IN TODAY'S ISSUE:

- As DAT premiums continue to compress, we look at the factors at play.

- With share unlocks still ahead for the BTC DATs, premiums may continue to compress for some companies.

- There may be some cycle information being conveyed in DAT premiums, but the sample size is small.

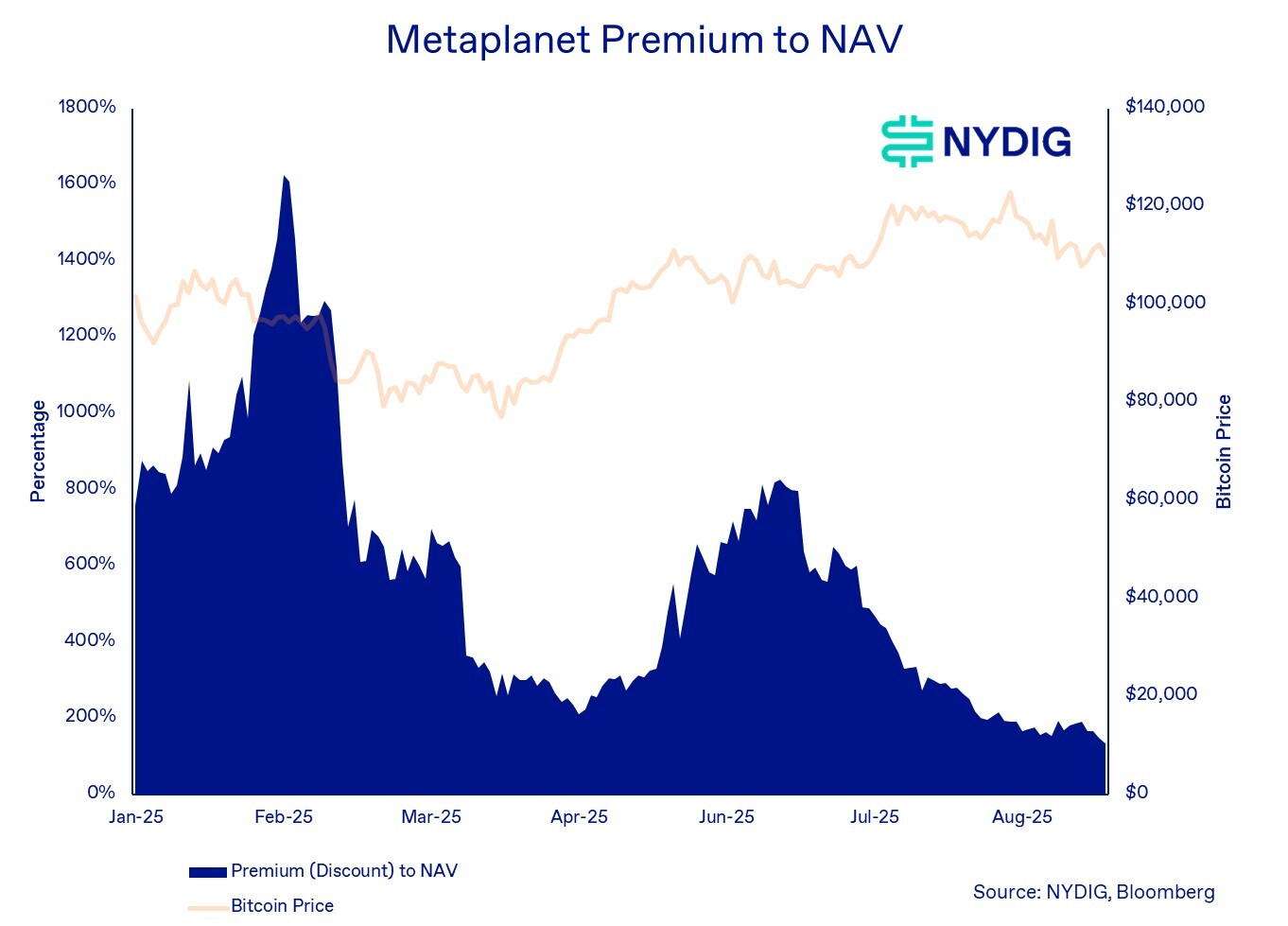

DAT Premiums Compress

Premiums on Digital Asset Treasury (DAT) companies, the gap between share prices and underlying net asset value (NAV), continue to compress. This trend persists even as bitcoin reached a new all-time high in mid-August and as DATs continue to proliferate. A clear example can be seen in the premiums at which the stocks of two leading DATs, Strategy (MSTR) and Metaplanet, currently trade.

The forces behind this compression appear to be varied: investor anxiety over forthcoming supply unlocks, changing corporate objectives from DAT management teams, tangible increases in share issuance, investor profit-taking, and limited differentiation across treasury strategies.

Unfortunately, A Bumpy Ride May Be Ahead

For many DATs, conditions may deteriorate before they improve. A number of bitcoin-focused DATs still have outstanding mergers or incomplete equity and debt financings. Completing these steps is often a necessary requisite for registering shares, which in turn allows unrestricted public trading of the shares. In many cases, over 95% of the new outstanding shares are tied to these transactions, raising the prospect of a substantial wave of selling once registrations are effective.

Complicating matters is the fact that the share prices of these DATs are trading at or even below the price of recent fundraises. Twenty One (CEP) shares are trading below their $21 PIPE from June (but above their $10 PIPE in April), Nakamoto (NAKA) is trading below their $5 additional PIPE (but above its $1.12 PIPE). ProCap/Columbus Capital (CEP) is trading just above its SPAC and preferred equity raise price, and Bitcoin Standard Treasury Co/Cantor Equity Partners (CEPO) is trading just above the price of its equity PIPE. We could easily see shares slip below these key price levels, which might exacerbate selling once shares are freely tradeable.

Share Buybacks Would Be Key

If DAT shares were to fall and trade below NAV, the most straightforward course of action would be stock buybacks. However, none of the major bitcoin DATs currently have buyback programs in place, except for Empery Digital (EMPD), which trades at a 24% discount to NAV. Nakamoto (NAKA), in fact, is moving in the opposite direction, with a $5B at-the-market equity offering that is likely to further compress its premium to NAV. If we were to give one piece of advice to DATs, it’s to save some of the funds raised aside to support shares via buybacks.

Accretive DAT Deals

A stage of market evolution that has yet to emerge is M&A or shareholder activism among DATs. While purchasing DATs trading below NAV is the obvious trade, a less intuitive scenario is one DAT acquiring another. Such a transaction could be accretive on a bitcoin-per-share basis simply because the acquirer trades at a higher premium to NAV than the target. Importantly, the target does not need to be at a discount to NAV for this dynamic to work. As a result, DATs with the highest NAV premiums and sufficient scale will have the greatest advantage in pursuing acquisitions. Over time, both premium levels and size are likely to determine which DATs become consolidators if the market reaches this stage.

Cycle Information in Premiums?

Although we have only one historical reference point, it raises the question of whether DAT premiums might signal stages of the broader market cycle. In the 2021 cycle, for example, MSTR’s premium to NAV peaked in February, preceding bitcoin’s $64K intermediate high in April and well before its ultimate $69K peak in November. With that in mind, the fact that MSTR’s premium to NAV topped out in November 2024 may be telling us something about the current bitcoin cycle. Still, with just one prior observation, it’s difficult to draw firm conclusions.

Market Update

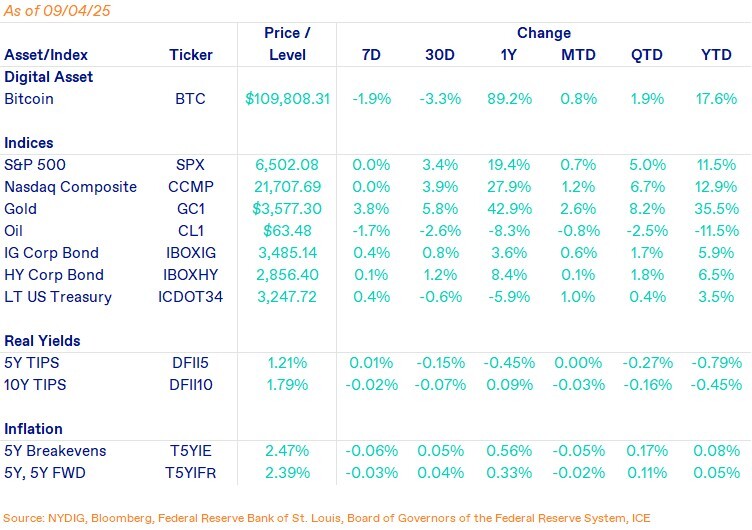

Bitcoin fell 1.9% in the week, hitting a low of $107,250 before rallying throughout the week. Equity markets were subdued, with both the S&P 500 and Nasdaq Composite flat on the week (yes, those percentages are right).

In recent weeks, the action in financial markets has been concentrated in precious metals, with both gold and silver breaking out to new highs after nearly five months of sideways consolidation (for gold). The rally was sparked by Fed Chair Powell’s remarks at the Jackson Hole Economic Symposium, which boosted expectations for rate cuts. Falling nominal rates, combined with the potential for rising inflation, drive real yields lower, enhancing the appeal of stores of value such as gold and silver. These dynamics should also support bitcoin. Adding to the case, rising government debt burdens, as highlighted by Ray Dalio (link below), further strengthen the outlook for both bitcoin and precious metals.

Important News This Week

Investing:

Ray Dalio on Macro Conditions, Precious Metals, and Crypto - X

Bitcoin-Volatility Collapse Forces Risk-Loving Traders Elsewhere - Bloomberg

Regulation and Taxation:

SEC and CFTC Staff Issue Joint Statement on Trading of Certain Spot Crypto Asset Products - SEC

US DOJ To Back Off Money Transmitter Cases in Shift Backed by Crypto - Reuters

The Loophole Turning Stablecoins into a Trillion-Dollar Fight - Wired

Trump Crypto News: World Liberty Financial Blacklists Justin Sun's Address With $107M WLFI - CoinDesk

Companies:

U.S. Bank Resumes Bitcoin Cryptocurrency Custody Services for Institutional Investment Managers - U.S. Bank

Galaxy and Superstate Launch GLXY Tokenized Public Shares on Solana - Galaxy

Upcoming Events

Sept 11 - CPI inflation reading

Sept 17 - FOMC interest rate decision

Sept 26 - CME expiry