IN TODAY'S ISSUE:

- With digital asset treasury companies (DATs) continuing to proliferate by the day, we conduct a thought experiment to see how things could unwind.

- If DATs are unable to sustain trading at a premium to NAV, they lose the main avenue to grow their treasuries on a per-share basis.

- We are already seeing warning signs emerge with specific DAT offerings, like one already trading below NAV less than 5 days after the announcement.

A Premortem on DATs

Digital Asset Treasury companies (DATs, we’re apparently calling them now) have become one of the defining features of this cycle. The funny thing is that nothing new this cycle, not regulation, not technology, not politics, nor legislation, uniquely enabled them. It’s just that corporations, in concert with Wall Street, figured out how to transmute $1 of crypto into $2 of equity value (with the help of investors). There’s some truth to this financial alchemy, though, simply because DATs can issue debt securities, levering their balance sheet, with the fulcrum advantaging equity holders.

Today, corporations (not exclusively DATs, those are a special beast) hold 976K bitcoins according to Bitcointreasuries.net, nearly 5% of all bitcoins in existence, a dollar figure amounting to over $115B. And with DATs spreading like the ghost grass of Dothrakian nightmares to every imaginable digital asset, the total figure of crypto held by corporations is about $120B according to The Block, implying bitcoin’s “DAT dominance” is nearly 96%.

But unlike ghost grass, the fictional vegetation that threatens to spread across every inch of Westeros, blotting out all life, there has to be some logical end to DATs. If there wasn’t, then the end state of the industry would be something like ghost grass for the industry - DATs continue to sell equity for $2 and purchase $1 of crypto, purchasing all of the crypto in existence.

Leverage isn’t the Issue

How does this cycle end, or what cracks it? A lot of people think it has to do with leverage, and while that might be the case for some companies, it’s not a chief worry for us. Using MSTR as an example, the company has nearly $75B in bitcoin and only $14.6B in notional debt instruments outstanding. Bitcoin would have to fall 81% for the principal on its debt to not be covered. Its annual interest expense is only about $615M, more than covered by its bitcoin holdings or any income-generating opportunities it has with its holdings. Could debt become an issue for DATs at some point? Yes, but right now it’s a red herring.

The bigger risk, to us, is simply that the market fails to continue to place a premium on DAT crypto holdings, that $1 of crypto isn’t worth $2 of equity. And here we are starting to see some cracks emerge. Because of this, we think it’s instructional to undergo a “pre-mortem,” a hypothetical risk exercise that attempts to identify why something failed before it even happens.

The Design of DATs

As a refresher, a key measure for DATs is the amount of crypto they own per share (ignore the basic fact that the equity has no direct claim on the corporate crypto). These companies increase their crypto per share using one or more of only 3 available options to acquire crypto: 1) issuing equity at a premium to NAV (or buying back stock trading below NAV) 2) issuing debt securities and levering up (or using excess/opco generated cash) 3) active treasury management. By far and away the most popular strategy has been for DATs to issue stock at a premium to NAV followed by issuing debt as a distant second. Only a couple of companies have even tried active treasury management.

With that as a precursor, DATs are extremely reliant on their stock trading above NAV. Where does this premium come from? While there’s a quantifiable source, leverage, most of that premium comes from narrative, a memetic premium based on the figurehead at the company – you know them by name. But what makes one company’s memetic premium greater than another’s? Got us, but the variability is huge – some companies trade at discounts to NAV, while on the high end, Nakamoto once traded at 24x NAV. There does seem to be a time component to the premium, though, where newer companies, especially ones with no prior connection to crypto or without an identifiable figurehead, are receiving lower premiums over time. This makes sense because, if all the DAT is doing is issuing stock to buy crypto, it should trade at no premium to NAV – these are called ETFs.

Maintaining Premium to NAV is Key

Where a DAT gets into trouble is when it cannot generate and sustain a sufficient premium to NAV – it loses its main avenue to increase its crypto per share. How does this happen? Either it fails to generate sufficient memetic premium or investors sell shares, forcing the premium to NAV to collapse. If the stock trades at a discount to NAV, the DAT can sell its crypto to buy back stock, generating a positive crypto yield, but then the company risks the impact of becoming a dwindling treasury company. Not exactly what investors or the company want.

The issue of DAT investors selling shares to reduce the premium to NAV is a real problem. Most of these DATs come to life by selling 95%+ of their stock, all of which becomes freely tradeable all at once. If the DAT doesn’t reserve some of its fundraise to sop up this onslaught of liquidity from investors, its premium to NAV can be materially impacted. Using this excess cash to buy back stock at a premium to NAV is yield minimizing, as we showed in our BMNR example 2 weeks ago, but it’s an attempt to preserve this premium that the company has to its NAV, a valuable feature.

Easy Come, Easy Go

It's important to remember that, just as easily as this “memetic premium” has emerged, it can disappear. MSTR traded for 2 years, 2022 – 2023, at zero premium or even a large discount to NAV (link). There’s no fundamental reason these premiums must persist. This “trade” reminds us a lot of the “GBTC arb”, the trade that famously blew up, taking down with it nearly the entire crypto industry. Our gut is that these premiums to NAV seem to be positively correlated to price. If crypto were to undergo a price correction, we guess that these premiums would collapse as well.

Warning Signs Flashing

There are recent examples of DATs failing to gain memetic premium, a failure to achieve flight, which offer stark warning signs to us. One such example is ALT5 Sigma (ALTS), which raised $1.5B in 2 simultaneous deals, a $750M registered direct offering (RDO) with World Liberty Financial, Inc. and a $750M PIPE, to build a DAT in WLFI tokens, the governance tokens of World Liberty Financial, the DeFi platform closely associated with President Trump. With the deals priced at $7.50/sh, despite some suspicious price and volume action in the 2 days leading up to the deal announcement, shares closed Friday trading at $5.94, well below the deal price and thus NAV of the underlying WLFI tokens. This is even though WLFI tokens are presently immobile, not moveable on the blockchain, and thus cannot be sent to ALTS for treasury holding (Etherscan token link).

There’s one more wrinkle here. The RDO that World Liberty Financial, Inc. led is, well, registered. World Liberty’s ALTS shares are thus freely tradeable, while the shares for PIPE investors are not. Given that trading volume for ALTS rose from $1-2M/d before the deal (excluding the very noticeable bump to $4-$5mm traded on the Thursday and Friday before the deal was announced) to over $100M/d since, it’s possible, although we don’t know for sure, that World Liberty traded out of some of its position already, while PIPE investors are stuck, already sitting on losses.

Summing it Up

This is our premortem, how things could end up for DATs. Either crypto prices decline or DATs collectively exhaust the demand from traditional market investors - these DATs only work so far as investors can make money. Premiums to NAV contract. For companies trading below NAV, they will decide to sell the underlying assets to buy their stock, weighing on crypto prices, further exacerbating issues for DATs. If they don’t buy their stock at a discount to NAV, we’re sure there are plenty of activist funds willing to help them make this decision; it’s not even a complicated analysis. The whole thing works like the current cycle, but in reverse. It doesn’t have to end up like this, however, and this is just one possible future state.

We are often looking for signs of froth in the market. Historically, those have appeared in crypto native markets. But this is the first crypto cycle where traditional investors are fully engaged. Given some of the things happening in traditional capital markets, like these dynamics with DATs as well as other publicly traded crypto companies, the froth seems to be stemming from traditional financial market investors this time around.

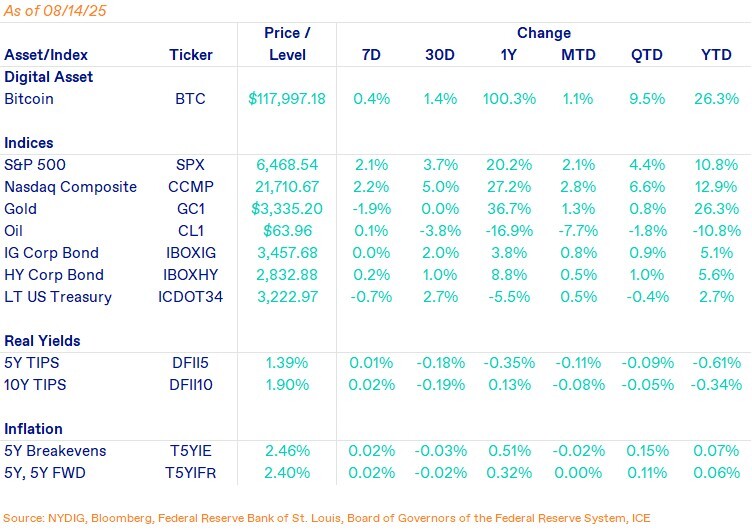

Market Update

Bitcoin hit a new all-time high again this week, breaking $124K for the first time, before retreating on a higher-than-expected inflation reading from the PPI on Thursday, which was a marked change from the in-line CPI reading on Tuesday. If indeed inflation is starting to pick up, and the jobs number that resulted in the firing of the BLS chief is at least directionally correct, the economy may be setting for stagflation – stagnant economic growth and ramping inflation. We’ll see how the Fed is thinking about handling the situation with the Jackson Hole conference coming up at the end of next week.

Even though bitcoin hit new all-time highs this week, its dominance has been on the decline since peaking at over 70%. Ethereum has sprung to life after bottoming against BTC (ETHBTC) in early May. This dynamic happens in every crypto cycle though, where bitcoin sheds dominance but continues to go up in price. Historically, bitcoin’s price and the cycle have peaked when bitcoin’s dominance is around 40%. Given that we are still at 60%, it still seems like a ways to go for bitcoin and the cycle.

Important News This Week

Investing:

Behind Wall Street’s Abrupt Flip on Crypto - Source

Scott Bessent Suggests Government Bitcoin Purchases Remain a Possibility - CoinDesk

Regulation and Politics:

Who Is Patrick Witt, President Trump's Next Senior Adviser on Crypto? - CoinDesk

Do Kwon Pleads Guilty to US Fraud Charges In $40 Billion Crypto Collapse - Reuters

Justin Sun Sues Bloomberg Over Plans to Publish 'Confidential' Crypto Holdings - Bloomberg

Companies:

Elon Musk’s SpaceX Bitcoin Holdings Top $1 Billion As BTC Hits Fresh Highs - The Block

Western Union Mulls Its Own Stablecoin as Payments Rivalry Grows - Bloomberg

Stripe Building ‘Tempo’ Payments Blockchain with Paradigm - Fortune

Upcoming Events

Aug 21 - Jackson Hole Economic Policy Symposium

Aug 29 - CME expiry

Sept 17 - FOMC interest rate decision