IN TODAY'S ISSUE:

- Investors should think of Strategy as a bitcoin-backed capital-markets vehicle, not a passive BTC proxy, with MSTR and STRC acting as the flywheel.

- MSTR trading above 1.0x mNAV (premium to NAV) and STRC trading at/near $100 are the key variables to determine whether Strategy turns from a BTC accumulator to a BTC seller.

- The balance sheet is well covered, with roughly $54.9B of BTC plus cash against $22.2B of debt plus preferred claims, but STRC near $90 keeps preferred issuance expensive, and MSTR is not yet trading at a large premium to NAV.

- The $6.7B convert put calendar makes Strategy a refinancing story. The LUNA/UST analogy does not hold because BTC, not MSTR equity, is the collateral asset backing the structure.

Strategy: The Bitcoin-Backed Capital Markets Flywheel Meets Its First Real Test

We have framed Strategy as something more specific than a levered bitcoin proxy: it is a bitcoin-backed capital market access vehicle that turns market confidence into incremental bitcoin accumulation, in a flywheel-like mechanism. That distinction matters because the company’s value creation does not come only from owning 847,363 BTC. It comes from repeatedly converting security-level premiums into more BTC per share. This is something that came into sharper focus this week with a big strategic update from the company.

The flywheel has 2 core mechanisms: MSTR common equity must trade above 1.0x mNAV (a premium to NAV) and STRC preferred equity must trade near $100. When those conditions hold, Strategy can issue common or preferred capital, buy bitcoin, increase BTC per share, and reinforce the market premium that made issuance possible. When those conditions fail, the same structure becomes liquidity-consuming because management must defend the instruments that fund accumulation with the asset backing them, bitcoin.

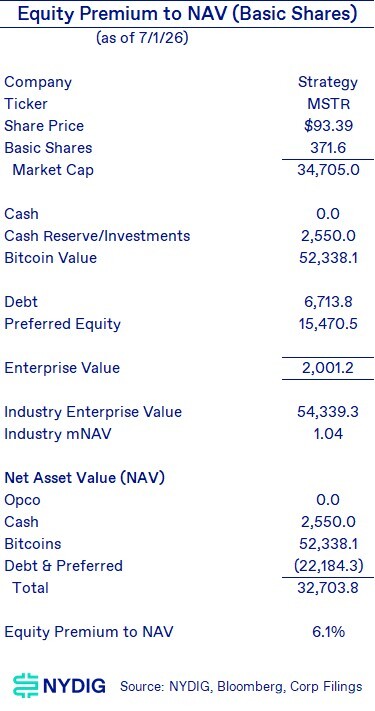

The current facts show a flywheel that is not broken but is struggling. As of July 1, MSTR closed at roughly 1.04x mNAV, a 6.1% equity premium to NAV, which technically reopens the common-equity channel but leaves only a narrow margin for accretive issuance. STRC has rebounded from a low of $74 and now trades around $90, which leaves the preferred-equity channel impaired at present time.

The Market Is Asking the Wrong Question

The first question for traditional investors should not be whether Strategy has sufficient asset coverage at today’s BTC price. At current bitcoin prices, the company’s BTC holdings are worth about $52.4B, and cash of $2.55B lifts total assets to roughly $54.9B. Against debt plus preferred claims of roughly $22.2B, the structure has about $32.7B of “surplus” NAV before any liabilities are not covered by existing assets.

That asset coverage is substantial, but it is not the critical constraint. The constraint is whether Strategy can maintain access to capital markets at prices that make bitcoin accumulation accretive rather than dilutive. MSTR above 1.0x mNAV is the price signal that determines whether common issuance adds BTC per share. If STRC trades below $100, Strategy can still raise capital, but each dollar raised creates more preferred claim and more dividend burden, which weakens the capital stack rather than cleanly funding BTC accumulation (higher cost of capital).

The current setup is therefore a market-access problem, not a solvency problem. MSTR at 1.04x mNAV tells us the common engine is open, but the window is narrow. STRC at roughly $90 tells us the preferred engine is still below the level required for clean par funding.

Why MSTR And STRC Are the Flywheel

MSTR common equity is the first engine because it monetizes the market’s willingness to pay above BTC-backed NAV. When MSTR trades above 1.0x mNAV, issuing common stock can be accretive because proceeds can buy BTC at spot while equity is sold above the value of the underlying BTC exposure. With NAV around $32.7B and market cap around $34.7B, MSTR currently embeds about $2B of premium value (equity it can issue to buy BTC or set aside for cash). That cushion is positive, but it is not large. The common engine is functioning, technically, but the spread is thin.

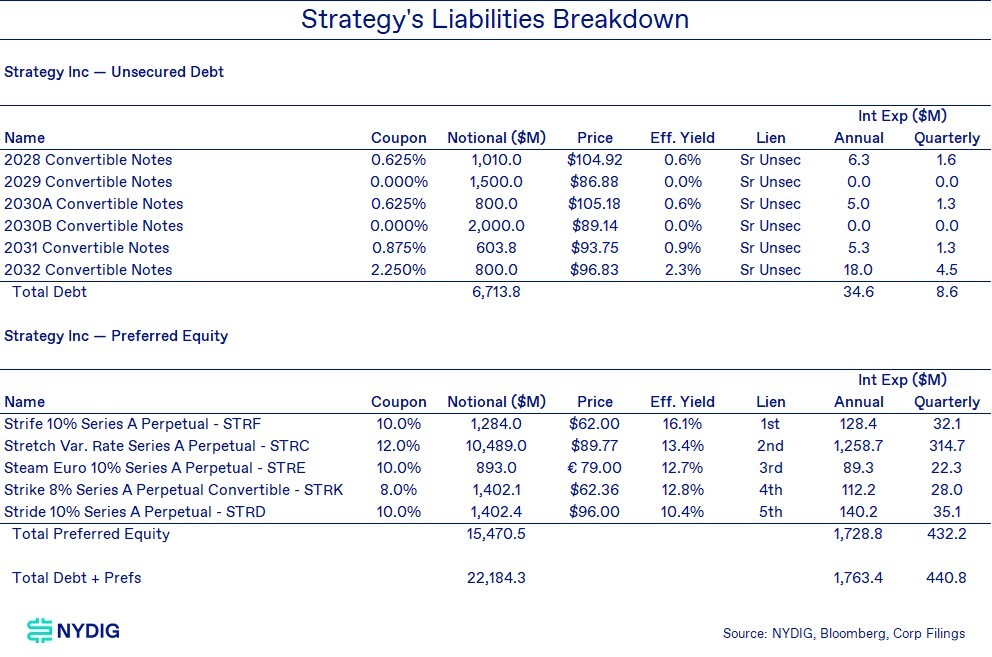

STRC is the second engine because it is the scalable preferred instrument in the capital stack. STRC has roughly $10.5B of notional, which is about 68% of the preferred equity stack and carries roughly $315M of quarterly dividends, which is about 70% of the company’s total quarterly interest and dividend payment. That size makes STRC the center of gravity for non-common equity capital markets funding.

STRC needs to trade near $100 because par-level preferred issuance is the cleanest route to raising capital. Strategy can technically issue STRC below par, but doing so raises the cost of capital to the market-implied effective yield. At $90, Strategy would raise $90 against a $100 preferred claim and pay a $12 annual dividend, which means BTC is effectively funded at roughly 13.3% before fees rather than the stated 12.0% rate. That discount matters because issuing below par raises the effective cost of capital and undermines the flywheel that transforms issuance into BTC ownership.

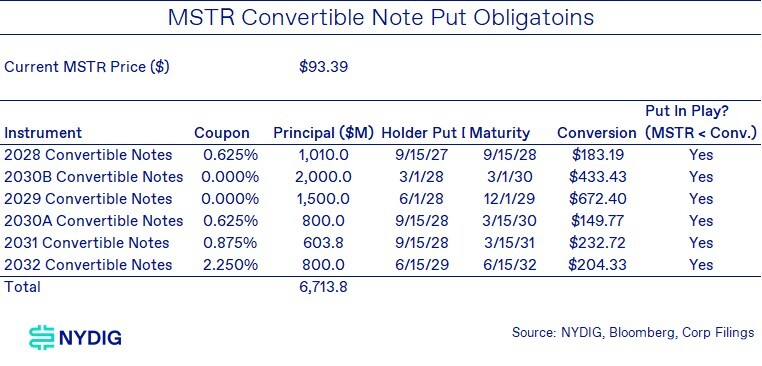

The Convert Put Calendar Is a Refinancing Test

The convert stack turns Strategy from a simple NAV story into a capital-market access story. Total convertible principal is roughly $6.7bn versus $2.55bn of cash, so cash covers only 38% of potential put principal if holders require redemption.

That gap does not have to become a cash drain, though. Strategy can issue a new convert series to take out existing obligations, provided investors accept the new coupon, conversion premium, tenor, and put structure. This is the cleanest path because it preserves cash, avoids BTC sales, and extends the maturity profile.

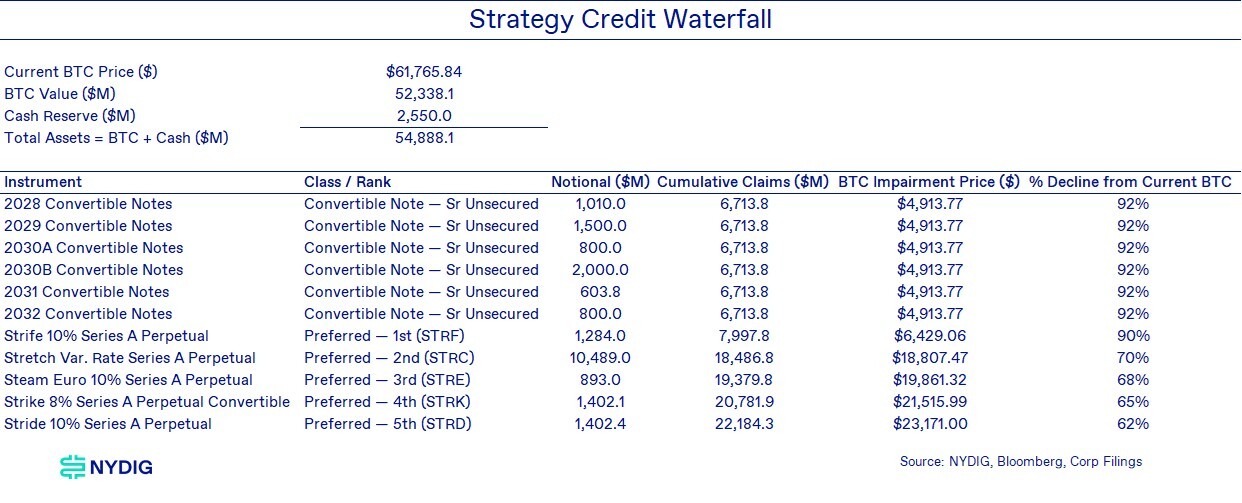

The issue is timing, not asset coverage. Senior debt impairment occurs only around $4,914 per BTC, or roughly 92% below the current BTC mark, so the convert risk is a refinancing risk rather than a solvency risk.

The key pressure point is 2028, when roughly $4.9bn of convert principal becomes puttable, equal to about 192% of the current cash reserve. The first $1.0bn put arrives in 2027, and another $0.8bn follows in 2029.

This is why capital-market access matters before the put dates arrive. MSTR above 1.0x mNAV supports common issuance, STRC near $100 supports preferred issuance, and an open convert market allows Strategy to roll the stack directly. If all 3 channels are impaired, Strategy becomes more reliant on BTC monetization, reserve drawdown, liability exchanges, or secured financing.

The Digital Credit Capital Framework Is a Price-Support Toolkit

The company’s recent framework should be read as a mechanism to defend capital-market access rather than as a conventional liquidity reserve announcement. The $2.55B cash reserve covers roughly 17.4 months of current preferred dividends and interest, which gives investors a clearer runway for scheduled cash obligations. The authorized $1.25B BTC monetization capacity extends that runway if external markets are unavailable. The $1.0B STRC repurchase authorization gives management a tool to buy discounted preferred instruments, while the $1.0B common repurchase authorization gives management a tool to defend MSTR when it trades near NAV.

Those tools target the flywheel’s market prices. STRC must recover toward $100 for preferred issuance to become a repeatable BTC funding channel. MSTR must stay above 1.0x mNAV for common issuance to be accretive. The reserve and buyback tools are therefore less about today’s asset coverage and more about preventing a market-access spiral.

The key trade-off is that BTC has become both the end asset and the treasury tool. Selling limited BTC to build reserves or stabilize funding instruments can be rational if it restores issuance channels that later buy more BTC than was sold. Selling BTC repeatedly to service the liability stack would change the thesis, because the asset base would be funding the structure rather than compounding through it.

The Structure Is Well-Collateralized but Market-Access Dependent

The market often collapses Strategy into a single BTC beta instrument, but the capital stack now requires a more precise framework. BTC plus cash of roughly $54.6B covers debt plus preferred claims of roughly $22.18B by about 2.46x, which supports the view that current pricing is not about immediate liquidation risk. The preferred waterfall reinforces that point because STRC impairment begins around $18,807 per BTC, or roughly 70% below the current BTC mark.

The problem sits in market access rather than collateral value. MSTR’s 6.1% premium to NAV is enough to reopen common issuance, but not enough to support indiscriminate issuance. STRC’s 10% discount to par keeps the largest preferred funding channel below the level required for efficient issuance. Convert puts totaling $6.71B create a refinancing calendar that cannot be solved by asset coverage alone.

This combination creates a sharper institutional framing: Strategy is a well-collateralized issuer whose growth rate depends on the market prices of its own securities. In traditional-market language, the company’s securities are not only liabilities and equity; they are operating inputs. MSTR and STRC prices determine whether the company can manufacture incremental BTC exposure on favorable terms.

Why The LUNA/UST Analogy Is the Wrong Collateral Framework

Some pundits have compared MSTR, STRC, and BTC to LUNA/UST because both structures contain reflexivity, but the comparison does not hold. In LUNA/UST, the stabilizing asset was endogenous. Confidence in UST depended on the market value of LUNA, and LUNA’s market value depended on confidence in UST. When confidence broke, the collateral mechanism weakened at the same time the liability needed support.

Strategy is structurally different because the collateral asset is BTC, not MSTR. MSTR common and STRC preferred are funding instruments, while BTC and cash are the reserve assets supporting the balance sheet. That distinction matters because MSTR can trade below mNAV and STRC can trade below $100 without immediately impairing the collateral base, provided BTC remains liquid and valuable. The reflexivity is still real, but it operates through capital-market access rather than an endogenous redemption loop.

The right institutional framing is that Strategy is a well-collateralized issuer with reflexive funding channels, not a LUNA/UST-style structure where the equity token itself functions as collateral. The risk is not that MSTR must be created to defend STRC in a circular peg mechanism. The risk is that weak MSTR, weak STRC, and a closed convert market could force Strategy to use BTC and cash defensively rather than use capital markets offensively to accumulate more BTC.

What Traditional Investors Should Track

The first variable is MSTR mNAV, because common issuance requires a premium above 1.0x. The current 1.04x reading is constructive, but the narrow premium means issuance discipline is essential. A durable premium above 1.1x would create a materially larger common-equity funding window.

The second variable is STRC price, because the preferred engine requires proximity to $100. STRC at $90 indicates that the preferred market is still demanding a discount despite reserve support and dividend adjustments. A move toward $99-$100 would be the cleanest signal that the preferred channel has reopened.

The third variable is the convert put calendar, because $6.7B of principal across 2027–2029 creates a liquidity test before final maturity. The 2028 wall of roughly $4.9B is the most important date cluster because it exceeds the current cash reserve by nearly 2x. That timing means the company must preserve capital-market access before the calendar forces liquidity decisions.

The fourth variable is quarterly cash burden, because the company has roughly $441M of quarterly interest and preferred dividends. The $2.55B reserve covers about 5.8 quarters of that burden, which buys time but does not remove the need to refinance, issue, repurchase, or monetize assets selectively.

What Bitcoin Investors Should Understand

For bitcoin investors, the relevant shift is that Strategy’s BTC accumulation is now inseparable from traditional capital-market confidence. The company can own a large amount of bitcoin, but BTC-per-share (BPS) accretion depends on whether investors are willing to fund the structure through MSTR and STRC at favorable prices. Bitcoin is the collateral base, but capital markets are the accumulation mechanism.

The distinction matters because BTC sales are no longer unthinkable inside the framework. A limited sale used to defend STRC, strengthen reserves, or protect MSTR’s funding premium can support long-term accumulation if the flywheel restarts. A recurring sale program used to cover preferred dividends, convert puts, or market-support costs would weaken the bitcoin accumulation thesis.

Bitcoin investors should therefore watch the same variables as credit and equity investors. MSTR above 1.0x mNAV means common issuance can add BTC per share. STRC near $100 means preferred issuance can add BTC without common dilution. Convert puts that remain refinanceable mean BTC does not have to become the primary liquidity source.

Final Thoughts

Strategy’s current challenge is not that the company lacks bitcoin collateral. The challenge is that bitcoin collateral must support a capital structure whose market prices determine whether the company can keep accumulating bitcoin accretively. That makes MSTR and STRC the flywheel mechanisms, while the convert put calendar is the clock.

The company is therefore operating in a narrow but still viable corridor. MSTR at 1.04x mNAV keeps the common engine alive, but STRC at $90 keeps the preferred engine constrained. The $6.7B convert put calendar requires the company to have market access before liquidity timing becomes the dominant issue.

For institutional investors, the clean formulation is that Strategy is no longer just a bitcoin exposure vehicle. It is a bitcoin-backed capital markets platform whose performance depends on whether security-level premiums can be maintained long enough to refinance obligations and compound BTC per share. The structure works when market access funds bitcoin accumulation. The structure struggles when bitcoin must fund market access.