IN TODAY'S ISSUE:

- Attack on Fed independence sharpens the focus for bitcoin.

- We examine the key drivers that may be underpinning the recent strength across crypto markets.

- A sharp rally in privacy-focused coins may be signaling something important about today’s geopolitical environment.

With Fed Independence Under Pressure, Bitcoin’s Value Proposition Sharpens

Late last week, the Trump administration’s attacks on the Federal Reserve and its chair, Jerome Powell, escalated sharply when the Department of Justice served grand jury subpoenas to the U.S. central bank. Powell responded in a strongly worded video statement, arguing that the threat of criminal charges stemmed from the FOMC’s refusal to set interest rates at the president’s discretion. President Trump has repeatedly criticized the FOMC’s interest-rate policy, contending that rates were far too high and pressing for substantial cuts.

This isn’t the first time in the U.S.’s history that the executive branch tried to influence the Fed and monetary policy. In the lead-up to the 1972 election, President Nixon exerted pressure on Fed Chair Arthur Burns to hold interest rates down, an action now widely cited as a classic example of political interference that produced short-term economic gains but fueled persistent inflation and undermined monetary credibility for much of the 1970s. In 1965, President Lyndon Johnson personally confronted Fed Chair William McChesney Martin, shoving him against a wall, amidst interest rate hikes during the Vietnam War. The FOMC eventually resumed raising rates, but their delayed response is seen as contributing to the inflationary era of the 1970s. There are also numerous examples around the world, such as Turkey and Argentina, of politicians meddling in monetary policy.

History shows that political meddling in monetary policy is almost invariably bad - higher inflation, damaged central bank credibility, and weaker currencies are typical byproducts. (We even have one counterfactual example too, the UK, where central bank independence was formalized in 1997, which led to lower and more predictable inflation). This is hardly surprising. Politicians and central bankers have different objectives, with political incentives almost universally skewed toward accelerating benefits and deferring costs to appease voters, a mindset evident in the United States’ nearly $38 trillion debt load. Central bankers are more focused on maintaining credibility, the value of their currency, and responding to changes in inflation and employment.

Following news of the Fed subpoena, precious metals surged. Gold rose 4.1% over the past 7 days, while silver soared 21.4%. Bitcoin initially caught a bid on Monday before rolling over on Tuesday to test the $90,000 level, then rebounded to hit nearly $98K. If there were ever a clear use case for a non-sovereign store of value, this is it. Bitcoin proponents have long been skeptical of central bankers’ influence on currency values. What happens when political influence enters the equation?

Crypto Awakens from Long Slumber

Bitcoin finished the year lower, an outcome that surprised many investors given that Q4 has historically been a period of seasonal strength. While price action struggled through much of the quarter after putting up a new all-time high, the market appears to have found a bottom in mid-November, with bitcoin and ether troughing on November 21 and most other digital assets following in mid-December. Since then, the major assets are up approximately 20–25% from their lows, and the year has begun on firmer footing. Against this backdrop, investors have increasingly asked what is driving the recent improvement in market conditions. Below, we outline several factors we believe are contributing to the current market dynamics.

Tax Loss Selling

We’ll classify this one as an “absence of an overhang” rather than an explicit positive. Bitcoin was one of the few asset classes down in 2025 (link to our 2025 review), and many other digital assets fared worse. It may have suffered from tax-loss selling heading into year-end. Gains that investors might have recognized in other asset classes may have been netted against losses incurred from owning bitcoin. With tax-related activity now largely behind us, bitcoin and other digital assets are no longer facing the incremental selling pressure that may have weighed on prices.

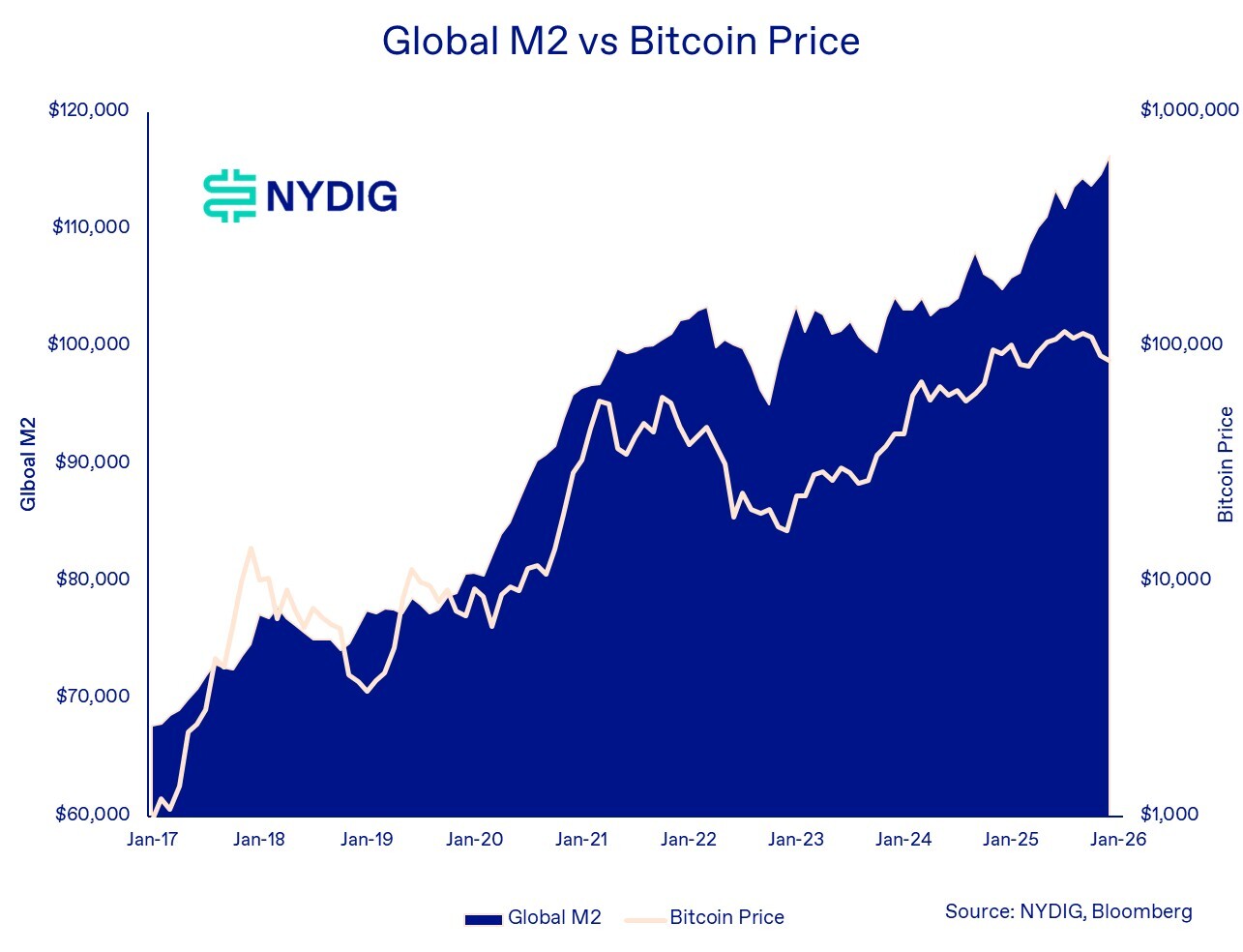

Global Money Supply Reaches New Highs

From our work on macro factors, global money supply (M2), along with real interest rates and inflation expectations, were some of the most important factors that affect bitcoin. The intuition is that as money continues to be pushed into the global economy without being funneled into the consumptive activities that comprise gross domestic product (GDP), it ends up being stored in capital assets, like bitcoin. Like any factor analysis, it doesn’t always work, which was frustrating in the back of last year, but the rise in global M2 continues nearly unabated.

Exchange Backstops Done Offloading Long Positions

If you haven’t read BitMEX’s research piece on the state of perpetual swaps, it’s one of the more eye-opening pieces, especially how exchanges operate and the context of the $19B liquidation event on October 10th (link). Essentially, exchanges operating under the “B-Book” model were left with unhedged long positions after auto-deleveraging (ADL) engines kicked in as traders were liquidated on their longs. The subsequent selling of these long positions was likely an overhang to prices in the weeks that followed. Fact: bitcoin only hit $107K on 10/10 — it didn’t hit its low of $80,524 (on Coinbase) until over a month later. It’s impossible for us, as outsiders, to judge the impact of exchange offloading, but it’s certainly plausible that this was an overhang that has now abated.

Catch Up Trade with Precious Metals

2025 was a banner year for precious metals, with gold, silver, platinum, and palladium up 67%, 149%, 144%, and 82%, respectively. Conversely, “digital gold” struggled last year, with bitcoin down 6%. Although our analysis indicates that gold and bitcoin respond to distinct macro dynamics, with effectively zero correlation between them, both highlight a broader reality: at a global scale, truly non-sovereign stores of value are exceedingly rare. For investors seeking that exposure, the menu of viable options is surprisingly limited. Even platinum and palladium are only $602B and $329B in total market value. The Swiss Franc? While bigger at $1.3T, is still smaller than bitcoin's market value at $1.9T, plus it's tied to a sovereign entity, as neutral as Switzerland might be. The reality is that for large and swift capital deployments into assets that are suited for the political and economic backdrop of 2026, bitcoin remains an important alternative.

Options Markets No Longer Constraining Spot

Throughout 2025, two market dynamics likely weighed on prices but have recently begun to fade. Bitcoin’s volatility, both realized and implied in options markets, continued a secular decline. Long-term holders increasingly engaged in call overwriting, which contributed to lower implied volatility, while spot bitcoin itself became structurally less volatile as the asset matured. As implied volatility compressed throughout the year, call selling became less attractive for these holders. When investors sell calls, dealers buy them and accumulate an inventory. To hedge that exposure, dealers sell spot as prices rise and buy spot as prices fall, a dynamic that can dampen upside moves and weigh on spot prices.

However, that dynamic appears to have flipped as we enter 2026. Call skew has turned positive, with calls trading richer than puts, suggesting increased demand for upside exposure rather than downside protection. In this environment, dealers are more likely to be short calls and short gamma. As a result, dealer hedging behavior may now reinforce price trends, requiring dealers to buy spot as prices rise and sell as prices fall, potentially amplifying upside moves rather than suppressing them.

Sell America Trade

The United States, long viewed as a stabilizing force in the global system, albeit with mixed results, is increasingly being perceived, both domestically and abroad, as less predictable, for lack of a better descriptor. A shift away from a stabilizing role toward a more confrontational posture has prompted investors to reassess geographic and asset allocation assumptions. We already have outlined that precious metals posted a banner year in 2025, but both emerging- and developed-market equities outperformed U.S. equity benchmarks, plus the U.S. dollar index (measured against other currencies) declined over the year. Bitcoin is a uniquely apolitical asset and may be a beneficiary of some of that rotation.

Privacy Coin Rally Might Be Telling Us Something

One of the major outperformers of 2025, with their rally beginning in earnest in Q4, were privacy coins such as Zcash (ZEC), Monero (XMR), and Dash (DASH), coins with embedded or optional features that anonymize the source and destination of funds. Bitcoin and other crypto networks, such as Ethereum and Solana, operate pseudonymously; that is, funds can still be traced on the blockchain, and as long as real-world entities are tied to addresses, the movement of funds between entities and individuals can be identified, made easier with blockchain analysis tools.

When enabled, privacy coins make transaction tracking either difficult or impossible, but the strength and implementation of privacy technology vary significantly by protocol. Monero enforces privacy by default and does not allow users to opt out, using ring signatures, RingCT, and stealth addresses to obscure the sender, transaction amount, and recipient. Zcash offers strong cryptographic privacy between shielded (z-address) transactions, hiding the source, destination, and amount through zero-knowledge proofs, but this functionality is optional. Dash, by contrast, provides optional privacy through PrivateSend, a CoinJoin-style mixing mechanism (similar to that used on Bitcoin) that obfuscates transaction details but does not fully anonymize it.

While the technical distinctions may be of interest to technologists, the more relevant takeaway for investors is that privacy-preserving crypto assets have been among the best-performing over the past 12 months. We believe this outperformance reflects growing sensitivity to the geopolitical backdrop discussed earlier, rising central bank intervention, and a shift in the U.S. from a stabilizing presence to a more confrontational actor. In that context, market performance suggests investors are increasingly assigning value to privacy as a core monetary feature, not a niche technical preference.

Market Update

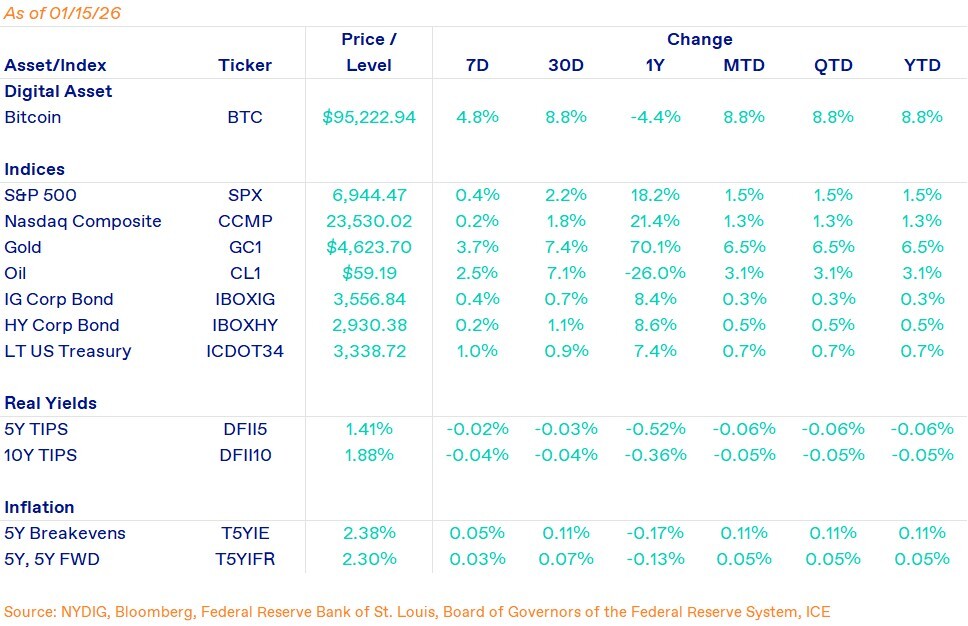

Bitcoin rallied 4.8% over the week and is now up 8.8% year-to-date. While the initial price bump following the DOJ probe in the Fed proved short-lived, sentiment shifted meaningfully a few days later as investors seemed to reassess bitcoin’s positioning in the current macro environment. As discussed earlier in this note, bitcoin appears uniquely suited for this moment, a view that seems to be starting to build some momentum.

Flows into bitcoin ETFs were notably strong, with approximately $1.8B of net inflows recorded from Monday through Thursday, reinforcing the idea that demand remains intact despite near-term macro uncertainty. This was a notable change from the prior week, the first full trading week of the year, which saw outflows of $666M.

Importantly for the longevity of a rally, there are few signs of speculative excess in the market. Despite higher spot prices, trader behavior appears relatively subdued. The front-month CME futures basis is running at roughly 4% annualized, with the second-month contract near 5%, levels that are well below those typically associated with exuberant positioning. Similarly, open-interest-weighted funding rates on perpetual swaps are currently around 4.7% annualized. During periods of heightened speculation, this metric can easily surge into the triple-digit range, underscoring how measured current positioning remains.

Important News This Week

Regulation and Taxation:

Senate Banking Committee Cancels Crypto Market Structure Markup - CoinDesk

Coinbase Pulled Support for Senate Crypto Legislation — Here's What Happened - The Block

Crypto Firms Buoyed by Trump Get Rocked as Crucial Bill Delayed - Bloomberg

Investing:

Jefferies Strategist Swaps BTC For Gold, Cites Quantum Computing Risk - CoinDesk

Interactive Brokers Unlocks 24/7 Funding With USDC, Plans to Rollout Ripple and PayPal Stablecoins Next Week - The Block

Companies & Technology:

Bitcoin Core Promotes First Trusted Keys Maintainer in Three Years - Protos

Project 11 - Blog - Announcing Project Eleven’s Series A - Project 11

MrBeast's Beast Industries Gets $200 Million Investment from Ether (ETH) Treasury Firm BMNR - CoinDesk

StanChart Said to Prepare Crypto Expansion With Prime Brokerage - Bloomberg

Upcoming Events

Jan 28 - FOMC interest rate decision

Jan 30 - CME expiry

Feb 11 - CPI release