IN TODAY'S ISSUE:

- Bitcoin had a difficult start to the year, declining 22.6% in Q1. While weak by historical standards, negative Q1 performance has not been a reliable indicator of full-year performance.

- Performance in Jan and Feb was affected by the delay in the CLARITY Act, AI fears, and monetary policy concerns with the nomination of a new Fed Chair.

- Since the conflict in Iran erupted, bitcoin is one of the few assets higher, while other safe-haven assets like gold and U.S. Treasuries are down.

- Artificial Intelligence is hitting bitcoin on two fronts: fears are weighing on long-duration assets such as bitcoin, while miners are selling their coins to fund AI buildouts.

- Quantum computing is the hot button issue for crypto investors. Potential impacts are still well into the future, and solutions are available today. The issue is going to be at the social layer – getting the community to agree on a path forward.

- DATs were highly active this quarter with major players such as Strategy and Metaplanet continuing to add to their positions, but many smaller players are trading below NAV, causing them to sell their bitcoins or hold off on purchases.

- Drawdown metrics suggest we are roughly 1/3 through prior-cycle patterns and tracking slightly better than historical drawdowns at comparable stages, while on-chain data indicates only a partial cycle reset.

PERFORMANCE REVIEW

Bitcoin Stumbles to Start the Year but Stabilizes with Iran Conflict

Bitcoin had a difficult start to 2026, posting one of the weakest performances across major asset classes in Q1, down 22.6%. The weakness was concentrated early in the quarter, with sharp declines in January and February before prices began to stabilize in March, coinciding with rising geopolitical tensions, including the conflict between the U.S. and Iran.

Beneath the surface, structural selling played a key role. Miners and large holders were consistent sources of supply, while the mid-year 2025 enthusiasm around digital asset treasury (DAT) companies has faded, with some participants turning into sellers. Bitcoin ETF flows were very mixed, with bitcoin ETFs showing a net outflow of $474M in the quarter. That said, not all institutional demand disappeared. Strategy (MSTR) remained a notable and persistent buyer, helping to provide support throughout the quarter.

In contrast, traditional asset classes showed a very different leadership profile. Energy-related assets dominated, with oil surging over 70% and volatility also spiking, while commodities broadly delivered strong gains. Energy equities followed suit, significantly outperforming most other sectors. Gold ended the quarter slightly higher, but that headline gain obscures a volatile path, with two sharp drawdowns along the way. The swings suggest investors may have become overly optimistic about the strength of its “safe haven” appeal.

Equity markets saw a clear rotation. Large-cap and growth-oriented segments, particularly technology and AI-sensitive stocks, struggled meaningfully, while value, defensive sectors (like utilities and consumer staples), and small caps held up better or posted gains. This shift reflects a broader change in market leadership, as investors moved toward more resilient, cash-flow-generating areas. Concerns around AI, both its economic and societal implications, added pressure to software and other long-duration growth assets, a dynamic that also weighed on bitcoin, given its sensitivity to liquidity and forward-looking narratives.

Weak Q1 by Historical Standards, but Not Determinative of Full-Year Performance

From a historical perspective, Q1 2026 stands out as one of the weakest starts to a year for bitcoin, with a return of -22.6%, ranking 13th out of 16 observed years. This places it firmly in the lower tail of quarterly outcomes and well below both the historical mean (+52.8%) and median (+3.2%) for first quarters.

For institutional investors, the context is important. Historically, every positive Q1 has been followed by a positive full-year return; however, negative Q1 outcomes have not always translated into negative annual performance. In other words, early strength has been a consistent signal, but early weakness has not been determinative. That said, the magnitude of this year’s drawdown, alongside shifting macro dynamics and softer marginal demand from prior structural buyers, points to a more cautious near-term outlook and reinforces bitcoin’s role as a high-beta, liquidity-sensitive asset within diversified portfolios rather than a defensive allocation.

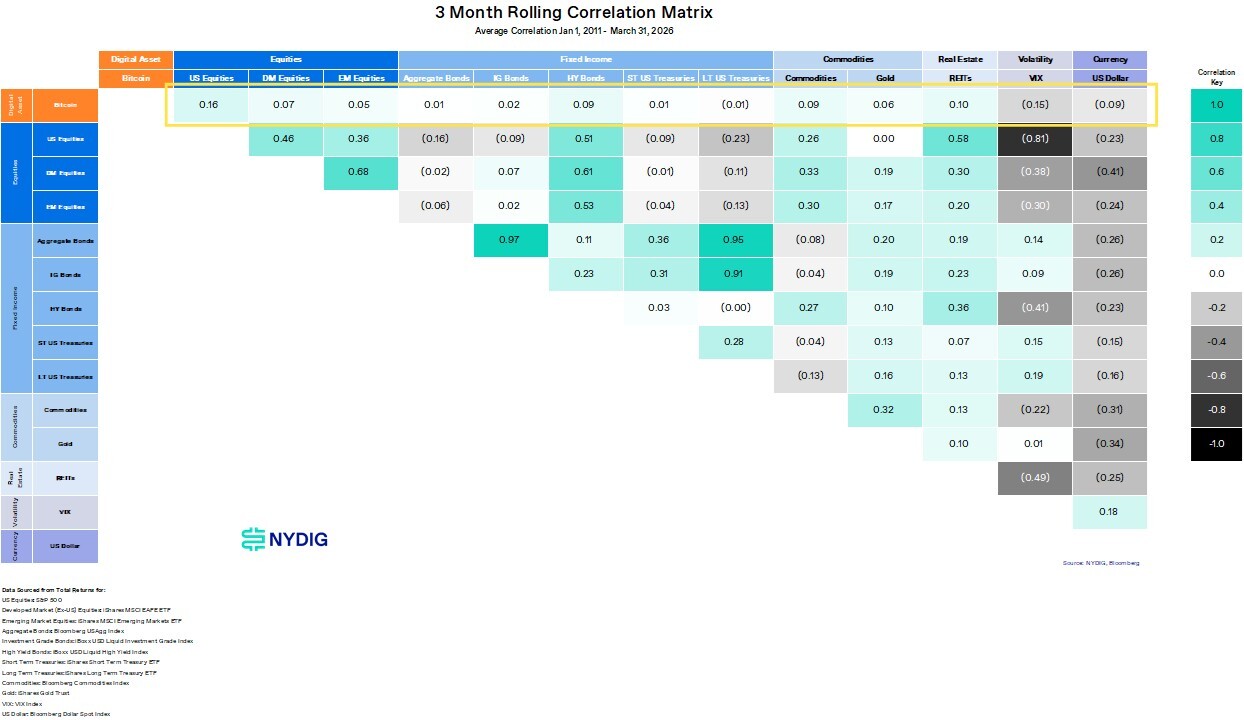

Equity Correlations Remain High

Bitcoin’s relationship with traditional macro assets continues to evolve, with a clear post-COVID regime shift. Before 2020, correlations with equities were inconsistent and often low, occasionally even negative. Since then, however, the baseline has moved structurally higher, with correlations spending much more time in positive territory. More recently, that relationship has strengthened again, with bitcoin’s correlation to U.S. equities rising back toward levels last seen in 2023, suggesting a renewed coupling with broader risk markets.

By contrast, bitcoin’s correlations with gold and the U.S. dollar remain low and unstable. The relationship with gold, often cited in the “digital gold” narrative, continues to alternate between positive and negative, while the inverse relationship with the dollar, though somewhat more consistent, is still volatile and unreliable. Taken together, the key takeaway is that bitcoin’s most durable linkage today is to equities, reinforcing its role as a liquidity-sensitive asset.

The correlation matrix reinforces that bitcoin’s relationships with traditional asset classes are, in practical terms, at a level generally considered zero. This includes equities, where long-term correlations with U.S. (0.16), developed (0.07), and emerging markets (0.05) are minimal, despite the much higher correlations observed in the post-COVID period. That contrast highlights a clear regime shift. Bitcoin has traded more like a risk asset in recent years, but over the full sample, its equity linkage remains weak. Similarly, correlations with fixed income are effectively nonexistent, and relationships with gold (0.06), commodities (0.09), and the U.S. dollar are negligible. Taken together, the data suggest that while bitcoin can exhibit episodic co-movement with equities, particularly in the post-2020 environment, its longer-term profile remains largely uncorrelated, supporting its role as a potential diversifier in institutional portfolios.

THE EVENTS THAT SHAPED THE QUARTER

Legislation Stumble Weighs on Industry

Momentum around U.S. crypto regulation took a step back at the start of the year as the CLARITY Act failed to advance out of markup, weighing on broader industry sentiment. The setback highlights ongoing friction between the crypto and banking sectors, particularly around the treatment of stablecoin rewards, which remains a key point of contention. This comes at a time when regulatory progress had been a major pillar supporting bitcoin’s strength since the 2024 election, and the reversal has contributed to a more cautious tone across the market. While legislation is still actively being worked on and remains a priority after years of industry advocacy, the window for meaningful progress is narrowing with the looming midterm election.

That Did Not Stop the Advancement of Regulation

Importantly, the legislative setback has not halted regulatory momentum. U.S. agencies continued to advance the framework in Q1, with the SEC and CFTC stepping up coordination through formal information sharing and a more unified approach to oversight. Together, they also moved toward greater clarity on token classification, including emerging efforts to distinguish commodities from securities and introduce more functional categorizations of digital assets. In parallel, the SEC issued interpretive guidance addressing how securities laws apply to activities such as staking and mining, while the OCC released guidance tied to the GENIUS Act, signaling a clearer path for banks engaging with crypto and stablecoins. Additional work from the Federal Reserve and Treasury around stablecoin oversight and market structure further underscores that, even without near-term legislative success, regulators are actively defining an institutional U.S. crypto framework.

Institutions Keep Building in Crypto

Despite the legislative and market headwinds, institutional engagement in crypto continued to grow in Q1. Traditional financial players are deepening their involvement, highlighted by the NYSE’s push into tokenized securities and its parent company, ICE, making a strategic investment in OKX. At the same time, Kraken Financial secured a Federal Reserve master account, a significant milestone that strengthens the bridge between digital asset firms and the U.S. banking system. Additional developments, including expanding custody offerings from major banks, growing ETF and structured product pipelines, and increased participation from asset managers and payment firms, underscore a broader trend. Institutional adoption is progressing steadily, with infrastructure, market access, and regulatory clarity all moving incrementally forward.

AI and Quantum Computing Fears Weigh on Bitcoin

Concerns around artificial intelligence have begun to weigh on bitcoin and other long-duration assets, as more pessimistic narratives around AI’s economic impact gain traction. In the “AI doomer” scenario, rapid advances in automation threaten large swaths of knowledge work, potentially leading to structurally higher unemployment, weaker aggregate demand, and a deflationary macro environment. In such a world, the ability of households and businesses to service debt could deteriorate, raising broader financial stability concerns. For investors, the key question is what happens to demand for risk assets, particularly those like bitcoin that rely heavily on forward-looking growth narratives and liquidity, if economic activity and income generation come under sustained pressure.

At the same time, a separate but increasingly discussed risk comes from advancements in quantum computing (QC), which have more direct implications for cryptocurrencies. Recent progress from major technology companies like Google, alongside academic research, has highlighted the accelerating pace of development in quantum capabilities. Even under aggressive timelines, the risk is not viewed as imminent. However, the concern is that sufficiently advanced quantum systems could ultimately compromise the cryptographic foundations, particularly digital signatures, that secure bitcoin ownership. Unlike macro-driven risks, this is a protocol-level concern, and while potential mitigations such as quantum-resistant cryptography are already available, the uncertainty has contributed to a more cautious sentiment among institutional investors evaluating long-term risks.

Bitcoin Rises Modestly While Other Safe-Haven Assets Struggle in the Wake of Iran Conflict

Bitcoin showed notable resilience in the wake of the February 28 U.S. - Israel strikes on Iran, holding up and even posting gains in a market environment dominated by geopolitical stress. While the expected winners, oil, volatility, commodities, and energy equities, led performance, bitcoin also moved modestly higher. This is particularly notable given that risk assets broadly struggled, with equities across regions and styles largely negative in the period.

What’s more striking is the breakdown in traditional safe-haven behavior. Gold and silver both declined sharply, while U.S. Treasuries also sold off, with long-duration bonds down around 4%. Rather than a flight to safety, markets repriced toward higher yields, likely reflecting a combination of rising oil-driven inflation pressures, tighter policy expectations, and an increase in real yields. Importantly, even TIPS fell, indicating that real rates were rising faster than inflation expectations or that investors were broadly de-risking across fixed income. Taken together, the move suggests that concerns extended beyond inflation alone, encompassing tighter financial conditions and macro uncertainty, making bitcoin’s positive performance stand out even more in a period where traditional hedges failed to provide protection.

Prediction Markets and Crypto Trading Converge

Speculation markets continued to expand in Q1, with both crypto-native and traditional financial platforms increasingly embracing prediction markets as a new trading frontier. Coinbase launched prediction market trading powered by Kalshi, bringing regulated event-based contracts to a broad U.S. user base. At the same time, traditional platforms like Robinhood are moving into the space through partnerships and industry initiatives, highlighting a growing convergence between crypto infrastructure and retail trading ecosystems as prediction markets gain traction across both segments.

Regulators such as the CFTC have taken a more constructive but active stance toward this growth. The agency has signaled support for the “responsible development” of prediction markets and is actively working on new rulemaking to establish clearer frameworks for event-based contracts, while also asserting its exclusive jurisdiction over the space as a derivatives market rather than gambling. At the same time, enforcement remains a priority, with the CFTC emphasizing oversight around manipulation, insider trading, and market integrity as participation broadens. Taken together, the trend points to prediction markets becoming an increasingly institutionalized segment of both crypto and traditional finance, supported by growing infrastructure but still evolving within a complex regulatory backdrop.

DATs and Miners Make Marked Shift

Q1 marked a clear shift in structural flows as both DAT participants and miners moved from consistent buyers to a more mixed, and at times net-selling, cohort. While large players like Strategy (MSTR) and Metaplanet remained steady accumulators, others, such as Nakamoto and Empery Digital, turned into sellers. At the same time, miners emerged as a significant source of supply, with several firms selling bitcoin to fund operations and, increasingly, to finance a strategic pivot toward AI and high-performance computing. Companies like Core Scientific, Riot Platforms, TeraWulf, Applied Digital, and IREN have all leaned into this transition, repurposing energy-intensive infrastructure for AI workloads and, in some cases, monetizing BTC holdings to do so.

LOOKING AHEAD

DAT Behavior Will be Determined by Premiums/Discounts to NAV

DATs have become an important marginal flow driver, and their impact on bitcoin will hinge on how they trade relative to NAV. The dynamic is straightforward. DATs at a premium can tap equity markets and deploy proceeds into additional bitcoin purchases, reinforcing demand, while those at a discount are effectively shut out of issuance and instead face pressure to repurchase stock, which may require selling bitcoin or encumbering it to raise cash via borrowing. After serving as a strong demand engine in 2025, the group has already begun to diverge, and this dispersion is likely to persist. In practice, this increasingly resembles a single standout, Strategy (MSTR), sustaining a premium and continuing to accumulate, with Metaplanet and Strive currently trading right around NAV. The other bitcoin DATs trade below NAV, limiting their ability to add bitcoin, and in some cases, turning them into a source of supply, particularly during weaker market conditions.

Regulatory Progress vs. Delay

The regulatory backdrop remains a balance between legislative efforts and incremental agency-driven progress.

The stablecoin yield/deposit-flight dispute, the last major sticking point for the CLARITY Act, appears close to resolution after a second round of compromise language was reviewed by crypto and banking stakeholders last week, with both sides cautiously optimistic. The Senate Banking Committee markup is widely expected in the final two weeks of April, with remaining open issues around DeFi, tokenization, and token classification still needing closure before then. May will be a pivotal month for the next step in crypto legislation.

Regulatory momentum is shifting toward agency-led implementation and supervision, which is already reshaping the crypto market structure. The SEC is prioritizing incremental changes, expanding custody options, refining broker-dealer participation, and tightening disclosure standards, rather than sweeping new rules, thereby facilitating institutional access through regulated channels. At the same time, the CFTC is advancing its role as the core market-structure authority, promoting developments in spot market infrastructure, tokenized collateral, and derivatives integration to support deeper liquidity and more mature trading venues. Meanwhile, banking regulators, including the Fed, OCC, and Treasury, are moving to formalize crypto’s role within the financial system, particularly through frameworks governing stablecoins, bank issuance, reserve requirements, and balance sheet treatment. Institutional integration will be increasingly defined by products that align with these emerging regulatory pathways.

AI is Not Going Away – The Narrative Spillover

AI has emerged as a cross-asset narrative with meaningful second-order effects on bitcoin. On the macro side, more pessimistic views around AI-driven disruption, particularly the risk of large-scale displacement of knowledge workers, have fueled concerns about weaker aggregate demand, deflationary pressures, and a diminished bid for long-duration assets like bitcoin. This likely overstates the downside, given that every past technological shift has ultimately created new jobs, functions, and businesses even as some roles were displaced or replaced entirely.

More tangibly, AI is already influencing crypto through the supply side. Miners are increasingly reallocating capital toward AI and high-performance computing infrastructure, often financing that shift through bitcoin sales. If mining economics remain under pressure, this could persist as a steady source of supply.

AI won’t be a fad, though. While the sector may experience cyclical corrections, adoption will increase over the long term, meaning investors will need to adapt to a landscape where AI is both a threat and an opportunity.

Quantum Risk: A Technical Problem with a Social Bottleneck

Quantum computing has increasingly become the “tail risk” front of mind for institutional investors, and recent research has made it even more acute. Two papers published March 30–31 have modestly pulled forward expectations for 'Q-day.' One, from Google Quantum AI, reported improved logical qubit scaling and error rates; the other, from a Harvard-Quantinuum-Caltech team, demonstrated more resource-efficient implementations of Shor's algorithm. The direction of progress is clear: hardware is improving, algorithms are becoming more efficient, and the overhead required for error correction is gradually declining. That said, the remaining hurdles are still substantial. Fault-tolerant, large-scale quantum systems are not imminent, and meaningful cryptographic break risk likely remains years away.

From a mitigation standpoint, the technical path is relatively well understood. Post-quantum (PQ) signature schemes already exist, along with interim measures such as avoiding address reuse (public key exposure). Thus, the challenge is less about creating something new and more about coordination. Bitcoin’s governance model, while a strength in many respects, makes rapid protocol change extremely difficult, even for comparatively minor upgrades. A transition to PQ cryptography would require broad consensus across developers, miners, exchanges, custodians, and users, as well as the handling of coins that cannot be moved. In that sense, the binding constraint is social, not technical. The ecosystem has historically struggled to align on even low-stakes changes, and a quantum transition would be orders of magnitude more complex. For investors, the takeaway is that quantum risk is evolving from a distant hypothetical to a longer-dated but credible scenario, one where preparedness is possible, but execution risk around coordination remains the central uncertainty.

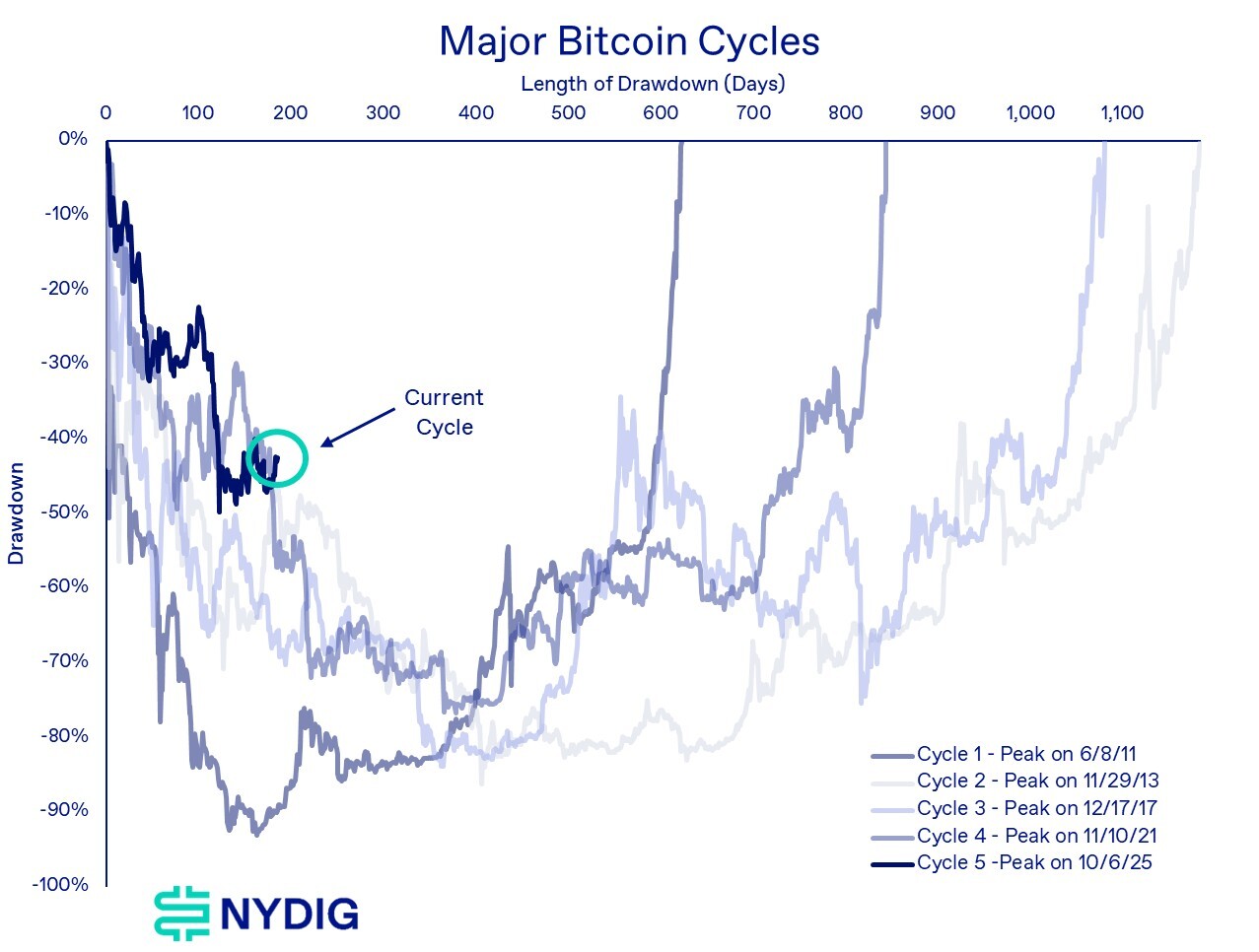

Assessing the Depth and Duration of the Current Bitcoin Drawdown

The key question for institutional investors is whether the worst of the current drawdown is already behind us. Bitcoin has declined approximately 52.5% from its all-time high, bottoming in February at nearly $60,000. While significant, this correction is notably shallower than prior cyclical drawdowns, which have typically exceeded 77% peak-to-trough declines and unfolded over much longer time horizons.

From both a magnitude and duration perspective, the current cycle appears atypical. The recent low was reached just 123 days after the all-time high, compared to roughly 363–376 days in the previous two cycles, suggesting a materially compressed timeline. At the same time, the depth of the drawdown is only about two-thirds as severe as prior episodes. Taken together, this implies a partial, rather than complete, cyclical reset. While it remains impossible to definitively call a bottom, these dynamics suggest the correction may be incomplete relative to past cycles, even as it has progressed more quickly.

Drawdown Comparisons

The current bitcoin drawdown is broadly tracking in line with or better than past cycles at a comparable stage. This indicates the market has already advanced meaningfully through the typical bear cycle path. If the drawdown follows past cycles from here, a meaningful additional downside remains. However, tracking stronger than historical drawdowns at this point suggests the market may be exhibiting increased structural resilience.

MVRV Ratio (Market Value to Realized Value)

The MVRV ratio, which compares bitcoin’s market value to its aggregate cost basis (realized cap), is a key gauge of valuation and investor profitability. Historically, cycle bottoms have coincided with MVRV falling below 1.0, signaling that the market is broadly underwater and in a capitulation zone. In the current cycle, however, MVRV has approached but not meaningfully broken below 1.0, remaining slightly above this threshold. This suggests that, unlike prior bottoms where widespread losses were fully realized, the market has not yet reached the same degree of valuation compression typically associated with cycle lows.

PSIP (Percent Supply in Profit)

The Percent Supply in Profit (PSIP) measures the share of bitcoin supply currently held above its cost basis, serving as a gauge of how broadly profits or losses are distributed across the market. Historically, cycle bottoms tend to form when PSIP compresses into the mid-range (~45–55%), reflecting widespread pain and a broad distribution of unrealized losses. In the current cycle, PSIP has declined into this range, hovering around the 50% level, which is consistent with prior late bear phases. This suggests that a meaningful portion of the market is now near or below cost basis, indicating that the necessary conditions of broad financial stress are largely in place, though not yet sufficient on their own to confirm a bottom.

LTH-SOPR (Long-Term Holder Spent Output Profit Ratio)

The LTH-SOPR measures whether long-term holders (coins held ≥155 days) are selling at a profit or loss, providing a direct view into the behavior of the strongest hands in the market. When LTH-SOPR falls below 1.0, it indicates that long-term holders are selling at a loss, reflecting capitulation from historically resilient participants. In the current cycle, LTH-SOPR has dipped below 1.0, consistent with prior bear market lows where strong-hand capitulation occurs. This signals that even long-term holders are realizing losses, a necessary condition for market bottoms, though confirmation requires a sustained reclaim back above 1.0 to indicate that selling pressure has been exhausted.

aSOPR (Adjusted Spent Output Profit Ratio)

The aSOPR (Adjusted Spent Output Profit Ratio) measures whether the overall market is selling coins at a profit or loss, filtering out short-term noise to better capture underlying behavior. When aSOPR falls below 1.0, it indicates that coins are being moved at a loss, reflecting broad-based capitulation across market participants. In the current cycle, aSOPR has dipped below 1.0, consistent with prior bear market conditions where sustained loss-taking dominates. This suggests that the market has entered a phase of widespread realized losses, though a confirmed bottom typically requires a sustained reclaim above 1.0, signaling that selling pressure has been absorbed and market behavior is shifting.

Putting it All Together

Taken together, the data suggest the market is in the late stages of a bear phase, though a confirmed bottom has yet to form. The depth of the drawdown remains moderate compared to previous cycles, MVRV has not fully entered capitulation territory, and PSIP indicates broad, but not extreme, levels of distress. Meanwhile, both LTH-SOPR and aSOPR continue to show losses being realized.

Overall, this points to a market that has made significant progress through its decline but has not yet reached true seller exhaustion. Signs of a durable bottom are emerging, but confirmation has yet to materialize.