IN TODAY'S ISSUE:

- We examine the market, macro, and narrative factors that are weighing on bitcoin and the broader crypto industry.

- With BTC falling to new cycle lows, the repeating 4-year cycles are coming back into view. We look at what the depth, duration, and on-chain metrics say.

- Poor contract design and dispute resolution can materially affect prediction market outcomes, as a recent event highlights.

What's Weighing on Crypto?

Bitcoin's recent weakness has pushed the asset back toward the February cycle lows of $60K, inciting investor questions around what’s driving the move. While no single catalyst appears sufficient to explain the decline, several narratives have emerged across macro, crypto-native, and technology markets that may be influencing sentiment, positioning, and capital flows. Below, we examine the key factors at play and assess how each may be contributing to the recent pressure on digital asset prices.

AI is a Competing Destination for Risk Capital

Bitcoin's recent weakness appears increasingly tied to competition for capital rather than any deterioration in the asset's underlying fundamentals. Over the last 18 months, artificial intelligence (AI) has become the dominant narrative across public and private markets, attracting an extraordinary share of incremental investment capital. AI’s impact on capital markets and economic trends is undeniable: AI is now one of the primary drivers of equity market performance, venture funding activity, corporate spending, and hiring trends. As that concentration has intensified, crypto has increasingly found itself competing against AI for the same pool of speculative and growth-oriented capital.

The overlap between the two investor bases is probably larger than many appreciate. Both AI and crypto attract investors seeking exposure to transformational technologies, asymmetric return profiles, and long-duration growth opportunities. When one narrative begins generating substantially stronger returns, capital naturally migrates toward the perceived opportunity set with the highest expected payoff, benefitting AI names and weighing on bitcoin.

The IPO Pipeline Could Create a Liquidity Vacuum

That dynamic may become more pronounced as investors look ahead to what could be the largest technology IPO cycle in more than a decade. Market participants expect several high-profile private companies, including SpaceX, OpenAI, Anthropic, Databricks, and Anduril, to access public markets in the coming quarters. While no formal timelines have been announced and several of these companies have not publicly filed registration statements, the expectation of eventual public offerings has become an increasingly important topic in institutional portfolios.

Collectively, these companies represent trillions of dollars of private market value and could ultimately seek hundreds of billions of investor capital through a combination of primary issuance and secondary share sales. Historically, large IPO cycles have acted as a temporary drain on market liquidity as institutions raise cash, trim existing positions, and preserve risk budgets in anticipation of participating in new offerings.

Crypto may be particularly vulnerable to this dynamic because many of the same investors allocating capital to bitcoin, crypto equities, and digital asset funds are also among the natural buyers of large-scale AI and technology IPOs. After several months of bitcoin underperformance relative to leading AI-related equities, some investors may be rotating capital toward what they view as the next major opportunity set.

None of this changes the long-term investment case for digital assets. It does, however, create a potential near-term flow headwind at a time when incremental demand already appears less robust than it was earlier in the cycle.

Iranian Crypto Asset Seizures Raise New Questions

Another potential overhang emerged following recent comments from Treasury Secretary Scott Bessent, who claimed that the United States had seized approximately $1 billion of Iranian-linked crypto assets. The statement was widely reported and immediately attracted attention across the digital asset industry, not because of the size of the seizure itself, but because of what it may imply about the government's capabilities.

Since its inception, crypto has benefited from a perception of sovereignty, censorship resistance, and independence from traditional financial enforcement mechanisms. Any suggestion that governments possess greater visibility into, or control over, digital assets than previously understood challenges part of that narrative.

What makes the story particularly notable is the absence of supporting information. Beyond Bessent's comment, "just outright grabbed the wallets,” little information has been released publicly regarding the activity. We do know Treasury sanctioned Iran’s largest digital assets firm, Nobitex, as well as 3 Iranian crypto exchanges, but not much is known beyond that.

The market may ultimately conclude that this was a unique enforcement action involving sanctioned entities, but until additional information emerges, investors are left with a gap between the scale of the claim and the amount of evidence available to evaluate it. At a minimum, that uncertainty has the potential to weigh on sentiment among market participants who view crypto as an alternative to traditional financial systems.

Strategy’s Role in the Market May Be Changing

The reported sale of 32 bitcoin by Strategy last week was economically insignificant, representing roughly $2.5 million of supply in a market that trades billions of dollars per day. Psychologically, however, the transaction may be far more important.

Since 2020, Strategy has served as one of bitcoin's most reliable sources of incremental demand. Regardless of market conditions, investors could rely on the fact the company would continue accumulating bitcoin whenever financing conditions allowed. That assumption became particularly important during periods when ETF inflows slowed and retail participation weakened, conditions that have characterized much of the last six to nine months.

The more important question is whether the transaction was followed by additional selling later in the week. Management had previously signaled the possibility of larger sales after attempting to “inoculate” the market with initial sales activity. Investors will therefore be focused on whether Strategy sold additional bitcoin to retire the remaining balance of its 2029 convertible notes or strengthen its cash position, with greater clarity to come from the company's 8-K filing on Monday morning. While the initial transaction was economically immaterial, incremental follow-on sales could begin to affect the marginal supply-demand balance, particularly as bitcoin demand has become increasingly concentrated among a narrower set of buyers.

Quantum Risks Move From the Shadows

Quantum computing has also re-entered the conversation, though not because of a breakthrough in quantum hardware. Instead, the catalyst has been the public emergence of quantum attack techniques that were previously hidden from public view.

Earlier this year, Google researchers published dramatically lower resource estimates for breaking elliptic curve cryptography, including the secp256k1 curve used across much of the cryptocurrency ecosystem, including Bitcoin. In the interest of responsible disclosure, the researchers withheld the underlying circuit designs and instead relied on a zero-knowledge proof that allowed independent verification of the results without, in Google's words, providing "a roadmap for bad actors."

More recently, a French cryptographer published a detailed circuit architecture that reproduces broadly similar performance characteristics and resource estimates. While the work does not reveal Google's exact implementation, it provides the first public blueprint for how such improvements can be achieved and makes much of the underlying innovation accessible to the broader research community.

The significance is not that quantum computers suddenly became capable of breaking modern cryptography. Rather, the episode highlights a continuing trend: the algorithmic resources required to attack elliptic curve cryptography continue to fall. As a result, the gap between theoretical vulnerability and practical feasibility is narrowing even in the absence of major advances in quantum hardware.

Multiple Headwinds, One Narrative

Viewed independently, none of these developments appears sufficient to drive a major correction in bitcoin. Viewed collectively, they help explain why price action has weakened despite the absence of a clear deterioration in underlying adoption metrics.

AI is attracting an increasing share of global risk capital. Anticipated IPO activity may be encouraging investors to raise liquidity. Sovereign seizure headlines are raising questions about crypto's role outside traditional financial systems. Strategy's transition from perpetual buyer to potential seller challenges a foundational market narrative. And renewed attention on quantum vulnerabilities has introduced an additional source of uncertainty.

At a time when incremental demand appears increasingly concentrated among a relatively small group of buyers, the cumulative impact of those headwinds may be proving more important than any single catalyst alone.

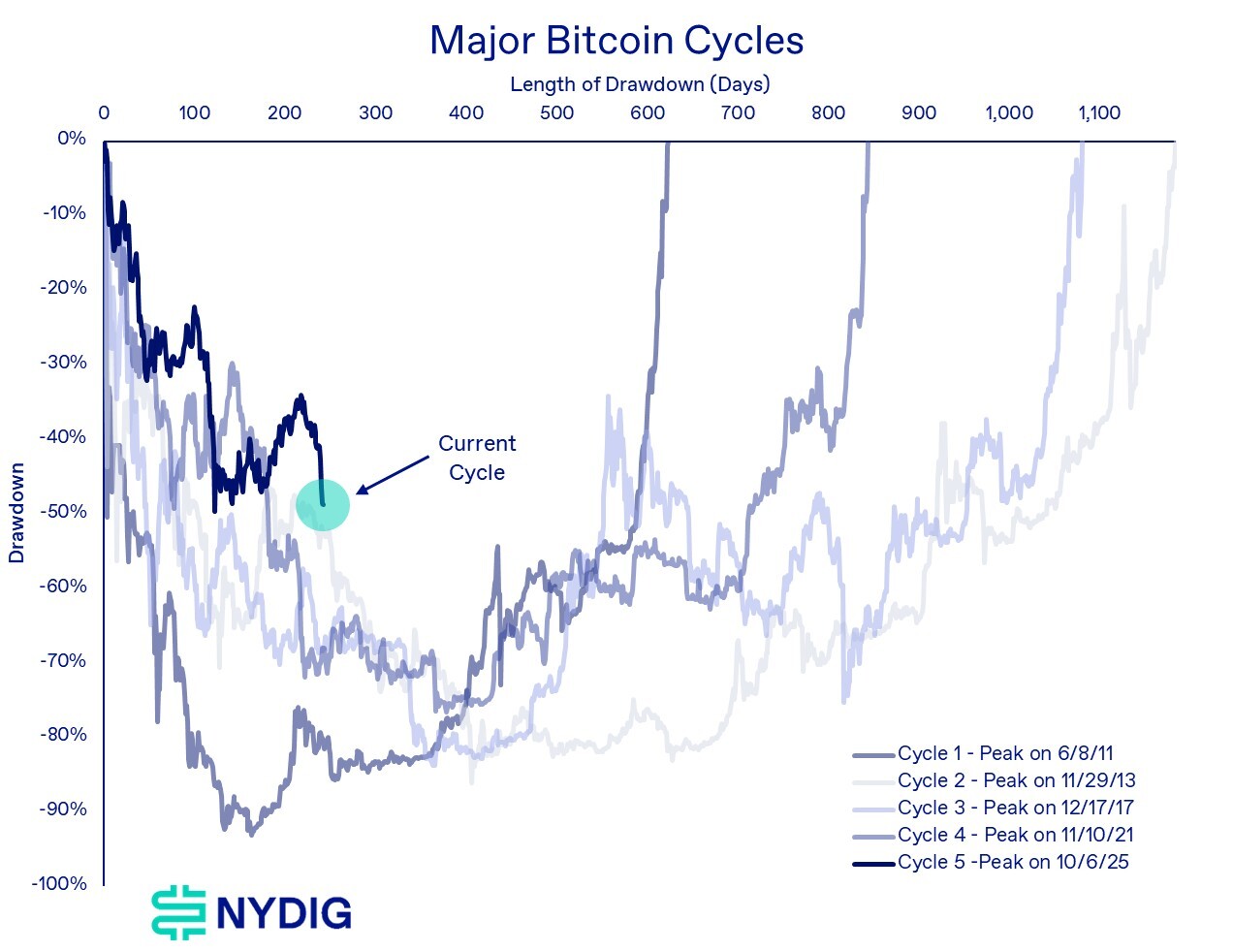

Re-Underwriting the Cycle

Bitcoin has reached new cycle lows, increasing the probability that the market is reverting to the historical four-year cycle pattern despite a materially shallower initial correction. We assess the cycle through three key dimensions: drawdown magnitude, drawdown duration, and a range of on-chain indicators relative to prior market cycles. Current metrics remain broadly consistent with historical cycle behavior, suggesting that the market continues to track a well-established pattern. However, if historical analogues remain the primary guide, the cycle's ultimate drawdown depth has likely not yet been reached.

Numerical Comparisons

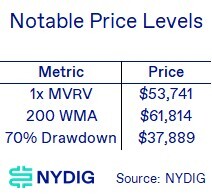

Relative to prior bitcoin bear markets, the cycle's current low price of $59,750 represents a 52.7% decline, materially shallower than the 77.6% drawdown recorded in 2021–2022 and well below the 84–94% declines observed in the first three cycles. While drawdown severity has compressed across successive cycles, a move to the projected low would still be broadly consistent with the long-term trend of diminishing downside volatility. Notably, a deeper correction to the 70% drawdown threshold near $37,900 would remain less severe than every prior cycle and would therefore still fit within the historical pattern of progressively shallower bear markets.

Several historically significant price levels are now coming into focus. The 1x MVRV level of $53,700 marks the point where bitcoin's market value converges with its aggregate cost basis, while the 200-week moving average near $61,800 has repeatedly served as long-term support during prior bear markets. Together, these levels provide an important reference range for assessing downside risk (we’ve already fallen through the 200 WMA, like the previous cycle drawdown). A decline toward the 70% drawdown level would imply a more complete retracement relative to prior cycles, but would still represent a meaningful narrowing versus the drawdowns experienced in previous market bottoms.

Depth and Duration Comparisons

One of the simplest ways to contextualize the current market is to compare the ongoing drawdown against previous bitcoin cycles. The current cycle has experienced a peak-to-trough decline of roughly 50%, significantly shallower than the +75% drawdowns observed during prior bear markets. Even with the recent downturn, the current cycle has thus far displayed greater resilience compared to prior drawdowns.

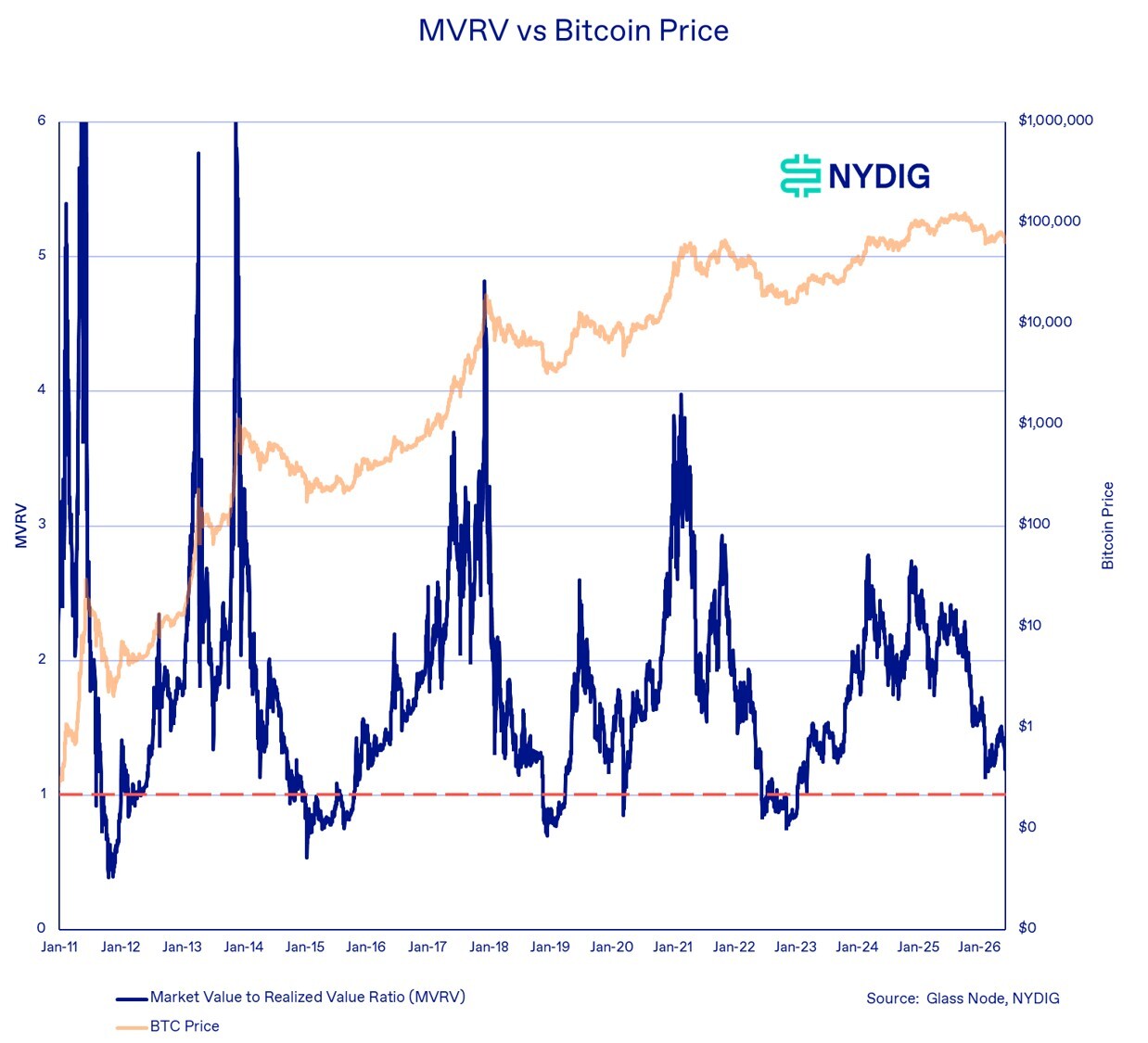

MVRV (Market Value to Realized Value)

MVRV measures Bitcoin's market capitalization relative to the aggregate cost basis of all coins. The current MVRV ratio sits at 1.2x, well below prior cycle peaks and only modestly above the 1.0 level that typically defines a cyclical bottom.

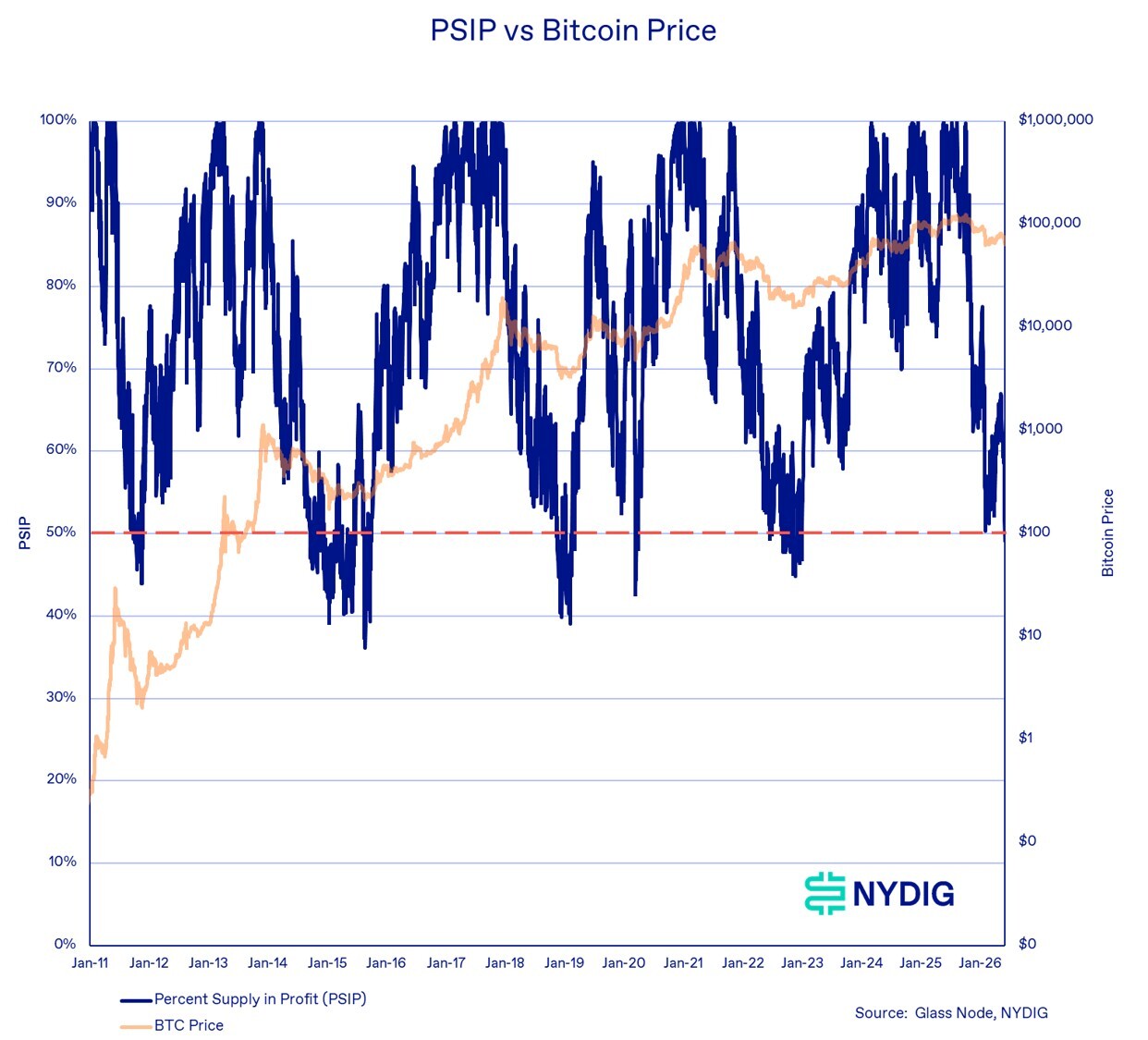

PSIP (Percent Supply in Profit)

Percent Supply in Profit measures the share of bitcoin supply currently held above its acquisition cost. Typically, cycle bottoms are formed when this metric breaks the 50% threshold. Bitcoin just hit 49% yesterday.

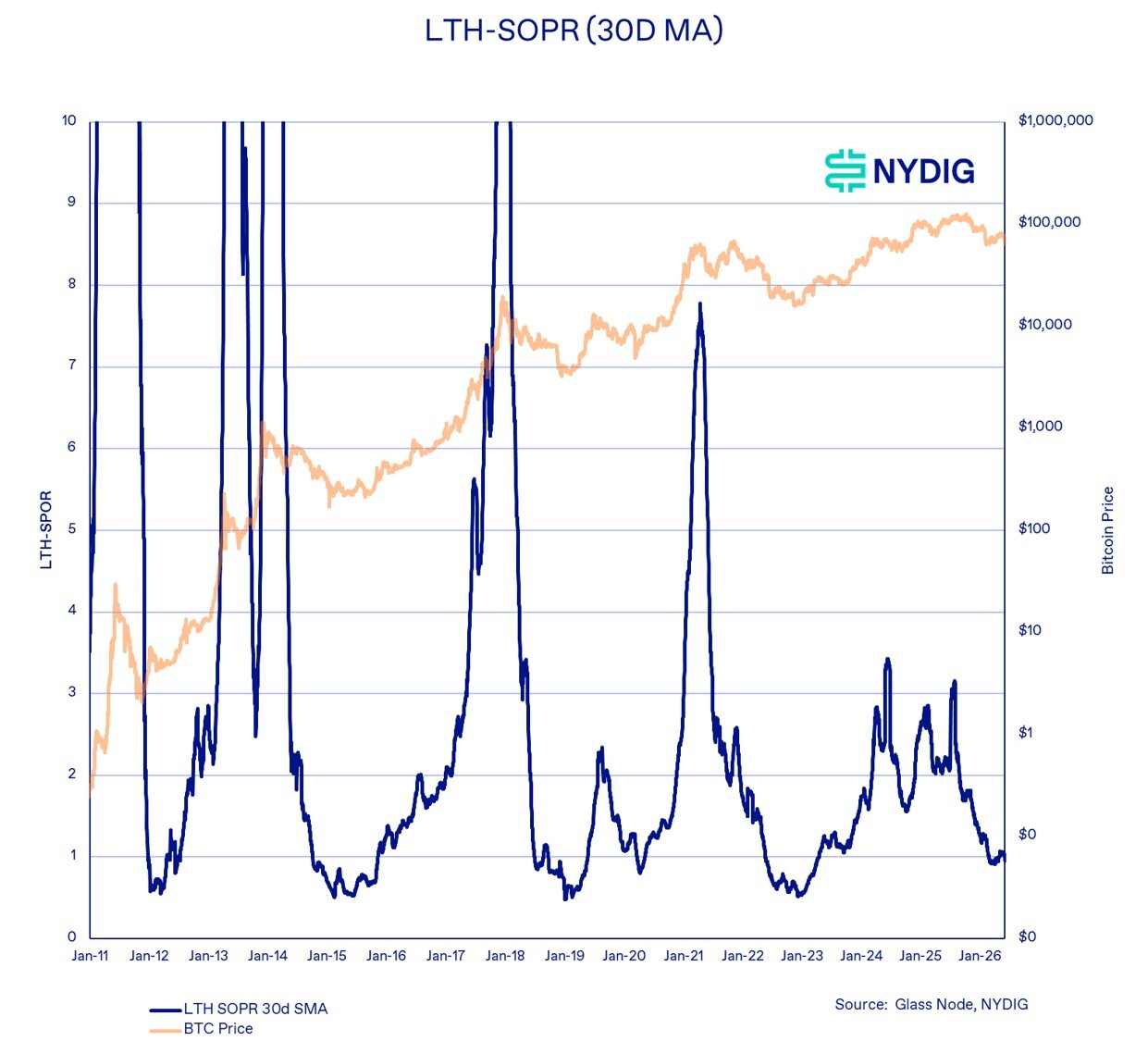

LTH-SOPR (Long-Term Holder Spent Output Profit Ratio)

LTH-SOPR measures whether long-term holders are spending coins at a profit or loss. Values above 1 indicate that long-term holders are realizing gains, while values below 1 indicate capitulation and loss realization. The metric recently reached 0.95. Historically, sustained readings near 1.0 have often served as reset periods that either establish durable bottoms or create the foundation for the next leg higher.

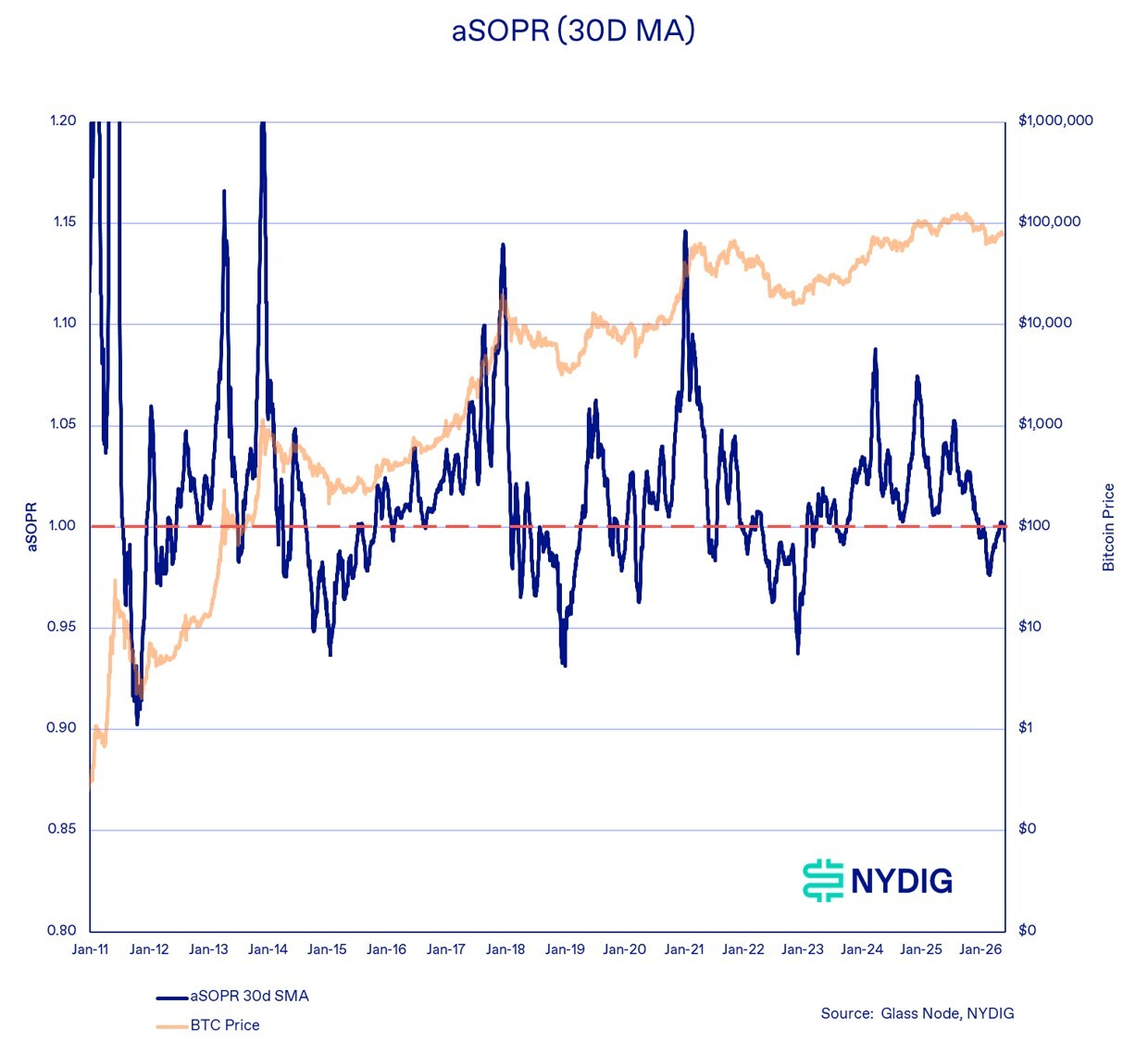

aSOPR (Adjusted Spent Output Profit Ratio)

aSOPR measures whether coins moved on-chain are being spent at a profit or loss, excluding short-duration transactions that add noise to the signal. The 1.0 level serves as an important dividing line between profit realization and loss realization.

The current reading sits almost exactly at 1.0, indicating that the average coin being spent is realizing neither significant gains nor significant losses. The current reading, therefore, suggests that speculative excess has largely been worked off. Market participants are not exhibiting the aggressive profit-taking behavior that typically accompanies late-cycle conditions.

Bottom Line

The on-chain data suggests the market has undergone a meaningful reset, but the evidence for a definitive cycle bottom remains mixed. MVRV is approaching historically attractive levels, Percent Supply in Profit is below 50%, and both SOPR metrics indicate that excess leverage and speculative positioning have largely been flushed from the system. However, the current drawdown remains substantially shallower than the 75% to 90% declines that marked prior cycle lows, and profitability metrics never reached the deeply distressed levels seen in 2015, 2018, or 2022.

The implication is that the recent correction exhibits many of the characteristics of a cyclical low, but fewer signs of the outright capitulation that has historically accompanied major bitcoin bottoms. Whether the low is already in place likely depends on whether institutional demand has structurally altered the cycle or merely delayed a deeper reset.

The MicroStrategy Polymarket Resolution Controversy

The dispute surrounding Polymarket's "MicroStrategy sells any Bitcoin by May 31" contract highlights a fundamental weakness in prediction markets: poorly specified resolution criteria can create ambiguity even when the underlying facts are not in dispute.

The relevant facts appear straightforward. Strategy disclosed in a June 1 Form 8-K that it sold 32 bitcoins during the period from May 26 through May 31. The filing explicitly states that the sales occurred within the contract's stated time window. By any ordinary reading of the question “whether MicroStrategy sold any bitcoin by May 31?” the answer is unambiguously "Yes."

The controversy stems from the timing of the disclosure rather than the timing of the transaction. Following a challenge of the market’s initial “No” resolution, the resolution was upheld by holders of the UMA token, which governs Polymarket's dispute resolution system. Polymarket relies on on-chain voting, where disputed outcomes are ultimately decided through token-holder voting of using the UMA token rather than by Polymarket itself. In this case, additional guidance reportedly argued that no information from Strategy, on-chain data, or a consensus of credible reporting confirmed the sale before the market deadline, and that confirmation obtained after expiration would not qualify.

That interpretation effectively transforms the question from "Did MicroStrategy sell bitcoin by May 31?" into "Was there public confirmation by May 31 that MicroStrategy sold bitcoin by May 31?" Those are materially different questions. The first concerns an underlying real-world event. The second concerns the availability of evidence about that event at a specific point in time.

The distinction matters because Bitcoin transactions are disclosed after they occur. Public companies routinely report transactions days after execution through SEC filings. A market intended to predict whether an event occurred should generally resolve based on whether the event occurred, not whether market participants possessed the evidence of the event before expiration. Moreover, the idea that “on-chain data” would resolve the timing of the sale is a naive interpretation of how bitcoin sales with institutions occur. The on-chain movement results from settlement of a trade, not the sale itself, which happens off-chain, typically the day before settlement (on-chain movement).

After a second dispute, the contract was finally resolved to the initial “No” outcome, robbing investors of their money, not because they were wrong, but because the contract was poorly specified and the governance vote failed to correct an error.