IN TODAY'S ISSUE:

- STRC issuance has been a primary driver of incremental bitcoin demand lately, with prefs surpassing $10B and overtaking converts in MSTR’s capital stack.

- These instruments are not traditional credit. They are actively managed, BTC-supported liabilities where capital markets access, not cash flow, is the key factor.

- A powerful reflexive flywheel is at play. When prefs trade near par and equity at a premium, issuance fuels BTC accumulation, but this dynamic can abruptly halt if market confidence falters.

STRC, SATA, and the Emergence of Managed Bitcoin-Backed Liability Structures

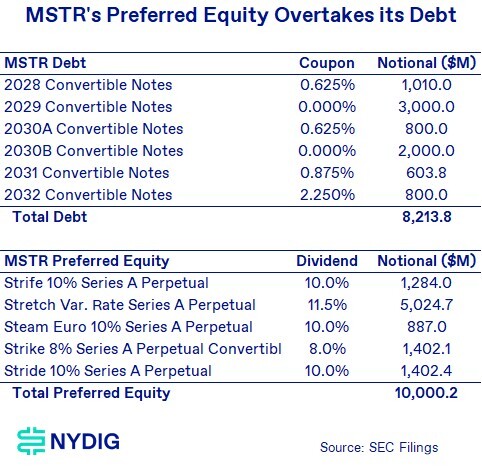

Growing issuance of Strategy’s (MSTR) Stretch Variable Rate Perpetual Preferred Equity (STRC) has been driving large-scale bitcoin purchases recently, making the instrument a key driver of incremental bitcoin demand. Over the past week alone, the company issued approximately $1.2B of STRC, bringing total STRC outstanding to just over $5B. When combined with an additional $5B of other preferred equity, total preferreds now exceed $10B, surpassing the firm’s convertible debt stack, and making novel financial instruments an essential part of its bitcoin accumulation strategy.

This dynamic has captured the attention of institutional investors, who are increasingly focused on the implications of these financing structures for both bitcoin and markets. As visibility has increased, so too has public discourse, with a range of bullish and bearish interpretations emerging across the community. However, evaluating STRC and analogous instruments such as Strive’s (ASST) SATA requires a shift in analytical framework. These securities are not well understood through the lens of traditional credit or equity; rather, they are best viewed as actively managed, capital markets–dependent liability structures backed by a reserve asset, bitcoin.

STRC and SATA are not Debt and Should not be Evaluated as Such

STRC and SATA differ meaningfully from conventional corporate credit. They are technically preferred equity, ranking junior to debt but senior to common equity, and their economic characteristics are unique. They are unsecured, feature variable and fully discretionary dividend policies, and provide limited governance rights to investors. Importantly, issuers are explicitly managing these instruments with the objective of maintaining price stability around par (typically $100), using a combination of signaling, dividend reserve management, and, most critically, active adjustment of periodic dividend rates.

Capital Markets Access, not Cash Flow, is the Binding Constraint

These instruments are not funded by operating cash flow, nor are they designed to be serviced through corporate earnings. Instead, they function as capital markets vehicles in which preferred securities are the core funding product, and the corporate balance sheet, anchored by bitcoin holdings, is constructed to support ongoing issuance. As a result, traditional credit metrics such as EBIT-to-interest coverage are not the appropriate lens for evaluating sustainability.

The binding constraint is not income generation, but the combination of continued access to capital markets and sufficient asset coverage. While some argue that interest coverage is the key metric, often based on the assumption that Strategy “never sells bitcoin,” the company’s own filings describe a far more flexible model. Strategy explicitly contemplates funding bitcoin accumulation through ongoing issuance of equity, debt, convertible securities, and preferred stock, as well as the potential sale of bitcoin, the use of bitcoin as collateral, and the development of income-generating strategies tied to its holdings.

The economic model is not one in which operating earnings service the capital structure. It is one in which the issuer maintains a large asset base, preserves investor confidence, and sustains access to funding channels.

Credit Stack Durability: Limited Triggers

The broader credit stack, including both debt and preferred securities, at Strategy and Strive, is generally more durable than much of the public analysis suggests. At Strategy, debt is typically unsecured and carries limited financial or restrictive covenants unless explicitly specified. Default is primarily triggered by payment failure or bankruptcy, not mark-to-market declines in asset values. Importantly, this framework extends to the preferred layer as well. While structurally junior and more exposed to discretionary outcomes, these instruments are not subject to hard triggers tied to bitcoin price movements or coverage ratios.

As a result, there is no automatic mechanism that forces bitcoin liquidation simply because bitcoin declines or because traditional coverage metrics deteriorate. This distinguishes the structure from conventional corporate credit, where asset volatility or covenant breaches can accelerate distress. The more relevant questions are whether issuers like Strategy and Strive can maintain access to capital markets, continue issuing across the stack (debt, converts, and preferred such as STRC and SATA), and actively manage their liabilities through market cycles.

Risks: Governance and Subordination

The appropriate way to assess risk in STRC and SATA is through the lens of governance and subordination rather than focusing solely on payment risk. Strategy’s base prospectus makes clear that the company retains broad flexibility to issue additional common equity and multiple series of preferred stock over time, with proceeds potentially used to acquire more bitcoin, while SATA holders have only limited protections against additional senior preferred issuance. Within this framework, risks extend beyond non-payment. New issuance can add senior claims ahead of existing holders, dividends are discretionary, and growing preferred layers can dilute recovery.

The Flywheel: How Capital Markets Access Drives Bitcoin Accumulation

At the core of these structures is a capital markets–driven flywheel in which funding capacity, bitcoin accumulation, and market confidence reinforce one another. When functioning, preferreds like STRC and SATA trade near par, enabling issuers to raise capital against a backdrop of strong asset coverage and positive market perception. Proceeds are deployed into bitcoin, expanding the asset base and NAV. When equity values trade at a premium (mNAV > 1), stock issuance becomes accretive on a bitcoin-per-share basis, further supporting balance sheet growth. This creates a reflexive loop: capital access funds bitcoin purchases, which strengthens the balance sheet and sustains investor confidence, allowing continued issuance. As long as preferreds remain anchored near par, equity trades above the NAV, and capital markets stay open, the flywheel drives ongoing bitcoin demand.

Breakdown: How the Flywheel Slows and Unravels

The same reflexive structure can stall or reverse when conditions deteriorate. Declining bitcoin prices or weakening investor confidence can push equity below NAV (mNAV < 1) and preferreds below par, constraining capital markets access and making new issuance dilutive or infeasible. As asset coverage compresses, the liability stack becomes less supported, increasing reliance on management actions such as dividend adjustments to stabilize preferreds. With issuance impaired, the flywheel halts. Reduced capital inflows limit bitcoin purchases, slowing NAV growth, and further eroding confidence. The burden of adjustment falls primarily on the preferred layer through dividend deferrals, rate changes, or increased subordination. Notably, this process does not require insolvency. The structure can remain solvent while still delivering suboptimal outcomes for preferred holders due to the loss of confidence and funding access.

An Options Lens: STRC as Selling a Put on Bitcoin Coverage, with Caveats

For institutional investors, STRC and SATA can be viewed through an options lens. It resembles being short a put on bitcoin asset coverage, earning yield in exchange for bearing downside risk if bitcoin declines and erodes the asset cushion. Unlike a standard option, however, there is no fixed strike or maturity, and outcomes are path-dependent and shaped by management discretion. Dividends can be adjusted or deferred, subordination can increase through new issuance, and price stability is a policy objective rather than a guarantee.

From the issuer’s perspective, STRC monetizes this optionality by transferring downside risk to investors in exchange for flexible, non-mandatory capital. With no hard payment obligations, the issuer can actively manage dividends and issuance, raising capital in strong markets to acquire more bitcoin and reinforce the broader flywheel while retaining control over the capital structure.

Bitcoin Purchases Conditional on Price Stability

Critically, this mechanism depends on STRC trading near par, which enables economically viable at-the-market (ATM) issuance and, in turn, bitcoin purchases. In practice, this creates a market-imposed threshold where the preferred equity part of the flywheel only functions when demand and confidence are strong. When STRC trades below par, often during periods of sharp bitcoin price declines, issuance becomes uneconomic, limiting the ability to raise capital and slowing the flywheel.

SATA operates under a similar framework but has generally traded at a wider discount to par (see prior graph), constraining issuance and making price stabilization a key management priority. In response, Strive has taken steps to support trading levels, including increasing the dividend, explicitly setting aside cash reserves to support dividend distributions, and even purchasing STRC to support SATA's dividend obligations. The objective is to narrow the discount to par and restore economically viable issuance, underscoring how critical price stability is to activate the flywheel.

For Bitcoiners, these instruments are inherently conditional on market stability and should not always be relied upon as consistent drivers of bitcoin purchases across all environments.

Equity Offerings Still Matter

Even with all the talk about STRC, equity offerings remain a central pillar of Strategy’s capital strategy. While preferred offerings have added flexibility, equity issuance still overwhelmingly dominates in scale and impact. This is largely because Strategy's ability to issue equity at a premium to its net asset value (mNAV > 1) is critical to the model, enabling the company to raise capital in a way that is accretive on a bitcoin-per-share basis. As long as that premium persists, equity issuance effectively allows Strategy to expand its bitcoin holdings while increasing exposure per shareholder, reinforcing why equity offerings continue to matter despite the growing role of structured products like STRC.

Final Thoughts

STRC and SATA represent a new category of bitcoin-linked financing, one defined not by traditional credit fundamentals, but by asset coverage, confidence, market access, and active management of the capital structure. Their ability to drive incremental bitcoin demand can be strong, as recent weeks have demonstrated, but it is inherently conditional. When preferreds trade near par, and investor demand remains strong, the system can scale rapidly, reinforcing itself through a reflexive issuance-driven flywheel. However, this dynamic can shift quickly in more volatile environments.

For institutional investors, these securities are best understood not as static yield products, but as dynamic exposures to a managed system shaped by management decisions, subordination risk, and shifts in market confidence. As these structures mature, they offer a differentiated and increasingly relevant way to gain exposure to bitcoin-linked capital markets activity, with the potential for attractive risk-adjusted returns when approached with disciplined positioning and a clear understanding of the underlying dynamics.

Market Update

Bitcoin entered the week with improving momentum, before encountering resistance around $76K. Macro conditions then shifted decisively, as the latest FOMC decision triggered a broader risk-off move, amplified by rising geopolitical tensions tied to the protracted Iran conflict. Most risk assets moved lower, including equities. Notably, gold, despite its traditional safe-haven role, broke its upward momentum and declined sharply, underscoring the indiscriminate nature of the selloff. Against this backdrop, bitcoin retraced to $69K, down modestly on the week but still broadly holding within its recent range.

Positioning and flows point to a clear cooling in sentiment. Offshore perpetual funding rates are hovering near neutral, while CME basis, previously widening as a signal of incremental institutional demand, has compressed back to low single digits, indicating more cautious positioning. In spot markets, ETF flows have reversed. After a sustained period of consistent inflows during the prior rebound, flows reversed midweek, with Wednesday marking a notable shift to net outflows. Taken together, the move appears primarily macro-driven, though the softening in derivatives and ETF demand suggests institutional appetite has become more measured in the near term.

Important News This Week

Regulation and Taxation:

SEC Clarifies the Application of Federal Securities Laws to Crypto Assets - SEC

Investing:

Digital Credit Is the Latest Code Word for Leverage Among Crypto Treasury Companies - Bloomberg

Companies:

Blockfills Files for Bankruptcy Protection - Blockfills

Crypto Wealth Platform Abra to Go Public Through $750 Million SPAC Deal - CoinDesk

Metaplanet Raises $255 Million to Accelerate Bitcoin Accumulation - CoinDesk

Mastercard Agrees to Buy Stablecoin Platform BVNK for up to $1.8 Billion - CoinDesk

Cango is Selling Off its Bitcoin Stash to pay Down Debt and Fund an AI Makeover - CoinDesk

Bitrefill Reports Security Incident - X

Crypto’s True Believers Demand to Be Taken Seriously - Vanity Fair

Crypto Exchange Kraken Freezes Multibillion-Dollar IPO plan Due to Difficult Market Conditions - CoinDesk

Upcoming Events

Mar 27 - CME expiry

Apr 27 - Bitcoin 2026 conference