IN TODAY'S ISSUE:

- Critics say banks are losing out in the stablecoin game, but they just need to get creative.

- TradFi continues to drive crypto as we see a DAT for DAT transaction.

- Options open interest skyrockets and volatility sinks.

Why Stablecoin Critics Have It Backwards

Stablecoins now represent more than $287 billion in value, up about 38% year-to-date according to DefiLlama, and they’ve become one of the defining features of this cycle. Their role was further solidified with the passage of the GENIUS Act, which gave them a clear legal footing and drew the attention of fintechs, banks, and payment providers alike.

As with any new technology or financial innovation, though, regulation has produced some unexpected edge cases. The most prominent involves interest-bearing stablecoins, which the banking industry lobbied against and was ultimately successful in prohibiting. The reason banks were against them is that they feared interest-bearing stablecoins would steal from their traditional deposit base, which is central to their lending business.

Banks are at a Disadvantage, Critics Argue

Recent (here, here, and here) reports suggest growing frustration within the banking industry over platforms like Coinbase offering rewards on stablecoin deposits. Ironically, banks had previously lobbied for a ban on interest-bearing stablecoins to protect their deposit bases. Instead of safeguarding deposits, the policy has redirected yield opportunities to crypto platforms. Coinbase, for example, offers up to 4.1% on USDC balances, labeling the payouts as “rewards” rather than interest, though the distinction is largely semantic from a holder’s perspective.

The reason this works is because of the business model of stablecoins. Thanks to documents filed during Circle’s IPO process, we now know a lot about the business of stablecoins. Most of the investing public understands that stablecoin issuers take in dollars from users and issue them a commensurate number of stablecoins. Those dollars are invested in various low-risk instruments that provide a return. That investment income goes to the issuer, Circle in the case of USDC or Tether in the case of USDT.

Issuer vs. Custodian

A critical nuance in the stablecoin debate is the distinction between issuers and custodians of the stablecoins. Circle issues USDC, while platforms like Coinbase act as custodians. By law, USDC itself cannot pay interest. Stablecoin issuers are explicitly barred from doing so under the GENIUS Act. Stablecoin custodians, however, can pay “rewards” to users, often funded through revenue-sharing agreements with Circle and, in Coinbase’s case, supplemented by its own resources. Unlike bank deposits, USDC balances cannot be treated as FDIC-insured liabilities, meaning banks cannot lend against them without first redeeming for dollars.

Revenue Sharing Drives Rewards

Circle’s filings reveal how these rewards are funded. Coinbase, as a co-creator of USDC, receives a share of Circle’s reserve income, giving it greater earnings on USDC balances than Circle itself. This revenue, plus Coinbase’s own top-ups, underpins the rewards rates offered to users, which resemble interest in practice if not in form. Binance, by contrast, secured a $60.25 million upfront payment from Circle in 2024 to promote USDC distribution, highlighting how different platforms structure their incentives.

Banks Need to Get Creative

Banks can custody stablecoins too, they just count them as insured deposits to lend against (among other things). In practice, banks could instead adopt a model similar to Coinbase’s: earn a revenue share from Circle on USDC balances custodied, pass part of that back to customers as rewards, and position the product alongside real-time payments, cross-border settlement, and FX conversion services. So when critics complain that banks are at a disadvantage because “stablecoins can’t pay interest,” they’re missing the point: banks don’t need stablecoins to pay interest. They just need to get creative about how to share the rewards.

TradFi Continues to Drive Crypto

Over the past eighteen months, the principal drivers of the crypto narrative have increasingly originated in traditional financial markets. The approval of ETFs marked the initial shift, followed by the emergence of corporate bitcoin treasuries, high-profile IPOs such as Circle’s listing, and, most recently, the formation of purpose-built bitcoin treasury corporations, commonly referred to as digital asset treasury companies (DATs).

This evolution reflects a broader realignment of market attention. Analytical focus has shifted from blockchain-specific activity to traditional financial filings and market structures. The SEC’s EDGAR database and Bloomberg terminals are more important than block explorers and blockchain data. Except for occasional large transfers, Bitcoin’s blockchain activity has been relatively subdued, while the material developments are occurring in listed markets, corporate balance sheets, and capital formation events.

This week’s public offerings of Figure and Gemini extend the trend, joining Circle, eToro, Bullish, and Galaxy in capitalizing on the favorable U.S. regulatory environment.

In addition, a new DAT, Forward Industries (FORD), was launched with a $1.65 billion Solana treasury, backed by Galaxy, Jump, and Multicoin. These developments underscore the extent to which traditional financial infrastructure has become the primary venue for digital asset innovation and capital allocation.

This week, we saw a notable DAT for DAT investment where one DAT invested in another DAT. Nakamoto/Kindly (NAKA) purchased $30M of shares in Metaplanet’s (MTPLF) $1.45B capital raise. The purchase was funded with cash, and while it makes sense theoretically, given that NAKA trades at 2.5x mNAV and MTPLF trades at 1.6x, it would’ve been more effective to use the cash to buy spot bitcoin (at 1x mNAV). Still, we think this could be a harbinger of things to come, where DATs become more intertwined with transactions like this.

Options Open Interest Skyrockets as Vol Sinks

On July 29, the SEC approved a tenfold increase in position limits for several bitcoin ETFs and authorized options trading on an additional fund. Since then, open interest in bitcoin ETFs has risen 47.6% in less than six weeks. Over the same period, bitcoin’s implied volatility across various tenors has fallen by roughly 10% or 4 points. On a year-to-date basis, bitcoin implied volatility is down roughly 40% depending on the tenor. While the increase in position limits is not the sole driver of this decline, the expanded capacity for larger positions has likely reinforced the trend toward lower volatility.

Notably, FBTC was the only existing bitcoin ETF that did not receive approval for the 10x increase in position limits, as no application was filed. We initially expected that this could jeopardize its position as the second-largest fund. Instead, FBTC has posted the strongest gains on a percentage basis. The likely explanation is that traders had previously underutilized FBTC options relative to its market size, leaving room for outsized growth despite the unchanged limits.

Market Update

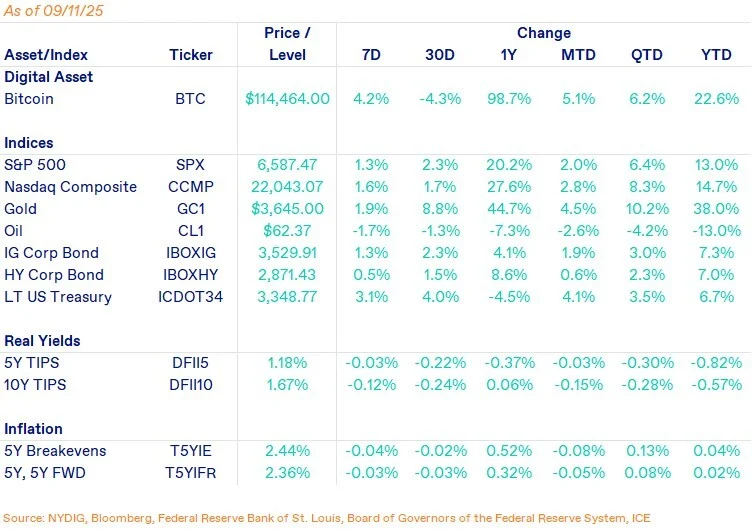

Bitcoin rallied 4.2% in the week, breaking through $116K at one point before trading off. Nearly every other asset class rallied this week as well, with the S&P 500 and Nasdaq 100 zooming to new all-time highs. Gold bumped up nearly 2%, bringing its year-to-date return to 38.0%. Even bonds got in on the action, with investment grade, corporate bonds, and long-term US Treasuries all up.

Against this backdrop, the US Dollar Index (DXY) continues to loiter around the lows. The dollar weakness, along with declining real interest rates, acts as a forcing function for risk assets and stores of value. Added on top of that are increasing prospects for interest rate cuts, and there’s a powerful backdrop for the cycle to continue.

Important News This Week

Investing:

The $7T Tailwind for BTC and Altcoins - CoinDesk

Echoes of Summer 2023: Bitcoin’s Volatility Set to Surge - CoinDesk

Growing Number of Family Offices Interested in Crypto Goldman Finds - Bloomberg

Regulation and Taxation:

New White House Crypto Adviser Patrick Witt Calls Market Structure Bill Top Priority - CoinDesk

Brian Quintenz Accuses Tyler Winklevoss of Lobbying Trump to Block His CFTC Chair Nomination - The Block

Companies & Technology:

Crypto Asset Manager CoinShares in U.S. SPAC Deal - CoinDesk

Bukele Says El Salvador Purchased $2.3 Million in BTC to Mark Bitcoin Law Anniversary - The Block

The Spectacular Comeback Tour of Ross Ulbricht, the Founder of Silk Road - NYT

Ledger CTO Warns Users to Halt Onchain Transactions Amid Massive NPM Supply Chain Attack - The Block

Binance, Franklin Templeton Join Forces to Expand Digital Asset Products - CoinDesk

Empery Digital Announces Update on Share Repurchase Program - Empery Digital

Metaplanet Sets $1.45B Share Sale to Fund Bitcoin Purchases, Treasury Shift - Decrypt

Stablecoin Talent Race on Wall Street Sends Pay Soaring - Bloomberg

Upcoming Events

Sept 17 - FOMC interest rate decision

Sept 26 - CME expiry