrastructure of the market has largely remained intact.

That’s why we continue to watch closely for incidental damage across the ecosystem. So far, however, there has been little sign of broader systemic stress surfacing beyond the Blockfills situation.

If additional pressure fails to materialize, this drawdown could ultimately prove less severe than the 2021 - 2022 downturn. The comparison isn’t perfect, however. Previous cycle drawdowns occurred even without widespread infrastructure failures. That said, business practices across the industry appear more disciplined this time around, which could help limit the risk of cascading failures if conditions deteriorate further.

Bitcoin’s Shrinking Available Supply, but Growing TAM?

This week marked the mining of Bitcoin’s 20 millionth coin. With that milestone, only 1 million bitcoins remain to be created, which will be issued gradually over the next 114 years. While it took just over 17 years for the network to produce the first 20 million coins, the remaining 1 million will not be fully mined until around the year 2140, reflecting Bitcoin’s steadily declining issuance schedule.

What’s interesting about this dynamic is that even as the number of coins left to be mined steadily declines, the dollar value of that remaining supply, measured as the remaining coins multiplied by the current bitcoin price at the time, has continued to rise over time. That outcome is somewhat counterintuitive given the shrinking supply of future issuance.

To be clear, we wouldn’t read too much into this, as the metric largely tracks bitcoin’s price. Still, it is not necessarily what one might expect at first glance, particularly as many bitcoin miners are increasingly diversifying into secularly growing compute-intensive industries such as HPC and AI. Nonetheless, it is an interesting way to frame the economics of the remaining supply.

Crypto’s Next Phase is About TradFi Integration

Crypto is increasingly shifting from an alternative financial system to one that is embedded within traditional financial infrastructure, with several recent developments illustrating this transition. Kraken’s banking arm received a limited Federal Reserve master account, Nasdaq announced a partnership with Kraken to develop tokenized equities, and Intercontinental Exchange (ICE), parent of the NYSE which is developing its own tokenized securities platform, made a strategic investment in OKX as part of a broader effort to integrate on-chain infrastructure with traditional trading, custody, and settlement systems. Taken together, these items suggest that crypto is rapidly integrating with the core plumbing of capital markets rather than operating alongside it.

Stablecoins and Payments Expanding Rapidly

The same dynamic is unfolding in payments and stablecoins just as rapidly. Stripe, Circle, PayPal, Visa, and Mastercard are all building infrastructure that integrates stablecoins into existing merchant and settlement networks. In most cases, stablecoins are not replacing traditional payment systems but instead becoming a new settlement layer beneath them, enabling faster cross-border transfers, programmable payments, and globally interoperable liquidity.

Stripe is integrating stablecoins into checkout, subscriptions, and billing APIs, while also developing its own blockchain payment infrastructure, Tempo, designed to support multi-chain stablecoin settlement and programmable payments directly within its merchant platform. Circle is expanding beyond issuing USDC by building dedicated infrastructure for financial institutions, including the Circle Payments Network (CPN) and its Arc blockchain, which are designed to facilitate bank and fintech settlement using stablecoins.

Meanwhile, PayPal has embedded its PYUSD stablecoin into its wallet and merchant ecosystem, allowing users to send, hold, and transact with stablecoins within PayPal and Venmo. At the network level, Visa and Mastercard are enabling issuers and payment partners to settle transactions on-chain across multiple blockchains, effectively integrating stablecoins into the global card infrastructure. Together, these initiatives suggest that the largest payments companies are not just supporting stablecoins as assets but are increasingly building the blockchain infrastructure themselves, reinforcing the trend of crypto rails becoming embedded within traditional financial networks.

Other fintech platforms are beginning to move in the same direction. Block (Square/Cash App) CEO Jack Dorsey, long focused on bitcoin infrastructure, has recently indicated that merchant demand for stablecoins is increasing. Meanwhile, fintech platforms such as Klarna and SoFi are exploring their own stablecoins or blockchain settlement systems, suggesting that tokenized dollars may increasingly become a standard component of modern financial infrastructure, rather than a niche crypto product.

Integration, not Substitution

For institutional investors, the implication is that the opportunity is shifting away from purely speculative crypto assets toward the interfaces between digital asset rails and traditional finance: tokenized securities markets, stablecoin payment infrastructure, and software platforms that enable machine-to-machine commerce. Crypto’s first phase built an alternative system; the next phase is about integration, as blockchain-based settlement gradually becomes part of the financial system’s underlying infrastructure.

Implications for Investors

For institutional investors, the opportunity in digital assets is increasingly shifting to the infrastructure that connects blockchain-based settlement with traditional financial markets. Some of that is happening on open permissionless Dapp platforms, such as Ethereum and Solana, but much of it is happening on private or permissioned blockchains and infrastructure. This suggests that long-term investment opportunities may concentrate in a smaller set of assets, including select tokens that capture value through transaction fees or have significant asset issuance on their platforms, as well as centralized organizations building and operating core infrastructure. As a result, the investable universe in crypto may narrow over time, a trend we have previously highlighted, reflected in bitcoin’s growing market dominance and the relative absence of a broad altcoin cycle in the last market cycle.

Market Update

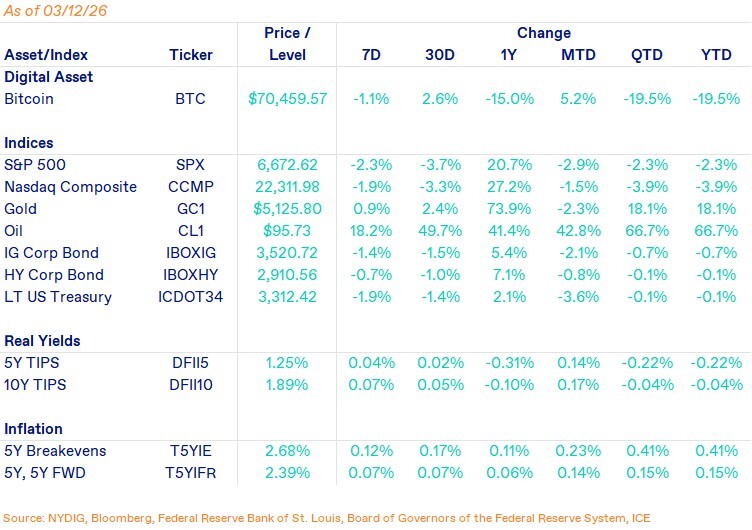

Bitcoin traded lower through the first half of the week before recovering in the back half, finishing the period down 1.1% on the week but still up 5.2% month-to-date. While no clear fundamental catalysts were driving the rebound, the price action suggests that the wave of marginal sellers that pressured the price to $60K in early February may be largely exhausted.

Derivatives markets also point to stabilization. CME futures basis has continued to firm modestly, while perpetual swap funding rates remain slightly negative. Together with offshore futures open interest holding broadly flat in bitcoin terms, this suggests positioning remains cautious and that the recent rally has not been driven by aggressive long leverage.

Flows and liquidity conditions across the broader crypto ecosystem remain constructive. Bitcoin ETFs saw steady but relatively small inflows during the trading week. Total stablecoin balances continue to rebound, driven primarily by growth in USDC, with USDT beginning to show early signs of growth as well after a period of stabilization.

Macro conditions remain mixed. Gold rose modestly on the week, while oil prices remain elevated at $95, even after pulling back from the recent spike near $120 amid the ongoing conflict in Iran. Energy markets continue to signal geopolitical risk and potential inflation pressures. Meanwhile, U.S. equities declined and real yields moved modestly higher, creating a somewhat less supportive backdrop for risk assets broadly.

Important News This Week

Investing:

Regulation and Taxation:

SEC, CFTC End Years of Rivalry with Deal That Will Mean Combined Crypto Oversight - CoinDesk

Wall Street Banks Weigh Lawsuit Over Crypto Banking Charters - Decrypt

Companies:

Strive Announces SATA Enhancements and Purchase of Bitcoin - Strive

Binance, PayPal, And Ripple Join Mastercard’s Massive New Push into Blockchain Payments - CoinDesk

Asia’s Biggest Bitcoin Buyer Now Wants to Build the BTC Ecosystem - CoinDesk

Utexo Raises $7.5M Led by Tether to Launch Native USDT Settlements on Bitcoin - Chainwire

Bitcoin Die-Hard Jack Dorsey Doesn't Like Stablecoins, But Block Will Use Them Anyway - Decrypt

Stablecoin Firms Bet Big on AI Agent Payments That Barely Exist - Bloomberg

Nasdaq Partners with Kraken Parent Payward to Link Tokenized Equities with Defi Networks - The Block

Upcoming Events

Mar 18 - FOMC interest rate decision

Mar 27 - CME expiry

Apr 27 - Bitcoin 2026 conference