IN TODAY'S ISSUE:

- We analyze bitcoin’s relationship with software equities to assess whether common underlying factors are driving performance across both asset classes.

- We assess recent critiques of Bitcoin from prominent investors and their relevance to its long-term growth trajectory.

Bitcoin’s Correlation with Software Stocks: Signal or Noise?

Bitcoin rallied sharply this week alongside U.S. software equities (the IGV ETF), prompting claims that bitcoin has effectively become an IGV proxy. However, while the visual fit of their indexed price is compelling, the conclusion that bitcoin and software equities have structurally converged, or that they share common exposure to themes such as AI or quantum risk, is overstated. The recent price action more plausibly reflects shared exposure to the current macro regime, specifically long-duration, liquidity-sensitive risk assets, rather than evidence of a structural convergence between bitcoin and software equities.

What Bitcoin’s Correlations Tell Us

On a 90-day rolling basis, bitcoin’s correlation with IGV has increased since its early October all-time high. Bitcoin’s correlations with the S&P 500 and Nasdaq 100 have also risen over recent periods, indicating that the change is not isolated to software stocks.

Additionally, bitcoin’s correlation with semiconductor equities softened in 2026 even as its correlations with broader equities, technology, and software have moved higher. Software and semiconductors have been driven by different fundamental narratives, with AI-related capital favoring infrastructure and chip names, while software has had to contend with competitive disruption concerns.

Factors Point to Bitcoin Being Priced as a High Beta Liquidity Sensitive Growth Asset

Bitcoin’s rising equity correlations with the S&P 500, Nasdaq 100, and IGV suggest it is keying off broad growth-beta and liquidity conditions rather than on sector-specific fundamentals. More specifically, it appears that bitcoin is not currently being priced as a macro hedge, a sovereign risk hedge, or a real-rate or inflation trade. That dynamic helps explain the ongoing frustration around bitcoin’s failure to “act like gold” despite the digital gold label. The marginal buyer today appears to be macro- and equity-sensitive, allocating along the risk curve, rather than capital expressing a distinct monetary thesis.

Bitcoin Price Movements are Still Largely Idiosyncratic

Even with correlations to IGV, the Nasdaq, and the S&P 500 in the 0.5 range, the majority of bitcoin’s price movement remains unexplained by equities. A 0.5 correlation implies an R-squared of roughly 0.25, meaning only about one-quarter of bitcoin’s moves are explained by that single equity factor. The remaining 75% reflect drivers outside traditional stock indices.

These idiosyncratic forces reflect bitcoin’s distinct market structure and drivers: asset-wide fund flows, network activity and adoption trends, trader and derivatives positioning, and regulatory and policy developments, to name a few. That differentiation supports bitcoin’s role as a portfolio diversifier. While cross-asset correlations with equities are currently elevated, they remain far from determinative of bitcoin’s returns.

Knives Out: Did Chamath and Dalio Turn on Bitcoin, or Did Their Views Evolve?

Recent comments from Chamath Palihapitiya (here) and Ray Dalio (link) have sparked debate over whether these bitcoin advocates have turned on the asset. Chamath was an early and vocal supporter (2013), while Dalio’s views are more recent (2021), but what we’d consider "skeptically constructive." While some interpret their latest remarks as a repudiation, we think the underlying questions have changed. The discussion has moved from “Can Bitcoin survive?” to “Is bitcoin ready to function as a sovereign reserve asset?”

Chamath: From Disruption to Institutional Constraints

In 2013, Chamath pitched bitcoin as a response to post-2008 distrust in financial institutions. In his Bloomberg op-ed, he described it as “Gold 2.0,” potentially even a reserve currency, and recommended a 1% allocation as “schmuck insurance” against systemic failure. The thesis was clear: decentralized, censorship-resistant money could rebalance power away from centralized intermediaries.

Now, he questions bitcoin’s suitability as a central bank reserve asset, citing privacy and fungibility concerns. That is not a reversal of the original thesis but rather a narrowing of it. In 2013, the target buyer was the individual investor hedging systemic risk. In 2026, the debate centers on sovereign balance sheets, where the same transparency once framed as a strength can look like a negative at the central bank level.

Dalio: Consistent Skepticism on Reserve Status

In Bridgewater’s 2021 note, Dalio called Bitcoin “one hell of an invention” but described it as “a long-duration option on a highly unknown future." The firm flagged volatility, regulatory risk, liquidity limits, and an unproven diversification record as barriers to reserve-grade status. Bridgewater’s 2022 research acknowledged improving liquidity and rising institutional participation but still framed adoption as early and operationally constrained.

Dalio’s recent critique centers less on price action and more on structural constraints. Like Chamath, he has questioned whether bitcoin offers the level of privacy sovereign institutions require and whether it suitable for central bank backing. In addition, he has flagged long-term technological risks, including the possibility that advances such as quantum computing could threaten cryptographic security. Taken together, these concerns are consistent with his longstanding view that bitcoin remains an emerging, high-uncertainty asset, better characterized as a convex alternative than a foundational reserve holding like gold.

What Actually Changed

The asset itself has not changed, but to us, these new concerns from Chamath and Dalio imply the standards by which it is judged have. As bitcoin evolved from a fringe alternative for individuals disillusioned with the post-GFC banking system into an institutional portfolio allocation, expectations have changed. What began as an asset outside the monetary order is now being evaluated within it. Chamath and Dalio are responding to that shift.

Bitcoin Does Not Need Central Bank Endorsement

Does bitcoin need to be adopted by central banks in order to continue growing? We don’t think so. To begin with, sovereign exposure already exists. Several nation-states hold bitcoin today, largely through asset seizures tied to criminal enforcement actions, while others have accumulated exposure more deliberately, either through direct purchases or via sovereign wealth funds. In addition, several countries have sponsored domestic bitcoin mining initiatives, effectively embedding exposure at the infrastructure level.

More importantly, bitcoin’s growth thesis does not depend on reserve adoption by central banks. Unlike prior technological revolutions, where venture capital and institutions captured early-stage gains before public markets allowed access to individuals, bitcoin was adopted first at the retail level. Individuals accumulated, secured, and monetized the network long before traditional financial institutions appeared. Institutional involvement has followed, not led, the adoption curve.

Bitcoin is structurally different from previous technological cycles. It is a monetary network that is built from the edge inward, from individual users to family offices, to asset managers, to corporates and ETFs, and now, in some cases, to sovereigns. Central bank ownership may ultimately validate the asset class further, but it is not a prerequisite for continued growth. Bitcoin’s value comes from its globally distributed network, political neutrality, and technical and economic properties that enable censorship-resistant value transfer, digital scarcity, and independent operation free from any single government, institution, or monetary authority.

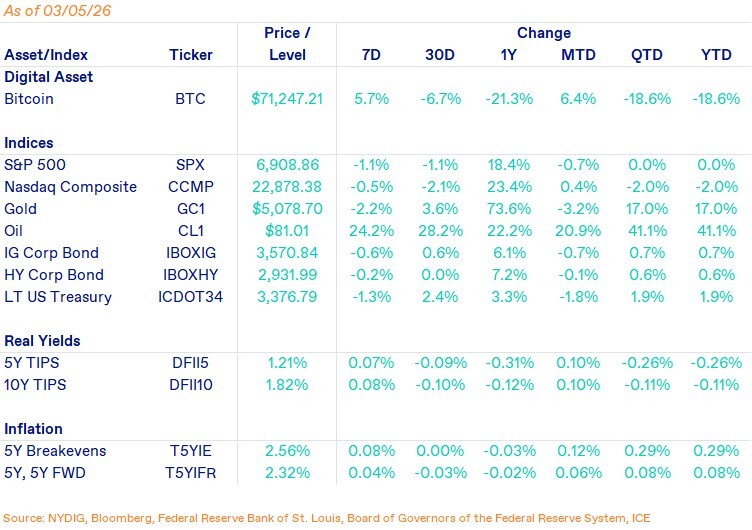

Market Update

Bitcoin rallied 5.7% on the week, briefly pushing through the $70K level before momentum faded and price slipped back below that level. The move followed a volatile start to the weekend. In the early hours of Saturday, when traditional markets were closed, bitcoin initially sold off in response to the strikes in Iran. The weakness proved short-lived. Bitcoin quickly stabilized and reversed higher, ultimately breaking decisively above $70K by midweek and reaching $74,100 at its peak. The price action suggests either that a short-term bottom had already formed or that bitcoin is increasingly being treated as a hedge during periods of geopolitical instability. That, however, has reversed course once again as bitcoin has fallen again with risk assets on the back of weak economic data on Friday.

Flows and derivatives positioning reinforced the constructive tone earlier in the week. U.S. spot ETFs recorded approximately $890 million in net inflows over the past five trading days, with the strongest creations occurring early in the week following the escalation in Iran. At the same time, CME front-month annualized basis widened from roughly 5 - 6% to 7 - 8%, signaling firmer demand and modest re-leveraging in regulated venues. Offshore basis also rose from around 1 - 2% to 2 - 3% but remains meaningfully below onshore futures.

Across macro markets, the reaction was mixed. Gold initially rallied sharply, up roughly 4.5% at its peak, consistent with its use as a safe-haven asset, but has since retraced and now sits below its pre-conflict level. Oil spiked on the news and continued to grind higher, potentially reflecting expectations of a more protracted conflict. U.S. equities showed notable resilience despite the geopolitical backdrop, while Treasuries sold off rather than rallied, likely in response to inflation concerns caused by high oil prices.

Important News This Week

Investing:

Kazakhstan Central Bank to Invest Up To $350 Million In Crypto and Digital Asset Markets - CoinDesk

Iran Strikes Expose Dark Edge Case of Prediction-Market Era - Bloomberg

Regulation and Taxation:

Trump Urges Passage of U.S. Clarity Act, Attacks Banks For 'Undercutting' GENIUS - CoinDesk

Tron's Rainberry to Pay $10 Million To Settle SEC, Justin Sun Lawsuit - CoinDesk

CFTC Chief Selig to Clear Path for U.S. Perpetual Futures in Coming Weeks - CoinDesk

Companies:

Kraken Wins Fed Master Account Approval, A First for the Crypto Industry - The Block

New York Stock Exchange Owner Values Crypto Exchange OKX at $25 Billion In New Partnership - CoinDesk

Over 15,000 BTC Sold and More Coming as Public Miners Pivot To AI - CoinDesk

Upcoming Events

Mar 11 - CPI release

Mar 18 - FOMC interest rate decision

Mar 27 - CME expiry

Apr 27 - Bitcoin 2026 conference