IN TODAY'S ISSUE:

- With analysts jockeying around year end to update price targets, we introduce a framework for evaluating their implications for fund flows.

- Comparing these inflow requirements to historical ETF demand highlights that many high-end targets would take years to achieve at current pacing.

- With tokenization becoming a major trend, we look at its impact on broader cryptocurrencies.

What it Takes to Reach $1M per Bitcoin

There has been a flurry of year-end price predictions from market commentators pegging bitcoin at $100K, $120K, $200K, even $1M. Naturally, we have received many questions about how credible these targets are. Without evaluating any specific forecast, we want to provide a framework for thinking about these numbers.

First, a simple observation: none of the widely circulated targets sit below bitcoin’s current price (draw your own conclusions). Second, the shorter the time horizon of a price target, the higher the margin for error. Even if one could approximate the distribution of potential bitcoin outcomes, shorter windows naturally produce wider variability. Lengthen the investment horizon, and that outcome envelope narrows.

Framework for Evaluating Price Targets

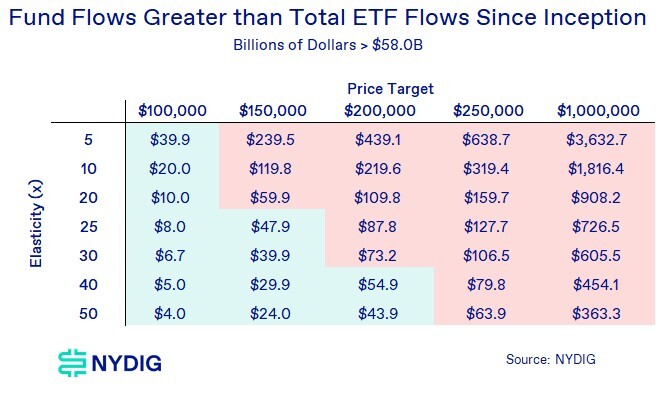

Now for some math. Analysts and prognosticators love to hand out price targets almost as much as investors love reading them, but beneath any target sits an economic reality, specifically, the capital flows required to get there. It’s not clear that analysts always appreciate what their targets imply. We walk through the framework of what it would take for bitcoin to reach $100K, $200K, or even $1M.

The mathematical approach is straightforward: calculate the market cap increase implied by the target (change in price × number of bitcoins outstanding), then divide by a “money multiplier,” the elasticity describing how much price impact $1 of net inflow has. In our 2023 pre-ETF research, we used 10x as an estimate, but that was admittedly a guess. For context, the stock market’s multiplier is roughly 5x, gold’s is 2 - 3x, Coventure once estimated bitcoin’s at 11.37x, and more recent work suggests a much wider 15 - 50x range. No one knows the true figure (it is certainly not below 5x though). Because this multiplier drives the required inflows, we present a range of scenarios so readers can see what different elasticity assumptions imply. For instance, assuming a 25x elasticity (we highlighted a band from 20x – 30x), a reasonable midpoint, it would take approximately $87.8B in net inflows for bitcoin to move from $90K to $200K.

Are The Implied Funds Flows Realistic?

With this framework in mind, the next question is whether these targets, and the implied inflows, are realistic. As a reference point, the U.S. spot bitcoin ETFs, launched less than two years ago and widely regarded as the most successful product launches in financial history, have accumulated $58.0B in net inflows. This isn’t the only channel for capital entering bitcoin (global ETFs, funds, and centralized exchanges all play meaningful roles), but the $58.0B provides a useful benchmark. When we overlay that benchmark onto the inflow requirements from the earlier table, we see that many of the price-target scenarios require inflows well above this level (red highlights).

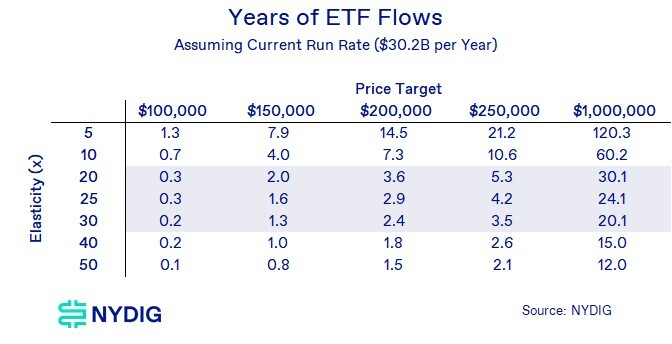

Measuring How Long It Would Take to Achieve These Targets

The final and arguably most important dimension is time. Capital may eventually arrive in the quantities required for certain price targets, but the timeline matters just as much as the magnitude. Using ETF flows again as a guidepost: the $58.0B came in over 1.9 years, or about $30.2B per year. Dividing the required inflows by this annual pace gives a rough estimate of the time needed to reach each target, recognizing these are total inflows to bitcoin, not just U.S. spot ETFs. Using the 25x elasticity assumption, reaching $200K would require roughly 2.9 years of inflows. Achieving $1,000,000, while not inconceivable in the long run, would require inflows equivalent to 24.1 years at the historical ETF pace, placing that milestone far into the future.

Cycle Inflows Have Been Dominated by ETFs

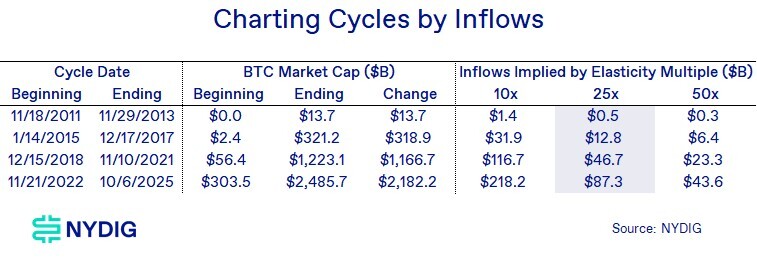

The last step we can take with this framework, now that we’ve stretched it about as far as it can go, is to estimate capital inflows across bitcoin market cycles. For this exercise, we’re treating the October 6th peak as the current cycle’s high, while acknowledging that this may or may not ultimately prove to be the true top.

Using the 25x elasticity multiple, we can approximate how much net capital entered bitcoin during each cycle. Under this assumption, the current cycle reflects roughly $87.3 billion in cumulative inflows.

Wrapping Up – Price Targets Aren’t Just About Levels but Capital Mobility

This framework makes one point unmistakably clear: ambitious price targets are not merely statements about where bitcoin could trade, but about the scale and pace of capital that must be mobilized to get it there. While bitcoin has consistently surprised investors with its ability to attract new inflows, the mathematics of elasticity and market depth impose real constraints on how quickly even large structural trends can play out. None of this diminishes the long-term potential of the asset; rather, it grounds expectations in the underlying economics. Whether bitcoin reaches $200K, $1M, or something in between will ultimately depend on whether future cycles can sustain inflow dynamics equal to or greater than those observed today. This framework does not predict which scenario will unfold, but it does clarify the conditions required, allowing investors to anchor their expectations not in headlines, but in the capital realities that drive price.

Tokenization: How One of the Industry’s Biggest Trends Impacts Crypto

In an interview last week (see link below), SEC Chair Paul Atkins touted tokenization as the key to modernization of US financial markets. While “tokenizing $68T worth of securities in the next few years” might be an aggressive goal, the point made by Atkins is an important one – tokenization is likely going to be a big trend. Because of that, we’ve got numerous questions about the tokenization of traditional assets and how it affects the rest of crypto.

Defining Tokenization

“Tokenization” most broadly means representing ownership or rights to an asset, whether it be physical, financial, or even digital, as a token on a blockchain, making it easier to transfer, divide, verify, or automate. The most popular example of this we have today is stablecoins. Issuers, such as Circle or Tether, hold dollars on behalf of clients and issue them tokens on a blockchain. One can do the same with shares of a stock, ownership interest in a fund, or even a physical asset such as gold.

Form and Function Differ Greatly

It’s important to understand that even though “tokenized” traditional financial products are an exciting market development with nearly $400B of “represented value” (not including aforementioned stablecoins) according to data aggregator RWA.xyz, their form and function differ greatly, eliciting important philosophical questions about the purpose of blockchain technology.

On one end of the spectrum, we have open, decentralized, and permissionless blockchains. Think Bitcoin and Ethereum. Anyone can become a validator/miner, inspect the blockchain, download the software, and run a node. On the other end, we have closed or permissioned blockchains. Technically, transactions are grouped and chained together with cryptographic signatures, but entry to the network or even access to the data or software is gated by say a bank or financial/technical consortium. Not all blockchains are equal, which is why saying “it’s on a blockchain” or “it’s tokenized” evokes important questions of “where?” or “how?”

Tokenization Doesn’t Imply Open Access

The largest network for RWAs today is the Canton Network, created by Digital Asset, with $380B of repurchase agreements on the network, or 91% of the total “represented value” of all RWAs. It operates as a privacy-preserving network, but is permissioned, meaning it is not a public network. Not everyone can run a node, become a validator, or deploy dapps on the network. To meme quote Boromir from LoTR, “one does not simply become a Canton validator.”

For open or permissionless networks, Ethereum is by far and away the most popular chain with $12.1B of RWAs deployed on it. BNB Chain is the second largest with $1.8B worth of RWAs. Tokenized U.S. Treasury funds are by far the most popular application there, with $8.6B of the $12.1B of RWAs.

But even on an open, permissionless network such as Ethereum, the design of the specific tokenized asset can vary greatly. And because these RWAs are often securities, broker-dealers, KYC/investor accreditation, whitelisted wallets, transfer agents, and other structures from traditional finance are required. Boromir again here: “one does not simply buy an RWA on Coinbase (a centralized exchange) or Uniswap (a decentralized exchange).”

Why Tokenize on Closed Systems?

So, if RWAs still require permissioned networks or traditional financial structures around it, why build them? What’s the benefit? Right now, near instant settlement, 24/7 operations, programmatic ownership, transparency, auditability, and collateral efficiency. These are big benefits, even at the onset. In the future, if things become more open and regulations become more favorable, as Chairman Atkins suggests, access to these assets should become more democratized, and thus these RWAs would enjoy expanded reach, in addition to all the previously mentioned back and middle office benefits.

The Benefits To Crypto

The benefits to networks these assets reside on, such as Ethereum, are light at first, but increase as their access and interoperability and composability increase. Initially, the benefits for Ethereum are transaction fees generated by the usage of the RWAs (part of which are used to burn ETH supply). Ethereum, or the home blockchain, would also enjoy increasing network effects of being the place where RWAs and other assets are built. In the future, one could see these RWAs being part of DeFi (composability), either as collateral for borrowing, an asset to be lent out, or for trading.

This will take time as technology develops, infrastructure is built out, and rules and regulations evolve. “One does not simply become composable and interoperable RWA” to meme quote Boromir one last time. But the future is exciting, and investors should pay attention, even if the economic impacts to traditional cryptocurrencies are minimal today.

Market Update

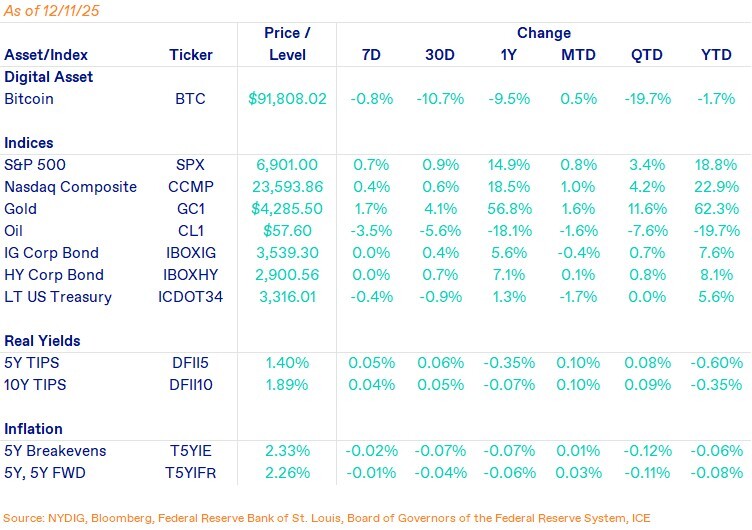

Bitcoin was essentially unchanged over the past seven days, continuing the consolidation phase that has characterized its trading since mid-November. The most notable catalyst this week was the FOMC’s December interest rate decision, which delivered a more dovish-leaning interpretation than markets expected. Bitcoin initially bounced on the announcement but failed to sustain momentum, retracing back into its prior trading range.

Flows into the bitcoin ETFs have turned positive again since mid-November, reversing the substantial outflows seen in the wake of the big liquidation event on October 10th. At the same time, stablecoin outflows have also reversed, with aggregate stablecoin supply now climbing back toward its all-time high.

Prices of cryptocurrencies across the board have stabilized, even rebounded in some cases (altcoins are often a leading indicator). But as we start looking forward to 2026, the question of cycles versus secular growth is still on everyone’s mind. There’s a lot to like in 2026: dovish monetary conditions, new use cases such as tokenized stocks and other RWAs, growing institutional participation, and a maturing ETF ecosystem that continues to broaden access. Yet the bigger issue is whether these developments merely set the stage for another cyclical upswing, or whether they mark the beginning of a more durable structural trend in crypto adoption. The answer will depend on whether capital inflows and real-world utility break the industry out of its historical boom-and-bust pattern.

Important News This Week

Regulation and Taxation:

SEC's Paul Atkins Touts 'Tokenization' as Key to Modernizing US Markets - Fox Business

U.S. SEC Gives Implicit Nod for Tokenized Stocks - CoinDesk

U.S. Senate's Crypto Market Structure Bill Gets Messy as Calendar Weighs Down - CoinDesk

Mexico’s Central Bank Keeps a ‘Healthy Distance’ From Crypto - CoinDesk

Investing:

JPMorgan Analysts Doubt Crypto Winter Is Coming, Despite 'Meaningful' Bitcoin Sell-Off - Decrypt

Ark Invest’s Cathie Wood: Bitcoin’s Four-Year Cycle Will Be ‘Disrupted’ - Decrypt

Companies:

Strategy's Letter to MSCI Regarding Index Inclusion - MSTR

Interactive Brokers Allowing Accounts to be Funded by Stablecoin - Bloomberg

Coinbase Ready to Launch Prediction Markets, Tokenized Stocks - Bloomberg

Tether Blocks Investor Sales While Pitching $20 Billion Funding - Bloomberg

UK Bitcoin Company Satsuma Sells 579 of Its 1,199 Bitcoin for $53.2 Million - CoinDesk

SpaceX Moves Another $95 Million of its Bitcoin Stash Amid Reported 2026 IPO Plans: Arkham - The Block

Upcoming Events

Dec 26 - CME expiry