IN TODAY'S ISSUE:

- We reopen the crypt of macro factors to unearth the linkage between bitcoin and inflation, a relationship that refuses to stay buried.

- We revisit the original reactions to the Bitcoin white paper to reveal that what now seems inevitable emerged from the shadows, shrouded in doubt and disbelief.

- Two chilling news stories remind us that cryptocurrencies are far harder to kill than many dare to imagine.

When Macro Factors Go Bump in the Night

Last week, our observations on bitcoin’s returns and macro factors, particularly inflation, stirred up a few spirits with the data. While it is always a challenge to present complex statistical analysis in a concise and digestible manner for expert and general audiences alike, we wanted to add one more layer of depth to our analysis supporting our claim around bitcoin and inflation’s statistical significance, which plainly translates to “unlikely due to random chance.” In other words, not just another phantom in the numbers.

Filtering bitcoin’s correlation coefficients (we like that correlations show directionality vs R-squareds) with various macro factors, the observation about current inflationary measures and their lack of impact on bitcoin becomes more apparent. Only one observation meets the hurdle of statistical significance. What works better, though, is inflation expectations, 5-year breakeven rates. This omen is a market-based measure of inflation over the next 5 years — the difference between nominal 5-year Treasury bonds and 5-year TIPS.

The legend of bitcoin as an “inflation hedge” is almost as old as Bitcoin itself, rooted in its fixed supply. Yet, analysis shows that bitcoin’s price tends to align more closely with inflation expectations than with actual, current inflation readings. In reality, bitcoin functions less as a hedge than the CPI boogeyman and more as a hedge against something more sinister, eroding confidence in fiat currencies and monetary policy. Other macro factors lurking in the shadows, such as global liquidity (M2), real yields, and the U.S. Dollar Index, also play significant roles, highlighting that a confluence of factors affects bitcoin’s price, not just the specter of inflation.

A White Paper in the Dark

Today, Halloween, marks the 17th anniversary of the release of the Bitcoin white paper, the moment it was first summoned into existence. Satoshi Nakamoto’s announcement was shared with The Cryptography Mailing List on Metzdowd, likely reaching only a small cabal of cryptography enthusiasts at the time. Few knew then that something revolutionary had just crawled out of the digital ether.

While we can’t know exactly how many souls saw Satoshi’s original post, we do know how some of the community’s active members initially reacted, including James A. Donald, John Levine, Ray Dillinger, Nicolas Williams, and Hal Finney. In hindsight, Bitcoin’s brilliance might seem obvious, but the early responses reveal a mix of curiosity and caution as they witnessed this strange new creature born of both math and mystery. Finney expressed notable optimism, yet much of the broader discussion reflected deep skepticism, both about Bitcoin’s economic feasibility and its technical foundations.

Today, we look back at the launch thread and summarize the viewpoints of those who commented. The full thread can be found here, but this is a summary of the viewpoints of the initial respondents.

James A. Donald – Economic and Technical Skeptic

Donald argued that verifying transactions at a global scale would require too much bandwidth and storage and questioned how bitcoin could gain value without intrinsic worth or centralized backing.

John Levine – Security Critic

Levine believed attackers already controlled far more computational power than ordinary users, undermining the proof-of-work security assumption at the heart of Bitcoin.

Ray Dillinger – Economic Doubter

Dillinger thought continual hardware improvements would cause inflation and that proof-of-work offered no inherent demand or value, making it unstable as money.

Nicolas Williams – Double Spend Skeptic

Williams argued that anonymity and post-double-spend detection weren’t enough and that the system needed near-instant agreement on transaction order.

Hal Finney – Constructive Supporter

Finney supported the concept of decentralized proof-of-work money but asked detailed technical questions about how Bitcoin would function in practice. Finney was the only respondent to the Bitcoin white paper thread who also commented on the launch of Bitcoin v0.1 software, becoming the network’s first transaction recipient.

Seventeen years later, we look back and see how unobvious it all was. What was mostly dismissed as fantasy became a trillion-dollar idea that refuses to die, no matter how many times skeptics pronounce it buried.

Sitting here in 2025, it’s worth asking: what new idea today seems strange, unsettling, or impossible, but might be inevitable 17 years from now?

Cryptocurrencies: Zombie Edition

Two news items in the past few weeks captured an important and strange truth about crypto’s durability. First, Kadena’s foundation announced it is shutting down operations, leaving the blockchain to run without a core team (Kadena launched in 2020). Second, Stratis, one of the older enterprise-focused projects, rebranded as Xertra, pivoting from “blockchain-as-a-service” to a new focus on gaming and DeFi. On the surface, one project is fading out, the other is trying to reinvent itself. Both events show how hard it actually is to kill a cryptocurrency.

Unlike startups or companies, blockchains don’t have a single switch you can turn off. There’s no CEO to fire, no servers to unplug. As long as someone somewhere runs a node or holds a copy of the ledger, the network continues to exist. Kadena’s chain will likely keep producing blocks, miners may keep validating, and investors will still trade its tokens, provided there’s a venue to do so, even if active development stops. Stratis, on the other hand, demonstrates the ‘survival through adaptation’ model: if you can’t die, you pivot. The same infrastructure and token can be rebranded, given a new story, and relaunched for a different audience.

These cases highlight an underappreciated feature of decentralization: even failure is distributed. Crypto networks can be abandoned, neglected, or forgotten, yet they rarely vanish completely. Some limp along indefinitely while others evolve into something new. In that sense, blockchains behave less like businesses and more like digital organisms: some go extinct, some mutate, and a few lie dormant until the next cycle of attention brings them back to life.

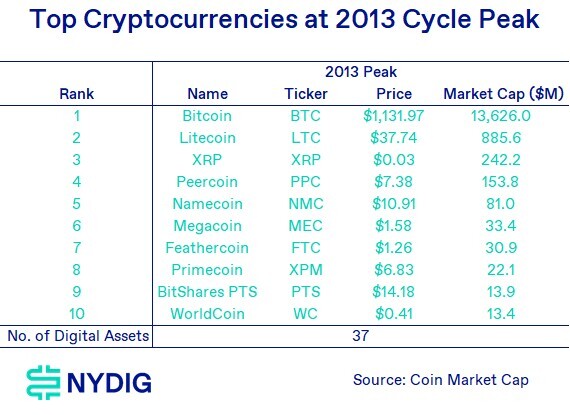

A look at the top coin rankings at the cycle peak in 2013 reveals numerous coins that have faded from public view, yet only Megacoin, BitShares, and WorldCoin seem to not be traded somewhere. In crypto, it seems what’s dead may never truly die.

Market Update

Bitcoin took a chilling turn this week, dropping 3.4%, but continued its broader trend of range-bound trading. The financial markets, including bitcoin, tumbled on Wednesday after the FOMC delivered a second consecutive interest rate cut but signaled uncertainty about another reduction in December, disappointing market expectations. Even with the correction, U.S. stocks ended the week up, while gold prices continued to correct after hitting a new all-time high two weeks ago.

The corrective price action in bitcoin drained funds from the ETF complex, which had been showing modest inflows until Wednesday. This week also saw the launch of 4 new spot crypto ETFs – Bitwise Solana Staking ETF (BSOL), Grayscale Solana Trust ETF (GSOL), which was a conversion from a closed-end grantor trust, Canary HBAR ETF (HBR), and Canary Litecoin ETF (LTCC). Net inflows in the ETFs have been mixed, with BSOL the clear leader with $152.5M of inflows, HBR with $32.1M, GSOL with $1.4M, and LTCC with $0.5M.

“Uptober” has turned into a trick rather than a treat, with bitcoin heading for just its 5th month-of-October loss since 2011. While Q4 has historically been a powerful time for bitcoin returns, little catalysts have emerged that would crystallize a movement outside the $107K - $123K trading band. Funding rates on perpetual swaps and basis on CME-listed futures, both subdued, confirm traders’ apathy right now.

Important News This Week

Investing:

Locked Out and Liquidated: Traders Blame Binance for $19 Billion Crash - Forbes

Unveiling GoDark: Crypto’s New Institutional Dark Pool Backed by Copper, GSR, Others - CoinDesk

Mt. Gox Delays Creditor Repayment to October 2026 - CoinDesk

JPMorgan to Allow Bitcoin and Ether as Collateral in Crypto Push - Bloomberg

Regulation and Taxation:

Trump to Pick Michael Selig for CFTC Chair Amid Crypto Expansion - Bloomberg

Tensions Rise as Senate Democrats, Crypto Executives Meet on Sweeping Digital Assets Bill - The Block

Warren Calls on Treasury to Close Gaps in GENIUS Act to Protect Consumers, U.S. Financial Stability, and National Security - Senate Banking Committee

OCC Announces Conditional Approval for Chartering Erebor Bank - OCC

CZ Threatens Elizabeth Warren with Lawsuit Over ‘Money Launderer’ Claim - Protos

Companies & Industry:

Citi and Coinbase Join Forces to Boost Digital Asset Payment Capabilities for Global Clients - Citi & Coinbase

Upcoming Events

Nov 13 (est) - CPI release

Nov 28 - CME Expiry

Dec 10 - FOMC interest rate decision