IN TODAY'S ISSUE:

- The CLARITY Act cleared committee 15-9 on Thursday, with bipartisan support and comments that give hope there will be sufficient support when the bill reaches the floor.

- The functional floor window is June through early August, after which the pre-election campaign season effectively closes it.

- Ethics was the major unresolved issue coming out of markup. The details of a floor amendment are likely already in the works, but whether the final language satisfies Democratic senators needed for cloture is the central question.

- While the stablecoin yield compromise is closed at the policy level, with passive yield prohibited and activity-based rewards permitted, banking trade groups are pushing for tighter language and could pressure Republican senators.

- Investors should watch for an ethics agreement in the next couple of weeks, completion of Banking/Agriculture bill reconciliation, whether law enforcement groups sign off on revised language narrowing certain exemptions, and whether bank trade groups are able exert their influence on the stablecoin yield topic.

What Is This Bill and Why Does It Matter

The Digital Asset Market Clarity Act (CLARITY Act) is the most comprehensive attempt by the U.S. Congress to establish a permanent legal framework for digital assets. For the past decade, crypto companies and investors have operated in a regulatory gray zone, with the SEC and CFTC frequently in conflict over which agency has jurisdiction and with enforcement actions substituting for clear rules. This bill resolves that ambiguity by drawing a definitive boundary: digital assets that function like securities (giving holders a claim on a company's profits or governance) fall under SEC oversight, while digital assets that function like commodities, bitcoin being the primary example, fall under CFTC oversight.

For institutional investors, the practical significance is substantial. Clear jurisdiction means crypto firms can structure products, custody arrangements, and trading operations with legal certainty for the first time. It enables traditional financial institutions such as banks, broker-dealers, and asset managers to participate in digital asset markets without regulatory exposure. It creates a federal licensing framework for exchanges and custodians that currently operate under inconsistent state-by-state rules. And it establishes the first federal framework for decentralized finance (DeFi), one of blockchain’s biggest applications, which has remained essentially unregulated at the federal level.

The bill also statutorily classifies bitcoin as a commodity under CFTC jurisdiction, removing any risk (as remote as it may be) that a future administration reasserts SEC securities classification over bitcoin.

The Path from Committee to Law

Congress has two chambers: the House of Representatives (435 members) and the Senate (100 members). A bill must pass both chambers in identical form and then be signed by the president to become law. The House passed its own version of the CLARITY Act on July 17, 2025, by a 294-134 bipartisan vote. The Senate Banking Committee vote on May 14th is the first of several remaining Senate steps. Once the Senate passes its version, the two chambers must reconcile any differences. In this case it is likely that the House will pass whatever version of the bill that the Senate ultimately passes thereby sending that version to the President for his signature.

After a Senate committee approves a bill, the Senate Majority Leader schedules it for a vote by the full Senate of 100 members. Before any senator can cast a final yes or no vote on the bill itself, the Senate must first agree, by a 60-vote supermajority, to end debate and proceed to a final vote. This threshold, called cloture, is the primary tool the minority party uses to block legislation it opposes. Without 60 votes to end debate, a determined minority can block a bill indefinitely regardless of how many senators would vote yes on final passage. Republicans currently hold 53 Senate seats. Even with all 53 voting yes on cloture, they are 7 votes short. They need at least 7 Democratic senators to allow the bill to come to a final vote, not necessarily to vote for it, but simply to not block it. Once the 60-vote threshold is cleared, final passage requires only a simple majority of 51, which Republicans can reach on their own.

How the Committee Vote Went Down

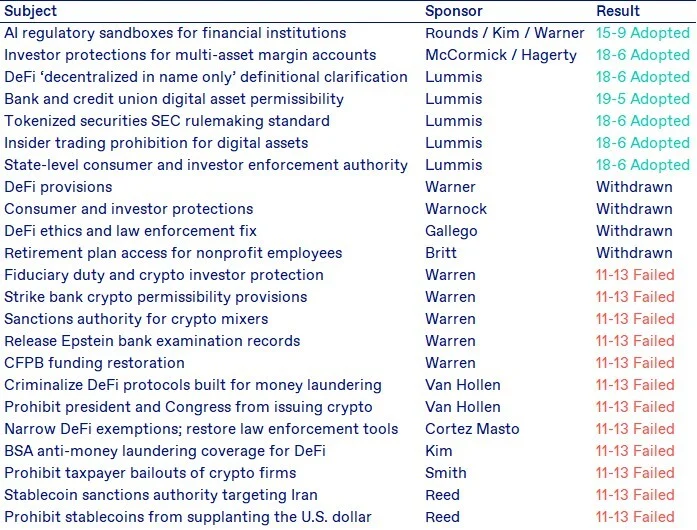

The Senate Banking Committee has 24 members: 13 Republicans and 11 Democrats. The bill passed 15-9, with all 13 Republicans joined by Senators Ruben Gallego (AZ) and Angela Alsobrooks (MD). The remaining nine Democrats voted no: Senators Catherine Cortez Masto (NV), Raphael Warnock (GA), Andy Kim (NJ), Lisa Blunt Rochester (DE), Chris Van Hollen (MD), Tina Smith (MN), Elizabeth Warren (MA), Jack Reed (RI), and Mark Warner (VA). While Senator Warner ultimately voted no on final committee passage, he continued to support ongoing negotiations.

The committee spent approximately four hours voting on 23 amendments. Republicans passed seven amendments, several with Democratic support, covering investor protections for multi-asset trading accounts, clarifications to the DeFi regulatory framework, and explicit permissibility for banks and credit unions to hold and trade digital assets. Eleven Democratic amendments failed on party-line votes of 11-13. Four amendments were withdrawn by Senators Warner, Gallego, and Warnock in exchange for explicit commitments from committee leadership to continue negotiating outstanding issues before a floor vote.

The two Democratic yes votes are not without conditions. Senator Gallego voted yes on the merits, specifically citing ethics guardrails, Agriculture Committee coordination, and remaining law enforcement concerns as the three conditions he needs resolved before committing to a floor yes. Senator Alsobrooks voted yes explicitly as a procedural vote to keep negotiations moving, stating on the record: "My vote today is a vote to keep working in good faith. It does not mean that I'll be voting for the passage of the Clarity Act on the floor." For investors assessing floor vote probability, the practical implication is that Democratic committee support is conditional.

The Legislative Timeline

White House crypto adviser Patrick Witt targeted July 4th at Consensus Miami on May 6, laying out specific mechanics: Senate Banking Committee markup in May (completed), four working Senate weeks in June for floor passage, and a House reconciliation vote before Independence Day, but this may represent an aspirational benchmark rather than a fixed legislative deadline.

The realistic window, however, is June through early August. The 119th Congress expires January 3, 2027, but Congress recesses in late July and returns in September to a pre-election period in which leadership is unlikely to schedule a contested 60-vote floor fight. If the bill misses that window, the highest-probability remaining pathway becomes a post-election lame-duck session, available only if Republicans hold the Senate and Majority Leader Thune prioritizes it over government funding deadlines. Senate control after the midterms remains competitive, creating uncertainty around the legislative environment for any delayed crypto market structure bill. If Democrats flip the chamber, a Republican-authored crypto market structure bill does not advance in the 120th Congress. Congressional negotiators face a tradeoff between accepting an imperfect bipartisan framework in 2026 versus risking a substantially different legislative environment after the midterms.

The Remaining Hurdles

Ethics: Narrowing

The bill already contains an ethics provision. The current Senate Banking text explicitly states that existing Office of Government Ethics laws and congressional ethics rules prohibit any member of Congress or senior executive branch official from issuing a digital commodity during their time in public service. Democrats’ objection is not that the bill lacks ethics language but that the existing language is too narrow, relies on existing statutes rather than creating new enforceable prohibitions, and does not cover holding or profiting from digital assets, only issuance. Republicans blocked every amendment seeking to expand the ethics provision, arguing the existing language is sufficient and that broader prohibitions belong in a different committee.

The White House's negotiating posture, confirmed by Witt at Consensus, is to accept a universal prohibition covering everyone from the president to a Capitol Hill intern, but to reject any language that singles out a particular officeholder, family, or office. "We're not going to allow targeting of anyone's family, any one particular politician," Witt said, adding: "I'm optimistic that we're going to be able to close that out." The most plausible landing zone is a forward-looking prohibition barring future profit-taking from new positions without requiring divestiture of existing holdings. The fact that Gallego and Alsobrooks voted yes in committee, both senior senators who understood the floor conditions when they cast those votes, suggests the contours of an acceptable floor amendment are likely already understood privately. The remaining question is whether the language that emerges is sufficient for the additional Democratic senators needed for cloture who were not part of the committee negotiation.

DeFi Law Enforcement: Solvable

The bill's framework for decentralized finance creates a regulatory carve-out for protocols that are genuinely decentralized, meaning no single person or company controls the software or the funds. The intent is to avoid regulating open-source code like a bank. During markup, Senator Cortez Masto referenced opposition letters from multiple law enforcement organizations expressing concern that DeFi carve-outs could weaken anti-money-laundering enforcement. Tornado Cash, a mixing service that laundered over $7 billion, including more than $450 million for North Korean state-sponsored hackers, is the reference case. Recent federal court rulings have constrained Treasury's ability to sanction certain smart-contract systems absent clearer statutory authority, and the bill as written does not clearly provide that authority.

This issue is closer to resolution than the committee vote suggested. Senator Lummis and Senator Warner reached a partial agreement during markup, reflected in the adopted Amendment 122. Witt confirmed at Consensus that several issues previously viewed as intractable, including DeFi governance and illicit finance protections, have been quietly resolved in recent weeks.

Agriculture Committee Reconciliation: Procedural

The Senate Agriculture Committee completed its parallel markup on January 29, 2026, advancing the Digital Commodity Intermediaries Act 12-11 on a party-line vote. That bill covers the CFTC side of the regulatory framework: digital commodity definitions, exchange registration, and intermediary compliance. It is a companion to the Banking Committee's CLARITY Act, not a duplicate. What remains is reconciling the two Senate bills into a single floor vehicle before a full Senate vote can occur. This is staff-level drafting work, which makes it faster and less politically exposed than a fresh markup. It is not ideologically contentious, but it is a hard sequencing requirement. For the floor debate to begin by the week of June 15, reconciliation needs to be substantially complete by June 1.

The Stablecoin Yield Provision

The yield debate is resolved at the policy level. Senators Tillis and Alsobrooks reached a compromise in early May, confirmed closed by White House adviser Witt at Consensus: passive yield on stablecoin balances is prohibited; activity-based rewards tied to actual transactions are permitted. "Crypto is unhappy, banks are unhappy, but they're both about equally unhappy. And so we know that we got the right compromise," Witt said.

The open question is whether that compromise holds on the Senate floor. Six banking trade associations are pushing for tighter language with no activity-based carve-outs, arguing that any reward structure tied to balance size or holding duration is economically equivalent to deposit interest and will drive deposit flight. The crypto industry wants room to offer yield in at least some circumstances. These are not drafting disagreements. They reflect a fundamental policy conflict over whether stablecoin issuers should be able to compete with bank deposits at all. The banking groups made limited headway in committee, but their floor leverage runs in both directions. Community banking associations have strong relationships with Republican senators from rural states where regional bank credit dominates. With Republicans needing to hold all 53 seats, a defection of even one or two members over the yield provision could complicate the floor math as much as any Democratic holdout.

Amendment Scorecard

Most Democratic amendments failed on near party-line 11-13 votes, while several bipartisan or Republican-backed amendments passed with support from a subset of Democratic members.

What Passage Would Mean for Crypto Markets

If the CLARITY Act is signed into law, the market impact operates through three channels. The most direct is institutional capital deployment. Major asset managers, pension funds, and bank trust departments have been restricted from meaningful crypto exposure by the absence of a clear federal regulatory framework, either because compliance departments cannot approve products without defined rules or because regulators have actively discouraged participation. Legal clarity on jurisdiction, custody standards, and product permissibility reduces those barriers for a pool of capital that dwarfs current crypto market capitalization. The bipartisan 19–5 committee vote adopting explicit bank digital-asset permissibility language reflect the breadth of political support for removing those barriers.

The second channel is balance sheet participation by regulated financial institutions. The bill explicitly permits banks to hold digital assets directly, lend against crypto collateral, and participate in DeFi protocols. This could increase liquidity provision, deepen market participation, and over time contribute to lower volatility and tighter spreads, and makes the market more accessible to risk-averse institutional allocators. These provisions passed with the widest bipartisan margins of any contentious element of the bill, suggesting they are durable through floor negotiations.

The third channel is statutory regulatory certainty for bitcoin specifically. CFTC commodity classification removes the residual risk of future SEC securities reclassification and establishes a lighter-touch oversight regime focused on market manipulation and fraud rather than the issuer-disclosure requirements that govern securities. Combined with the spot ETF approvals already in place, permanent CFTC jurisdiction closes the last significant regulatory overhang for bitcoin as an institutional asset class.

If the bill fails, most likely through stalled ethics negotiations, unresolved DeFi enforcement concerns, or Senate floor scheduling delays, the crypto industry operates under the current SEC and CFTC regime indefinitely. Under Chair Atkins, the SEC has reversed the Gensler-era enforcement posture and signaled a preference for rulemaking over litigation, plus the SEC and CFTC have jointly produced a token taxonomy to reduce regulatory ambiguity. That is still meaningful near-term improvement, but not the permanent jurisdictional ambiguity the legislation is designed to eliminate.