IN TODAY'S ISSUE:

- On May 26, one institution sold $1.26B of IBIT in a single off-exchange block. We unpack what the tape and holder data reveal about who sold and why.

- A 2.3% block discount, $29.5M in urgency premium, rules out basis arbitrage on economics alone and identifies a directional long position exiting.

- The $720 million of IBIT redemptions across May 26–27 should not be viewed as a direct measure of selling associated with the block, as net fund flows can obscure gross creation & redemption activity occurring simultaneously.

Notes on a $1.3 Billion Trade

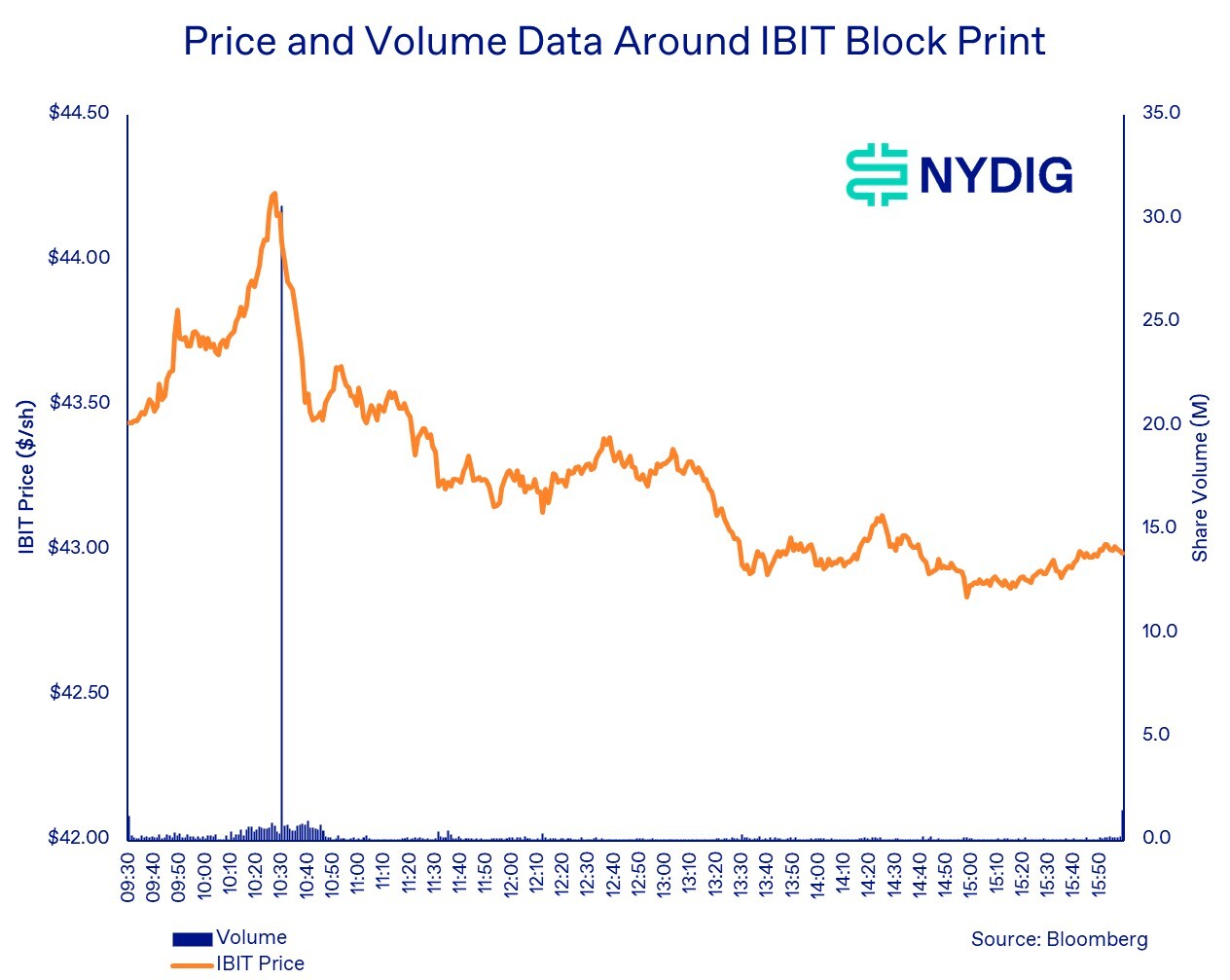

At 10:30:34 ET on May 26, 2026, a single counterparty sold 29.21 million IBIT shares in an off-exchange transaction at $43.16 per share, representing approximately $1.26 billion in notional value. The seller accepted a $1.01 discount to the prevailing market price of $44.17, a 2.3% concession worth approximately $29.5 million, in exchange for immediate execution.

The evidence is most consistent with a large directional holder exiting a concentrated position rather than a contemporaneous basis-trade unwind. The transaction exceeded the reported position of every disclosed March 31, 2026, 13F holder, required an unusually large price concession, and was not accompanied by the CME futures activity that would be expected if a basis position were being unwound.

Market Context

The block occurred against a deteriorating technical backdrop. U.S. spot Bitcoin ETFs entered May 26 following six consecutive sessions of net outflows beginning May 15. The category lost approximately $1.55 billion during the streak, with IBIT accounting for roughly $1.1 billion.

Bitcoin had rallied into its descending 200-day moving average near $82K-$82.5K in early May before failing to break through resistance. By mid-May, price had fallen back below the trendline and momentum had deteriorated materially, with the 14-day RSI declining from approximately 70 to the mid-30s. The failed breakout likely contributed to the persistent ETF outflows that preceded the block transaction.

Events Ahead of the Trade

IBIT opened May 26 at $43.44 and traded within normal volume ranges during the first hour. Activity accelerated between 10:16 and 10:28 as the stock advanced from $43.81 to an intraday high of $44.24.

The 10:26-10:27 and 10:27-10:28 intervals recorded 822,000 and 702,000 shares, respectively, approximately 3-4x normal trading activity. The timing suggests the executing broker and the seller may have used the increase in liquidity and price to facilitate placement of the upcoming block.

The Block Trade

At 10:30:34 ET, 29.21 million shares printed at $43.16 via FINRA/Nasdaq TRF Carteret, one of the reporting facilities broker-dealers use to disclose privately negotiated off-exchange transactions to the public tape.

The transaction carried three notable trade condition codes:

- Q (FINRA/Nasdaq TRF Carteret): The trade was reported through an off-exchange trade reporting facility rather than executed on a lit exchange. This indicates the transaction was privately negotiated before being reported to the public tape.

- R6 (Rule 611 Trade-Through Exemption): The transaction was executed under an exemption to Regulation NMS's trade-through protections, allowing the block to be completed at a negotiated price without routing portions of the order across multiple venues to seek displayed quotes.

- IS (Intermarket Sweep Order): The trade was designated as an Intermarket Sweep Order, a mechanism used when a participant prioritizes execution certainty and speed by taking responsibility for satisfying protected quotations across markets rather than relying on standard routing procedures.

Taken together, the designations indicate a negotiated off-exchange block transaction executed under trade-through exemptions and sweep procedures that allowed the seller to prioritize certainty of execution over price improvement.

The shares changed hands at $43.16, $1.01 below the prevailing market price of $44.17, representing a 2.3% discount and approximately $29.5 million of execution cost. The trade dominated activity in IBIT, with the 10:30-10:31 minute bar recording 30.62 million shares, roughly 40x the volume of adjacent intervals. A 20,000-share trade executed seconds earlier at $44.17 confirms that the discount was specific to the negotiated block rather than the result of a broader market move.

Following the print, IBIT recovered to approximately $44.06 within the next minute before gradually declining through the remainder of the session and closing at $42.99. The rapid recovery suggests the discount reflected the economics of transferring a $1.26 billion position in a single transaction rather than a market-wide liquidity event or sudden deterioration in underlying value.

Why a Basis Unwind Appears Unlikely

Three independent observations weigh against the basis-unwind explanation.

Economics

A delta-neutral basis strategy earns carry from the spread between spot and futures. At prevailing spreads, accepting a 2.3% discount on the ETF leg would consume a substantial portion of the strategy's expected annual return. A basis investor facing no external constraints would generally be expected to unwind passively over time rather than accept an immediate 230-basis-point execution penalty.

Execution Structure

The transaction was structured to maximize execution certainty. That behavior is more consistent with a holder seeking immediate liquidation than with a basis trader managing a delta-neutral position. While a forced deleveraging event could produce similar behavior, the transaction structure alone does not provide evidence of such a constraint.

CME Futures Activity

The strongest evidence comes from CME futures trading. A 29.21 million-share IBIT position represents approximately 18,500 BTC of exposure, equivalent to roughly 3,700 CME Bitcoin futures contracts. The total CME bitcoin futures volume on May 26 was approximately 8,630 contracts. The 10:30-10:31 interval corresponding to the block recorded only 91 contracts, while the adjacent minute recorded 93 contracts. Even the entire 10:30-11:00 window accounted for only about 1,070 contracts.

A simultaneous basis unwind of this size would have represented approximately 43% of total daily CME volume and likely produced a visible spike in futures activity. No such activity occurred.

Redemptions Do Not Identify the Seller

IBIT reported approximately $192 million of net redemptions on May 26 and $528 million on May 27, for a two-day total of approximately $720 million. These figures should not be interpreted as a direct measure of selling pressure associated with the block transaction.

ETF creation and redemption orders can be submitted either same day or on the prior evening, depending on the mechanism used, making it difficult to distinguish investor-driven flows from offsetting creation and redemption activity associated with ETF facilitation. In addition, IBIT's reported NAVs of $42.955 on May 26 and $42.431 on May 27 were both below the block execution price of $43.16. Redemption at NAV would therefore have been economically unattractive for a buyer seeking to monetize the position immediately.

The more likely exit path was secondary-market distribution rather than immediate redemption. Consequently, the reported redemptions may reflect other investors reducing exposure during the same period rather than activity directly attributable to the block itself.

Who Was the Seller and Why?

At 29.21 million shares, the position exceeded the reported March 31, 2026, holdings of every disclosed 13F holder of IBIT. Excluding authorized participants whose reported positions may reflect inventory rather than directional exposure, the universe of potential sellers is very narrow.

While the execution structure itself establishes urgency, it does not establish motive. One possibility is a forced sale driven by investor redemptions, risk limits, or balance-sheet constraints. Under that scenario, the transaction carries little informational value regarding bitcoin conviction. The alternative is a discretionary investment decision. In that case, the seller chose to absorb a $29.5 million execution cost rather than accept the risk of exiting over multiple sessions.

Public data cannot distinguish conclusively between these explanations. However, the weakening technical backdrop, ongoing ETF outflows, and willingness to pay a substantial execution premium for immediacy are more consistent with discretionary liquidation rather than investor redemptions or a portfolio rebalance.

Final Thoughts

The available evidence points toward a large directional holder exiting a concentrated IBIT position through a negotiated block transaction. The size of the trade, the 2.3% execution discount, the absence of corresponding CME futures activity, and the limited universe of potential sellers collectively weigh against the view that the transaction represented a contemporaneous basis-trade unwind.

The key unanswered question is whether the seller was responding to idiosyncratic constraints or expressing a broader investment view. While the transaction details themselves cannot answer that question, they do, however, demonstrate that at least one sophisticated holder was willing to pay approximately $29.5 million to eliminate a $1.26 billion bitcoin-linked position immediately.