IN TODAY'S ISSUE:

- Increased competition for attention and capital from an increasingly supply of speculative markets is likely weighing on interest for bitcoin and crypto at large.

- Individuals are increasingly willing to spend their time and money on short-duration, low-probability, high-payoff activities, which have broader implications for society.

- As attention becomes a binding constraint, assets like bitcoin that benefit from long holding periods face near-term headwinds despite unchanged long-term investment characteristics.

Speculation and the War for Attention

I read an article this week that closely aligned with themes I’ve been considering for some time (Bloomberg article link). The central takeaway is that a key reason bitcoin and broader crypto markets have underperformed recently, despite seemingly supportive macroeconomic and geopolitical conditions, is the emergence and growth of alternative speculative markets. These venues have increasingly diverted attention and capital that historically would have flowed into crypto.

There are three important trends here:

- The growing supply of speculation markets.

- The increasing societal demand for speculation activities.

- Increasing speed of markets

The combination of these things, which have been playing out for years now, are an important marker of not only financial markets, but societal trends.

Speculation Market Supply

Over the past 5 – 10 years, the supply of speculative markets has expanded materially. Online sports betting, online casino gambling, in-game live wagering, leveraged single-stock ETFs, ultra-short-dated options, and prediction markets have all grown, driven by a combination of market demand and regulatory liberalization.

These venues compete primarily for short-duration, high-risk capital seeking rapid feedback and asymmetric outcomes. Because price formation is driven by marginal buyers and sellers, the availability of these alternatives has implications for crypto markets, which historically absorbed a meaningful share of this speculative demand. As incremental risk-seeking capital and investor attention are redirected to other venues, activity within crypto, particularly in its higher-beta segments, can soften, weighing on liquidity, volatility, and price discovery.

Within crypto markets, this competition is most evident in areas associated with so-called “degen” activity. Memecoin trading, leveraged perpetual swaps, airdrop farming, recursive leverage, memecoin sniping, and yield farming represent speculative segments where attention and capital now face increased competition from alternative speculative outlets. While these segments are not synonymous with crypto, they have historically contributed to reflexivity and momentum across the broader market.

This distinction is important when evaluating bitcoin. While some observers characterize all crypto activity as speculative due to the absence of traditional cash flows, there remains a meaningful difference between speculation and investing. Speculation, in our view, is generally a negative expected-value activity. Over time, outcomes converge toward loss. “The house always wins,” is the old gambling adage. Investing, by contrast, benefits from time and compounding.

Traditional markets illustrate this dynamic clearly. The S&P 500 can be used as a speculative vehicle through short-dated strategies such as 0DTE options, yet extending the holding period allows investors to capture the index’s long-term return. The same framework applies to bitcoin. While bitcoin can be traded speculatively, its historical performance over longer holding periods more closely resembles an investment asset. Investors who have held bitcoin for more than five years have never realized a loss.

Speculation Market Demand

Over the past 10 – 15 years, demand for speculative activity has seemingly increased materially, not only in how individuals allocate capital, but also in how they allocate time and attention. A common feature across these activities is a preference for short-duration, low-probability, high-payoff outcomes.

In financial markets, this shift is evident in the growing participation in activities such as those mentioned previously, as well as meme stock trading, options trading among retail investors, communities like WallStreetBets, and even billion-dollar lottery participation. While these activities differ in form, they share a similar payoff profile: limited downside per attempt, low probability of success, and highly skewed potential returns.

A parallel shift is observable in how individuals allocate their time. There appears to be an increasing willingness to participate in “winner-take-most” activities, which are characterized by power-law income distributions where a small number of participants capture a disproportionate share of economic rewards. These markets are typically driven by scalability, network effects, and tournament-style compensation structures, where relative rank and small differences in performance or visibility can lead to large differences in economic outcomes. Historically, this would include acting, music, and professional sports, but now includes streamers, social media influencers, podcasters, and online content creators, to name a few. This stands in contrast to traditional professions, where earnings tend to follow a more normal distribution. Are there rockstar accountants? Sure, their income and productivity are constrained by location and productivity, plus the average accountant is probably doing ok, while the average Twitch streamer is probably not.

High Speed Markets

A third, related trend is the increasing speed of markets. Across both financial and non-financial domains, technological advances have compressed the time between decision, outcome, and feedback. Markets now increasingly offer near-instant resolution, continuous engagement, and rapid reinforcement, whether through real-time sports betting, ultra-short-dated options, high-frequency crypto, or algorithmically optimized content platforms.

This acceleration matters because speed shapes behavior. Faster markets reward immediacy, reflexivity, and repetition. It penalizes patience and long-duration decision-making. As a result, speculative activities with rapid feedback loops become more salient and engaging than investments whose payoff is realized over years rather than minutes or days.

In financial markets, these dynamics disadvantage assets like bitcoin that, while capable of being traded at high frequency, are best suited to be held over long periods of time. As attention and capital increasingly gravitate toward faster, more reactive markets, slower-moving investment theses struggle to compete for mindshare, even when their long-term return characteristics remain intact.

More broadly, the increasing speed of markets reinforces a preference for short time horizons across both capital and labor allocation, further amplifying demand for lottery-like outcomes and winner-take-most pursuits.

Societal Implications

When combined, rising speculative demand and increasingly high-speed market dynamics carry broader societal implications. There is growing skepticism that effort, persistence, and initiative reliably translate into upward mobility. The traditional notion of the “American Dream,” that success and prosperity are attainable through sustained effort regardless of background, appears, for many, increasingly out of reach. In its place, success is increasingly perceived as contingent on rare, outsized outcomes rather than cumulative effort.

Taken together, this shift carries important societal effects. As belief in effort-based mobility erodes, the perceived returns to education, apprenticeship, and long-term skill development become increasingly uncertain. Trust in institutions, including education systems and labor markets, declines as they lose credibility as reliable pathways to economic prosperity.

This environment favors shorter time horizons, reinforcing preferences for near-term outcomes over sustained investment in human capital. Creativity and effort are increasingly directed toward visibility-driven platforms, where success depends more on attention than cumulative productivity. Over time, these dynamics contribute to greater dispersion in outcomes and reinforce reliance on low-probability, high-payoff paths, despite their unfavorable expected value.

Final Thoughts

Taken together, the expansion of speculative market supply, rising demand for lottery-like outcomes, and increasing market speed help explain recent dynamics across financial markets and society more broadly. These forces do not invalidate the case for long-term investing, but they materially alter the environment in which it competes. Asset performance increasingly reflects not only fundamentals and macroeconomic conditions, but also how marginal capital and investor attention are allocated across an expanding supply of alternatives.

In this environment, attention has emerged as a binding constraint. Markets that offer continuous engagement and immediate feedback attract speculative participation, even when expected returns are unfavorable. As a result, marginal risk-seeking capital is increasingly absorbed by faster, more reactive venues, reducing participation in long-term investments such as bitcoin.

This dynamic represents a near-term headwind for bitcoin, not because its long-term investment thesis has deteriorated, but because its payoff profile increasingly competes with high-speed speculative alternatives in an attention-constrained market environment.

NYDIG State of Bitcoin Update (Video Update)

The State of U.S. Crypto Regulations

In this episode of The NYDIG Bitcoin Update, a new feature we've started, Ben Lawsky (Head of Regulatory Affairs) dives deep into the evolving U.S. crypto regulatory landscape, including the stalled market structure bill, stablecoin implementation challenges, and shifting agency dynamics. We assess what recent setbacks mean for regulatory clarity, industry momentum, and the path forward amid growing political time pressure.

Market Update

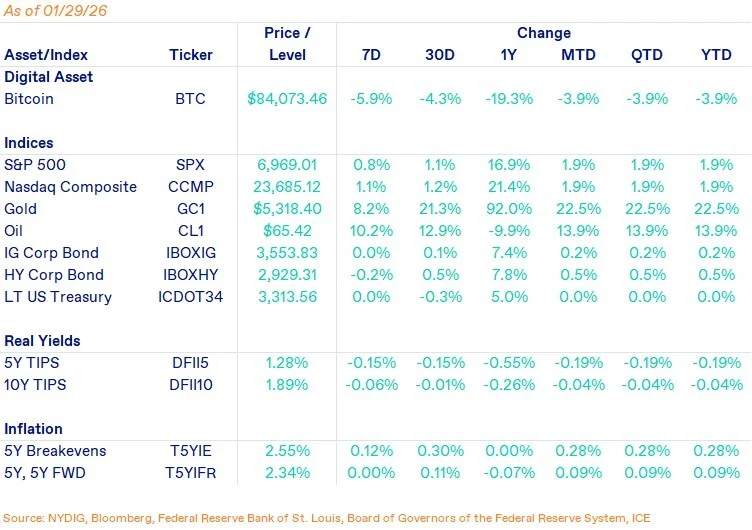

Bitcoin continued to struggle this week, declining 5.9%, despite broader risk assets moving higher. U.S. equities posted gains, with the S&P 500 up 0.8% and the Nasdaq Composite rising 1.1%. Gold, although it sold off following the announcement of noted hawk Kevin Warsh, still finished the week up 8.2%. The U.S. dollar was notably weak, with the DXY Index down 1.3% through Thursday before stabilizing after news of Warsh’s nomination.

Positioning stress was evident in derivatives markets. Approximately $850 million in long bitcoin futures positions were liquidated from Thursday into Friday amidst weak price action. While funding rates were not elevated by historical standards, the drawdown to $81K had a pronounced impact on leveraged traders. Funding rates briefly turned negative, indicating increased demand for short exposure, before bouncing back to near zero.

CME futures pricing further underscores the lack of speculative appetite. The annualized basis on front-month contracts for ETH and SOL is below that of BTC, signaling limited willingness to move out the risk curve into higher beta assets. Notably, absolute BTC basis levels are already subdued, 4 - 5%, indicative of broad trader apathy. Under more typical conditions, ETH basis would trade above BTC, with SOL above ETH. The current inversion reflects an unusually high degree of risk aversion.

Spot ETF flows remain a meaningful headwind. Since January 15, the day after bitcoin reached $98K, spot bitcoin ETFs have experienced persistent outflows. In aggregate, nearly $2.7 billion has exited the complex, including more than $800 million in outflows yesterday alone. Flows, however, remain uneven across products. Month-to-date, IBIT has recorded net inflows of approximately $392 million, despite consistent outflows over the past two weeks, while FBTC has seen nearly $850 million in net outflows during January.

Current stablecoin dynamics also reinforce the idea of a cautious backdrop. Despite a sharp jump in the supply of World Liberty Financial’s USD1 stablecoin, likely driven by incentive programs on Binance, with much of the issuance held there, the total supply of stablecoins has declined. After rebounding from the October 10 liquidation event, aggregate stablecoin supply has fallen roughly 4%, or $12.6 billion, since mid-January. Combined with ETF outflows, the data suggest a net withdrawal of liquidity from digital asset markets, rather than rotating internally.

Despite weak price performance and market internals, the broader macroeconomic and political backdrop remains supportive for an asset like bitcoin. With few non-sovereign stores of value globally available to investors, especially at the scale of bitcoin, it is likely a matter of time before capital re-enters the ecosystem.

Important News This Week

Investing:

Gold In “Extreme Greed” Sentiment as It Adds the Entire Bitcoin Market Cap in One Day - CoinDesk

It’s Like the GBTC Premium, But in Chinese Silver - Protos

Bitcoin Slides Toward Longest Monthly Losing Streak Since 2018 - Bloomberg

Regulation and Taxation:

Statement on Tokenized Securities - SEC

White House Set to Meet with Banks, Crypto Companies to Broker Legislation Compromise - Reuters

Companies:

Bitcoin Block Time Slows as Sweeping US Winter Storm Strains Power Grid, Prompting Miner Curtailments - The Block

World Liberty Financial's USD1 Tops $5B Market Cap - Decypt

Upcoming Events

Feb 9 - 13 - Bitcoin Investor Week

Feb 11 - CPI release