IN TODAY'S ISSUE:

- As crypto treasury companies continue to expand, intriguing puzzles have started to emerge.

- Option limit increases for bitcoin ETFs may further suppress volatility but make them more appealing to own on a risk-adjusted basis.

- The implications of in-kind orders for the spot ETFs for investors and market participants.

The Art of the (Crypto Treasury) Deal

Crypto treasury companies have emerged as one of the enduring themes of the current cycle. While the concept was pioneered by Strategy (MSTR) in 2020, it didn’t gain meaningful traction outside of a few corporates (Tesla, SpaceX, Block) until mid-2024, despite Strategy’s eye-popping stock performance after its adoption. The latest wave, led by firms like Metaplanet and Semler Scientific, propelled the model into broader relevance beginning a year ago. Today, this emerging “industry” includes dozens of publicly traded companies across various geographies, backed by a diverse range of assets.

Simplistic in Design

While these companies have approached the market with different approaches and backers, their structures are fairly simplistic at a high level. These corporations issue equity and debt instruments, then use the proceeds to buy their preferred treasury crypto asset. One metric that has been popularized to judge a treasury company’s effectiveness has been crypto holdings per share and change in crypto holdings per share (“yield”). The idea for equity holders is that every share they hold should be worth more of the specified treasury crypto asset, like bitcoin.

The Only 3 Ways to Create Yield

How does a treasury company increase its crypto holdings per share or generate yield? While crypto treasury companies like to make this sound more complicated than it is, there are only three mechanisms: 1) issuing stock at a premium to NAV and using the proceeds to buy crypto 2) issuing debt (including converts and preferreds) or using excess cash or income from operations to buy crypto 3) generating crypto denominated returns using active treasury management (selling options, lending, staking, liquidity providing, basis arbitrage, directional trading/market timing, etc.). That’s it. To the extent that these companies are “monetizing volatility,” as some like to think, they do that by selling convertible notes or preferreds, which inherently have a call option on the equity in them, that derives its value from the stock volatility. Some of these corporate presentations compare what they are doing with the titans of finance and technology throughout the centuries, overplaying what they are doing, to put it mildly.

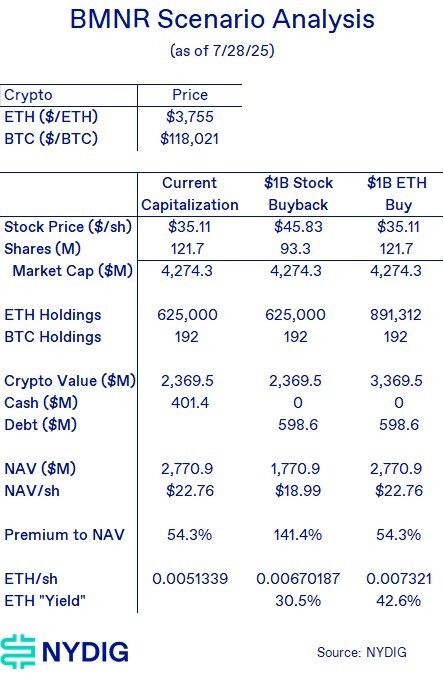

BMNR Announces Stock Repurchase

While corporates have been tripping over themselves rushing to issue equity and debt to hoover up more crypto, this week we saw the first crypto treasury stock repurchase announcement. On Tuesday, Bitmine Immersion Technologies (BMNR), which is mostly an ETH treasury company (some BTC too), announced a $1B stock buyback, aiming to use ~$400M in excess cash on hand and presumably issuing $600M in debt to fill in the rest. The odd thing, at first glance, is that the stock had closed the previous day’s trading not at a discount to NAV as once might suspect, but at a 54.3% premium to its NAV of $22.76/sh.

Because the company is using cash (and likely will issue debt) to repurchase the shares, the action generates positive “yield” on an ETH/sh basis, but as we’ll show, it is suboptimal for shareholders compared to using the same amount of cash, and using it to just buy ETH.

As shown in the preceding table, the $1B stock buyback generates an inferior “yield” compared to using the same proceeds and buying ETH. The intuition is straightforward – the reason is that it’s a choice of buying stock at a premium to NAV or the underlying assets at NAV. The cheaper option, therefore, results in a higher “yield.”

Share Repurchase Used to Sop up Liquidity

Why might the company choose to repurchase its stock rather than accumulate more ETH? One likely reason is to support the share price following selling pressure from the recently registered $250 million PIPE (Private Investments in Public Equity). The resale registration statement was filed and deemed effective on July 9, 2025, enabling PIPE investors to freely sell their shares on the open market. Notably, the stock declined by approximately 40% that day, likely reflecting the impact of sudden supply from PIPE-related selling. Even with the precipitous drop that day, PIPE investors made nearly 15x their money (using the July 9th close). Not bad for holding the investment for (checks calendar) 9 days.

Speed to Registration is the Key

Which brings us to our final point – lockups. In these transactions, equity investors typically participate in PIPEs at or near net asset value (1x mNAV), implicitly agreeing that “yes, your $1 of investment is worth $1 of stock.” When the deal is announced, the stock of the treasury company often “goes up a lot” – a technical measure, we know. At this point, PIPE investors are sitting on paper gains, having received $1 of stock for each $1 invested, with proceeds earmarked for acquiring the company’s favorite cryptocurrency.

Following the deal announcement, the treasury company rushes to finalize the deal and, critically, register the newly issued shares. Once the registration statement becomes effective, those shares, except for any under contractual lockup (typically affecting founders or the management team), are freely tradable. PIPE investors, in most cases, face no such lockups; their shares are simply registered and then eligible for sale.

Now, there are nuances to how quickly the deal can close and how fast the shares can be registered, but for PIPE investors, expediency is key, particularly if the stock price is above NAV. We don’t want to trivialize this part of the process. While BMNR may illustrate how quickly this can happen, many other treasury company deals announced months ago have yet to close or register their shares.

It’s also important to recognize the market dynamic at play: when a company sells 95%+ of its shares to new investors, as many of these deals do, those shares can flood the market once the lockup period ends. The result? Downward pressure on the stock price. This is what BMNR is likely trying to mitigate with its share repurchase agreement.

The Case of TRON, Tron, and TRX

There’s one final observation we have from our non-exhaustive, but exhausting, analysis of crypto treasury deals involving SRM Media, the manufacturer of stuffed animals, water bottles, and children’s toys, and owner of a media library that solely contains the 2019 movie “The Kid” starring Ethan Hawke. The company underwent massive change recently, pivoting to become a TRON (TRX – the cryptocurrency) treasury company, changing its name to Tron Inc. and ticker to TRON, naming TRON (the blockchain) founder Justin Sun as a special advisor, and engaging in a $100M Convertible Preferred PIPE, funded entirely with TRON (TRX) tokens, and whose investor base consists solely of Justin Sun’s dad. A registration statement appears to have been filed, but not deemed effective yet. Still the deal has generated a cool ~17x (paper) return, which, with warrants could amount to (again paper) profits of $3.3B (there are some restrictions here).

Final Thoughts

Crypto treasury companies continue to proliferate, and we likely haven’t seen the end of them. To the extent this capital markets trick continues to work, investors will continue to utilize it. While there are reasons why these companies should trade at premiums to NAV, chiefly their ability to issue debt instruments, there’s no guarantee they will continue to do so in the future. We’ve already seen premiums to NAV compress over time, even when shares have yet to be registered for sale. For companies only issuing equity for crypto purchases, the phenomenon is even more puzzling. ETFs are essentially the same instruments, issuing stock for the underlying, and do not trade at premiums to NAV. We think that’s something investors should think about.

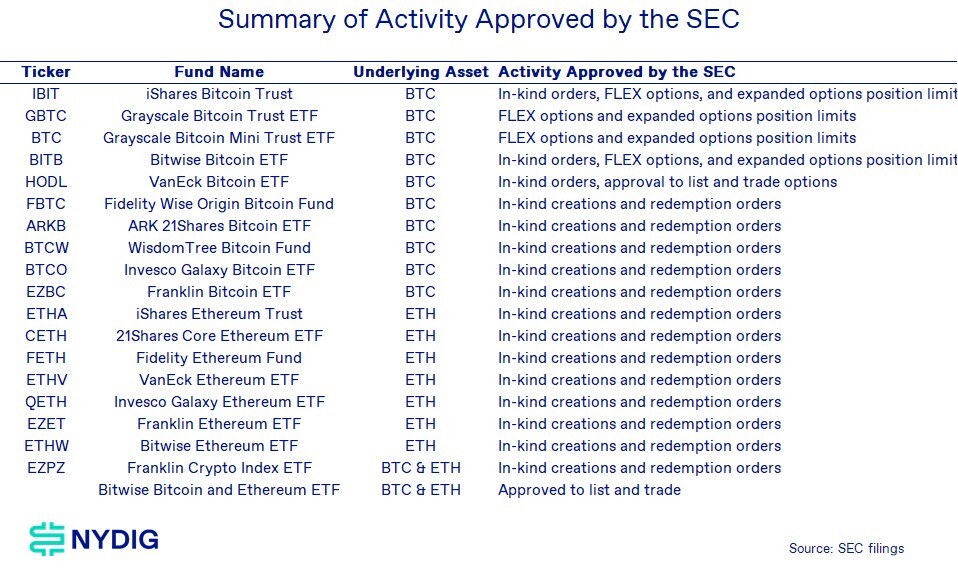

Flurry of SEC Approvals Has Important Market Implications

On Tuesday afternoon, the SEC issued a sweeping set of regulatory approvals impacting a broad range of crypto-related financial instruments. Among the decisions, the agency authorized in-kind creation and redemption orders, FLEX options trading, and a tenfold increase in options position limits for two ETFs. Notably, the SEC also approved options trading on HODL for the first time and greenlit the listing and trading of Bitwise’s Bitcoin and Ethereum ETF.

These long-anticipated moves, some sought by fund sponsors since before the initial bitcoin ETF approvals, will likely have important impacts on market structure and investor access. The effects will vary by individual products, and in this section, we break down the key implications of each change.

In-Kind Creation and Redemption Orders

In-kind orders, the ability for Authorized Participants (APs) to create or redeem ETF shares by delivering or receiving the underlying digital assets (BTC or ETH), were a key feature sought by ETF sponsors before the initial bitcoin ETF approvals in 2024. However, this became a major point of contention with the SEC, and the agency only allowed the ETFs to launch after sponsors agreed to exclude in-kind mechanisms and rely solely on cash orders.

For ETF sponsors, this restriction added operational complexity and ultimately increased costs for investors. ETF shares likely had a higher tracking error to NAV as a result. Based on our understanding, the SEC’s stance stemmed from post-FTX concerns. It was unwilling to allow regulated entities like broker-dealers (all APs are registered B-Ds) to directly handle crypto assets due to fears of systemic risk. Also, at the time, there were no clear regulatory guidelines in place for broker-dealers to custody or transact in crypto. There is still a need for further regulatory clarity for APs to fully engage in in-kind orders, but we should see spreads narrow with NAV over time, as well as lower tracking error and cost to place create and redeem orders.

Grayscale is Notably Absent from In-Kind Order Approvals

One key omission in the approval of in-kind creation and redemption orders is Grayscale products (GBTC, BTC, ETHE, ETH), simply because the changes were never requested. This is a noted change from December 2023, when Grayscale executives met with the SEC, pushing for in-kind orders (meeting memorandum).

One possible explanation is economic: the advantages of enabling in-kind orders may be outweighed by the risk of capital flight, particularly from products like GBTC and ETHE, where large holdings of low-cost-basis BTC and ETH continue to generate high fees. Still, even if large investors were able to work directly with APs to redeem the underlying crypto from these ETFs, there’s significant uncertainty around whether such transactions would be exempt from capital gains taxation. As a result, much of this capital may remain effectively locked within these funds, regardless of whether in-kind redemptions are available.

In-Kind Orders May Force APs to Acquire or Partner on Crypto Capabilities

In a world where in-kind orders are permitted by APs, those APs without the ability to affect those order when rules are clearer, will likely be at a disadvantage. There are only two APs today, Jane Street and Virtu, that also have corresponding crypto entities that can trade both sides of the trade. In the future, APs that don’t have crypto capabilities will likely not be able to take advantage of arbitrage activities and offer competitive pricing. We expect broker-dealers (APs) that don’t have crypto capabilities to acquire or partner to keep up.

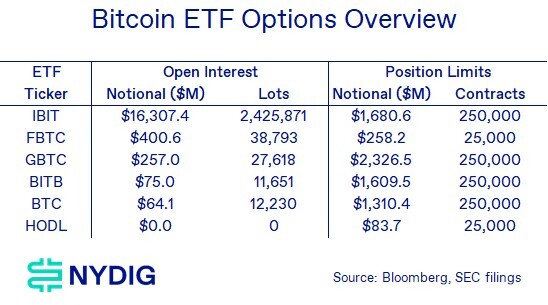

Options Limit Increases Likely to Increase IBIT’s Lead, Suppress BTC Vol Further

The other big change ushered in by the SEC was a change to individual position limits regarding the total number of contracts. When the SEC approved options on (some) bitcoin ETFs in November 2024, it set an initial position limit of 25,000 contracts. It has now upped that by a factor of 10x for all ETFs with options, except for FBTC. The change is likely to widen the monstrous lead that IBIT already has over the other players, while it hobbles FBTC’s position as the second-largest options player.

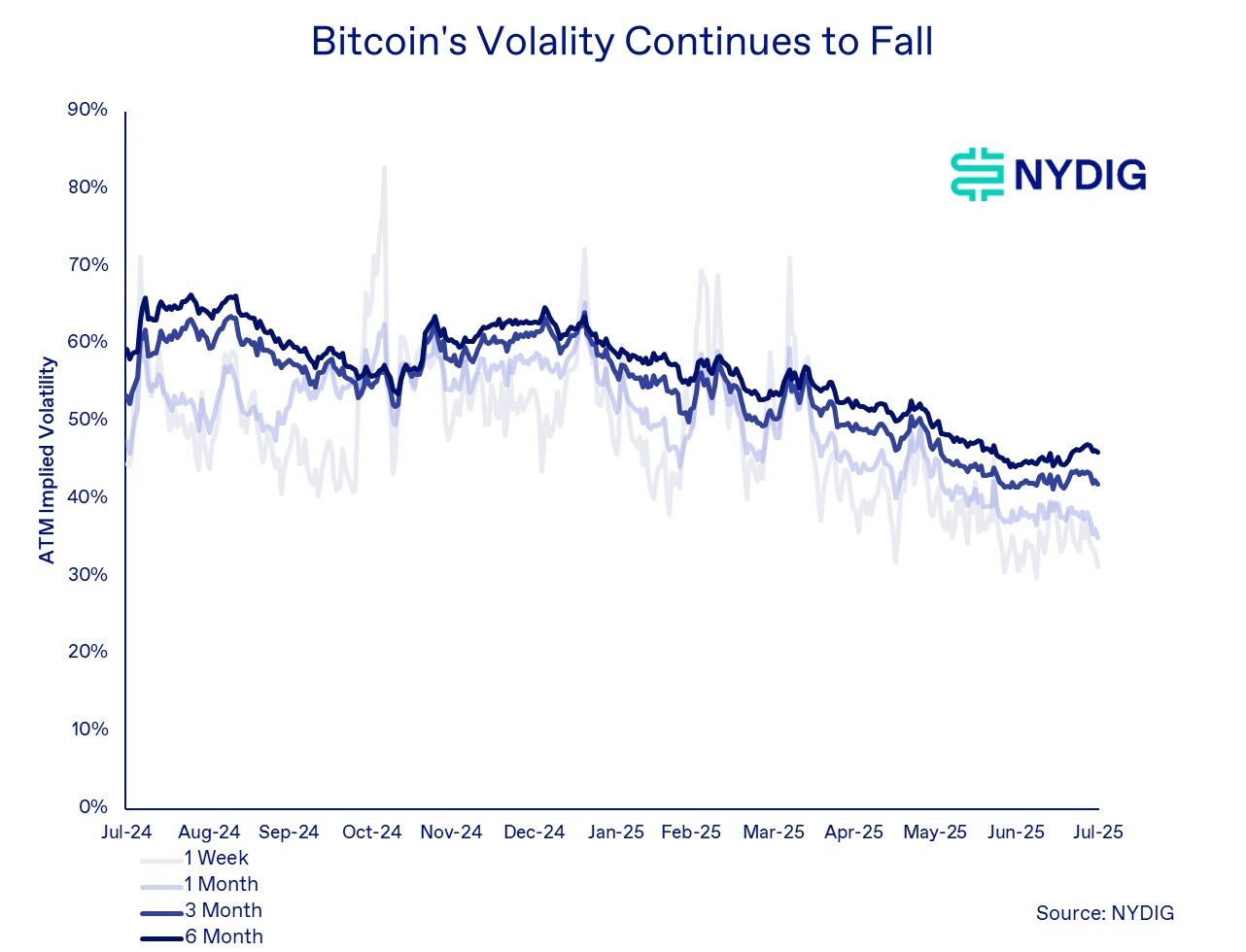

Options Supply Could Dampen Volatility

The recent increase in options position limits is likely to further suppress bitcoin’s volatility. This change enables more aggressive implementation of options strategies, like covered call selling, used to enhance returns on core positions. While bitcoin’s volatility has been in secular decline, it remains relatively attractive for volatility harvesters, especially given the broad compression of volatility across traditional asset classes.

…But Encourage Spot Buying

Although lower volatility may reduce potential yields for option sellers, it also makes bitcoin more appealing on a risk-parity basis, potentially drawing in new capital. As volatility declines, the asset becomes more investable for institutional portfolios seeking balanced risk exposure. This dynamic could reinforce spot demand. With risk-parity pioneer Ray Dalio recently advocating for a 15% portfolio allocation to gold and crypto in the face of ballooning government debt, the feedback loop of falling volatility leading to increased spot buying could become a powerful driver of sustained demand.

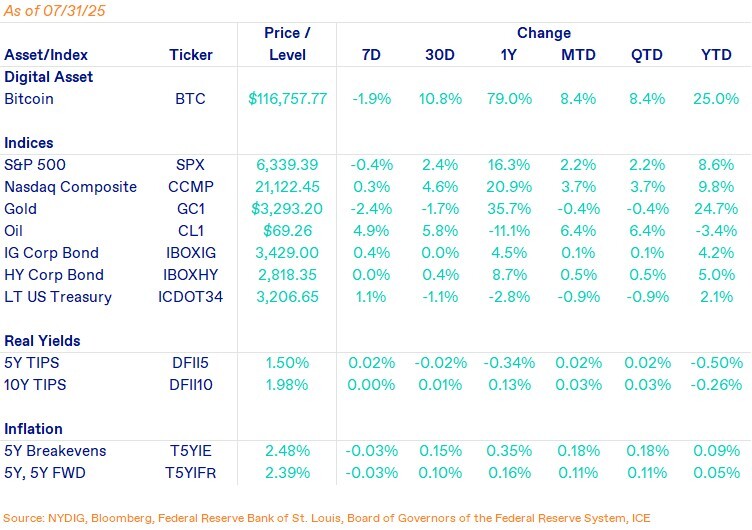

Market Update

Bitcoin fell 1.9% in the week in mostly sideways trading. While crypto got a boost from the White House’s supportive report on digital assets, and SEC Chair Atkin’s recent speech outlining numerous changes which should benefit the industry, they didn’t prove to be catalysts to keep the market rally going. While we highlighted the lack of froth in bitcoin market statistics a few weeks ago, it’s clear now in hindsight that the froth wasn’t in bitcoin markets, but in altcoins, which in some cases now have entirely roundtripped their recent rally. Markets will now have to contend with the summer seasonal lull as August rolls around, while expectations for rate cuts continue to be pushed out and jobs numbers come in weak.

Important News This Week

Investing:

Ray Dalio Recommends 15% Bitcoin and Gold Investment as U.S. Faces ‘Debt Doom Loop’ - CoinDesk

Regulation and Politics:

American Leadership in the Digital Finance Revolution - SEC

Fact Sheet: The President’s Working Group on Digital Asset Markets - White House

Report: Strengthening American Leadership in Digital Financial Technology - White House

Samourai Wallet Devs Plead Guilty to Conspiring to Run Unlicensed Money Transmitter - CoinDesk

Companies:

Chinese Crypto Giant Bitmain Plans US Factory in Trump-Era Push - Bloomberg

Upcoming Events

Aug 12 - CPI report

Aug 29 - CME expiry

Sept 17 - FOMC interest rate decision